Owner Financing: A Smart Move for Missouri Sellers

Jul 09, 2026

Written by David Dodge

If you are trying to sell a home in Missouri this summer, you are likely feeling the friction. We are sitting squarely in the middle of 2026, and traditional buyers are paralyzed. Why? Because the traditional banking system has made borrowing incredibly expensive and frustratingly rigid. But there is a creative, highly effective solution that allows you to bypass the banks entirely, dictate your own terms, and get your home sold: owner financing. Let’s take a deep dive into how you can use this strategy to bypass traditional lending barriers and secure a steady, lucrative income stream.

The "Rate Lock-In Effect" and the 2026 Buyer Paralysis

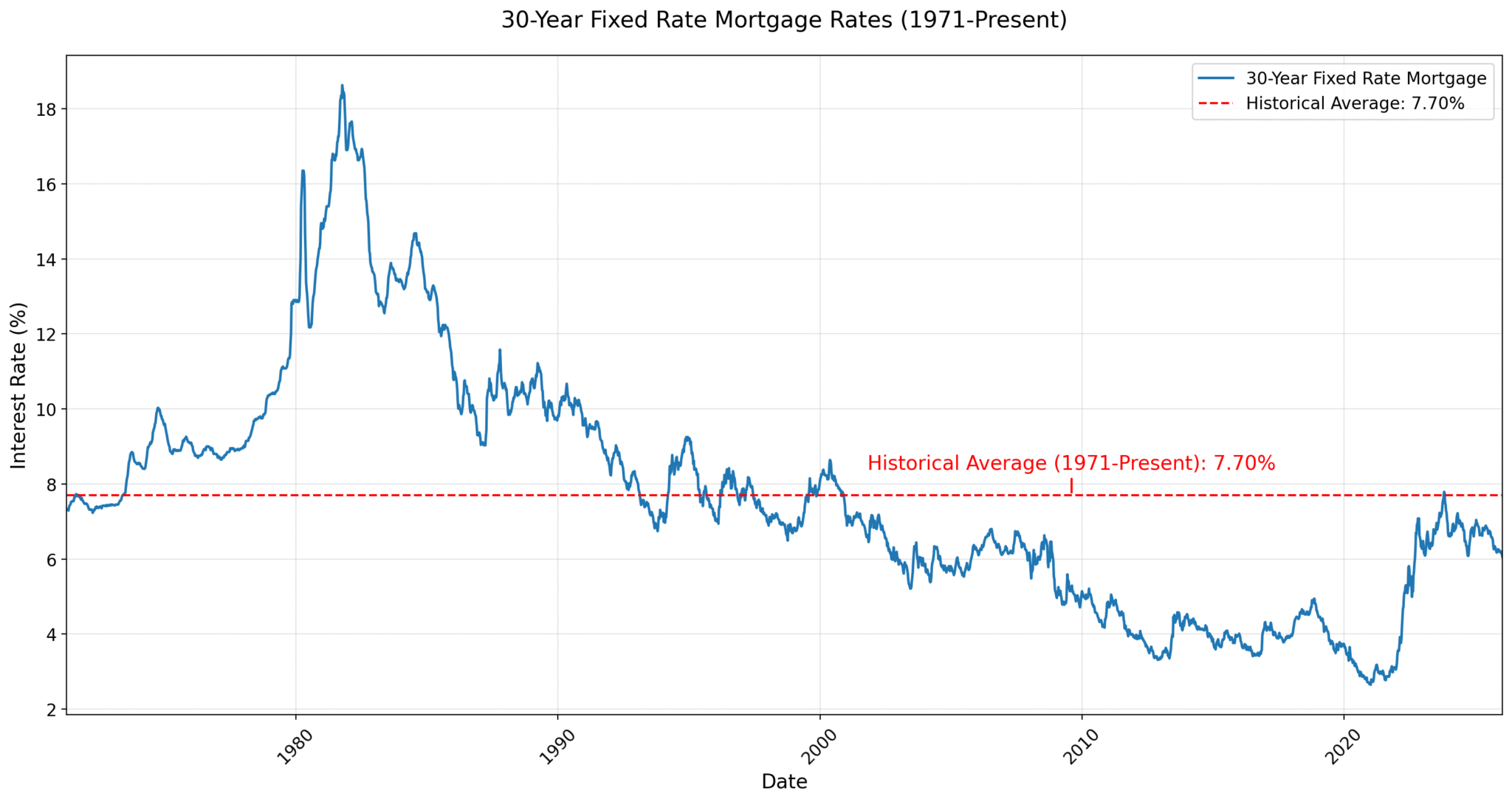

To understand why owner financing is having a major renaissance in Missouri right now, we first have to look at the macroeconomic climate of July 2026. Traditional real estate transactions rely on a delicate balance: buyers need affordable capital, and sellers need buyers who can qualify for that capital. Right now, that balance is severely disrupted by what economists call the "rate lock-in effect."

During the pandemic years of 2020 and 2021, millions of Americans secured 30-year fixed mortgages at historic lows—often between 2.5% and 3.5%.

This creates a massive gridlock:

-

Homeowners won't sell: A homeowner sitting on a 3% interest rate is deeply reluctant to sell their home and buy a new one at 6.7% because their monthly payment would skyrocket, even for a home of the same price.

-

First-time buyers are priced out: The combination of elevated home prices (the median home price in the St. Louis MSA is sitting near $309,900) and 6.5%+ interest rates means the monthly payment (principal and interest alone) is pushing many perfectly stable, employed renters completely out of the traditional mortgage market.

-

Tightened underwriting: Because the cost of capital is high, traditional lenders (banks and credit unions) have tightened their lending standards.

30-Year Fixed Mortgage Rate Trends (2023-2026). Source: The Mortgage Reports

When traditional buyers are stuck on the sidelines, properties sit on the market longer. If you have a home to sell in Missouri right now, waiting for a buyer with a pristine W-2 and a 780 credit score to brave a 6.7% interest rate is a test of patience.

This is exactly where owner financing (also known as seller financing) steps in as a strategic bypass around the bottleneck of the traditional banking system.

What is Owner Financing?

In a standard real estate transaction, the buyer goes to a bank, the bank hands you (the seller) a lump sum of cash, and the buyer spends the next 30 years paying the bank back with interest.

In an owner financing arrangement, you become the bank.

Instead of receiving a lump sum from a traditional lender, you and the buyer agree on a purchase price, an interest rate, a down payment, and a repayment schedule.

In Missouri, this is typically secured using two essential legal documents:

-

The Promissory Note: The buyer’s legally binding written promise to repay the loan under the agreed-upon terms (interest rate, monthly payment amount, duration).

-

The Deed of Trust: The security instrument recorded with the county. In Missouri, a Deed of Trust is preferred over a standard mortgage because it allows for a faster, non-judicial foreclosure process. If the buyer stops paying you, the Deed of Trust gives a designated third party (the Trustee) the power to sell the property to recover your money, meaning you can take the property back without having to drag the buyer through a lengthy, expensive court battle.

Positioning Owner Financing as a Strategic Bypass

By offering owner financing, you are completely removing the biggest obstacle in the 2026 housing market: institutional lending barriers. You are no longer waiting for an underwriter in a cubicle three states away to approve your buyer. You make the rules.

Why Traditional Lenders Fail Good Buyers Today

Consider the modern St. Louis workforce. Many potential buyers are small business owners, freelancers, or contractors. A traditional bank looks at a self-employed buyer’s tax returns—which are legally and smartly optimized to show as little taxable net income as possible—and declares them "unqualified."

Other buyers might have experienced a localized financial hardship—a medical bill dispute or a temporary job loss in 2024—that temporarily dinged their credit score to a 620. A bank sees a rigid number and denies the loan. You, as a human being, can look at their sizable down payment, their current steady income, and their rental history, and make a logical, secure business decision to lend to them.

According to local market analysts reviewing

The Compelling Benefits for Missouri Sellers

Offering terms on your property isn't just an act of charity for locked-out buyers; it is one of the most lucrative wealth-building strategies available to real estate investors and private sellers.

1. Steady, Passive Monthly Income

When you sell for cash, you get a lump sum. Unless you immediately deploy that cash into another high-yield investment, it sits in a bank account losing purchasing power to inflation. When you owner-finance, your equity is put to work instantly. You receive a down payment upfront, plus a monthly check that includes both principal and interest.

2. Maximum Asking Price

Because you are offering a unique, highly demanded service (financing), you have incredible leverage over the purchase price. Buyers who cannot qualify for a bank loan are not in a position to haggle over the asking price. If your home in Florissant or South City is worth $220,000, you can confidently list and sell it for full market value (or even slightly above) because the value to the buyer is the opportunity to buy, not just the house itself.

3. Faster Closings and "As-Is" Sales

Traditional bank loans require appraisals and strict inspections. If a traditional buyer’s FHA or conventional lender sends an appraiser who flags peeling paint, an older roof, or a missing handrail, the bank will refuse to fund the loan until you (the seller) fix it.

With owner financing, there is no bank appraiser. You can sell the property strictly "as-is." If the buyer is happy with the condition, you can draft the paperwork, head to a title company, and close the transaction in a matter of days rather than waiting 45 to 60 days for bank underwriting.

4. Tax Advantages (Installment Sales)

If you sell an investment property for a lump sum, you may be hit with a massive capital gains tax bill in a single year. Owner financing is classified by the IRS as an "installment sale." Because you are receiving the proceeds of the sale over several years, you spread out your capital gains tax liability, potentially keeping you in a lower tax bracket and keeping more money in your pocket.

The Incredible Benefits for Buyers

Why would a buyer choose owner financing, especially if the interest rate might be slightly higher than the

1. Skipping the Bank Approval Process Entirely

No W-2 requirements, no strict debt-to-income limits, and no arbitrary credit score cutoffs. The buyer’s qualification is determined entirely by you. For self-employed buyers or those recovering from past credit issues, this is often the only path to homeownership in 2026.

2. Lower Closing Costs

Traditional mortgages come with predatory junk fees: loan origination fees, application fees, bank appraisal fees, discount points, and private mortgage insurance (PMI). These can easily add $5,000 to $10,000 to the buyer’s closing costs. In an owner-financed deal, these fees evaporate. The buyer only pays standard title company fees, state recording fees, and attorney document prep fees.

3. Immediate Equity and Ownership

Unlike "rent-to-own" or lease-option schemes—which can often be predatory and rarely result in the buyer actually owning the home—owner financing is a legitimate transfer of ownership.

4. A Bridge to Traditional Financing

Most owner-financed notes are structured with a "balloon payment" after 5 to 7 years. This means the buyer makes regular monthly payments for five years, and at the end of that term, the remaining balance is due in full. This serves as a bridge. It gives the buyer 5 years to live in the home, improve their credit score, establish a rock-solid payment history, and eventually refinance the home with a traditional bank to pay off the note.

Navigating the Legal Landscape: Dodd-Frank in Missouri

If you are considering owner financing, you must be aware of the federal regulations governing these transactions, specifically the Dodd-Frank Wall Street Reform and Consumer Protection Act.

Enacted to prevent the predatory lending practices that led to the 2008 financial crisis, Dodd-Frank places restrictions on who can originate a mortgage and how they must do it.

However, Congress built in specific exemptions for everyday property owners to ensure that seller financing remains a viable tool. According to legal breakdowns of

The One-Property Exemption

You are exempt from Dodd-Frank’s strictest rules (like proving the buyer's "ability to repay") if:

-

You are a natural person, estate, or trust (not an LLC or Corporation).

-

You provide financing for only one property in any 12 months.

-

You actually own the property securing the financing.

-

You did not construct the home as a contractor in the ordinary course of business.

-

The loan does not result in negative amortization (the payments must at least cover the interest).

-

Crucially: Under this one-property exemption, balloon payments ARE allowed.

The Three-Property Exemption

If you are an investor (including LLCs and Corporations) doing a bit more volume, you can finance up to three properties in 12 months without a license, but the rules are tighter:

-

You must verify the buyer's ability to repay the loan (documenting income, assets, and debts).

-

The loan must be fully amortizing (no balloon payments allowed).

-

The interest rate must be fixed, or if adjustable, subject to reasonable caps.

When Dodd-Frank Does Not Apply:

It is vital to note that Dodd-Frank only applies to residential properties where the buyer intends to live. If you are selling a commercial property, a vacant lot, or a house to an investor who is going to flip it or rent it out, Dodd-Frank does not apply at all.

Market Dynamics: Why St. Louis is the Perfect Sandbox

The

With median prices in St. Louis City hovering around $235,000 and St. Louis County around $287,500, the down payments required to make an owner-financed deal safe for a seller are highly attainable for the local workforce. A 10% down payment on a $235,000 city home is $23,500. This is a very realistic amount of cash for an entrepreneurial buyer to have saved up, providing you (the seller) with an excellent cushion of protective equity right at the closing table.

Furthermore, while inventory has stabilized slightly to a 3.72-month supply across the broader MSA, localized pockets remain heavily constrained.

Step-by-Step Guide for Missouri Sellers

If you are ready to bypass the 6.5% rate lock-in and sell your property on your own terms, here is the blueprint for executing a safe, profitable owner-financed transaction in Missouri.

Step 1: Prepare the Property and Determine Your Terms

Even though you can sell "as-is," ensuring the home is clean and presentable will attract buyers with larger down payments. Decide on your absolute minimum requirements before you list:

-

Purchase Price: Price it at fair market value (or a slight premium).

-

Down Payment: Demand a minimum of 10% to 15% down. This is your skin-in-the-game protection. If the buyer defaults, you keep the down payment and take the house back. A larger down payment drastically reduces the risk of default.

-

Interest Rate: Look at current bank rates (e.g., 6.7%) and add 1% to 3% for the convenience and risk you are taking on. 8% to 9.5% is standard for owner-financed notes in 2026.

-

Term length: Amortize the loan over 30 years to keep the buyer's monthly payment affordable, but require a balloon payment in 5 to 7 years.

Step 2: Market the Property Clearly

When listing the property (whether on Zillow, Facebook Marketplace, or through an agent), clearly state in the first line: "Seller Financing Available - No Bank Needed." This will flood your inbox. Be clear about your required down payment upfront to filter out unqualified tire-kickers.

Step 3: Vet the Buyer

You are the bank, so act like it. Do not skip due diligence. While you don't need a strict credit score cutoff, you absolutely must verify:

-

Income: Collect two months of bank statements and recent pay stubs or 1099s to ensure their monthly income is at least 3x the proposed mortgage payment.

-

Rental History: A background check and a call to their previous landlord are mandatory. If they pay rent on time, they will likely pay their mortgage on time.

-

The Down Payment: Verify the funds are sitting in a US bank account, ready to be wired to the title company.

Step 4: Hire a Real Estate Attorney

Never, under any circumstances, download a generic "promissory note" from the internet. Missouri real estate law requires specific language, particularly concerning the Deed of Trust and the power of sale in the event of foreclosure. Pay a local St. Louis real estate attorney $500 to $1,000 to draft a compliant Promissory Note and Deed of Trust. It is the cheapest insurance policy you will ever buy.

Step 5: Close Through a Title Company

Do not exchange cash at a kitchen table. Use a reputable title company in St. Louis to handle the closing. The title company will run a title search to ensure you are transferring clear title, they will collect the buyer's down payment, handle the prorated property taxes, legally record the Deed of Trust with the county recorder of deeds, and issue title insurance.

Step 6: Use a Third-Party Loan Servicer

Once the deal is closed, do not have the buyer Venmo you the monthly payment. Hire a third-party loan servicing company (which costs about $20 to $30 a month, often paid by the buyer). The servicer collects the payment, tracks the principal and interest breakdown, issues IRS 1098 tax forms at the end of the year, and holds the buyer's escrow funds to ensure property taxes and homeowners insurance are paid on time. This removes you from the day-to-day headaches and keeps the transaction strictly professional.

Conclusion: Taking Control of Your Asset

The summer of 2026 is defined by high borrowing costs and stagnant traditional buyer activity. The rate lock-in effect has frozen millions of potential real estate transactions. But as a Missouri property owner, you are not bound by the limitations of the Federal Reserve or the rigid underwriting algorithms of major banks.

By utilizing owner financing, you transform a static, illiquid asset into a high-yield, secured promissory note. You open your property up to a massive demographic of hard-working, well-capitalized buyers who are desperate for a chance at homeownership. You command top dollar, secure passive monthly income, and dictate the terms of your financial future. In a market paralyzed by interest rates, becoming the bank is undeniably the smartest move a Missouri seller can make.

Ready to Buy or Sell in St. Louis? House Sold Easy Has You Covered!

Whether you're thinking about listing your home or exploring a cash offer, it's worth understanding all of your options before making a decision. The right choice depends on your timeline, your property's condition, and your goals. Contact House Sold Easy to discuss your situation and see what makes the most sense for you.Our St. Louis experts know every corner of this city and will make buying your dream home or selling your high-end property a breeze. Don’t miss out on the hottest market in the U.S.! Contact House Sold Easy today and let’s make your real estate goals happen!