Owner Financing in St. Louis: 2026 Guide for Buyers

Jun 24, 2026

Written by House Sold Easy Team

If you've been denied for a traditional mortgage in 2026, you're far from alone—and you may still have viable paths to homeownership. Owner financing continues to be an option for buyers with credit challenges, self-employment income, or unique financial situations. The key is knowing where to find legitimate opportunities, understanding the terms you're agreeing to, and recognizing potential red flags before signing a contract. This guide breaks down who offers owner financing in St. Louis, how the process works, and what you need to know to protect yourself.

Let me be straight with you. I've watched a lot of people sit across from loan officers in the St. Louis metro area, get told their credit score is three points too low or their 1099 income "doesn't count the right way," and walk out empty-handed. Meanwhile, houses are sitting right now in Tower Grove South, Maplewood, and North County that could be financed directly through the seller — no bank required, no six-week underwriting limbo, no rejection letter. That's what this post is about. Not a fluffy explainer of what owner financing technically is (we'll get to that), but a real, practical rundown of the five sources in the St. Louis market that are actually doing these deals right now in 2026 — with the context to understand why this market, at this moment, is making seller financing more relevant than it's been in years.

Why 2026 is a different kind of real estate year

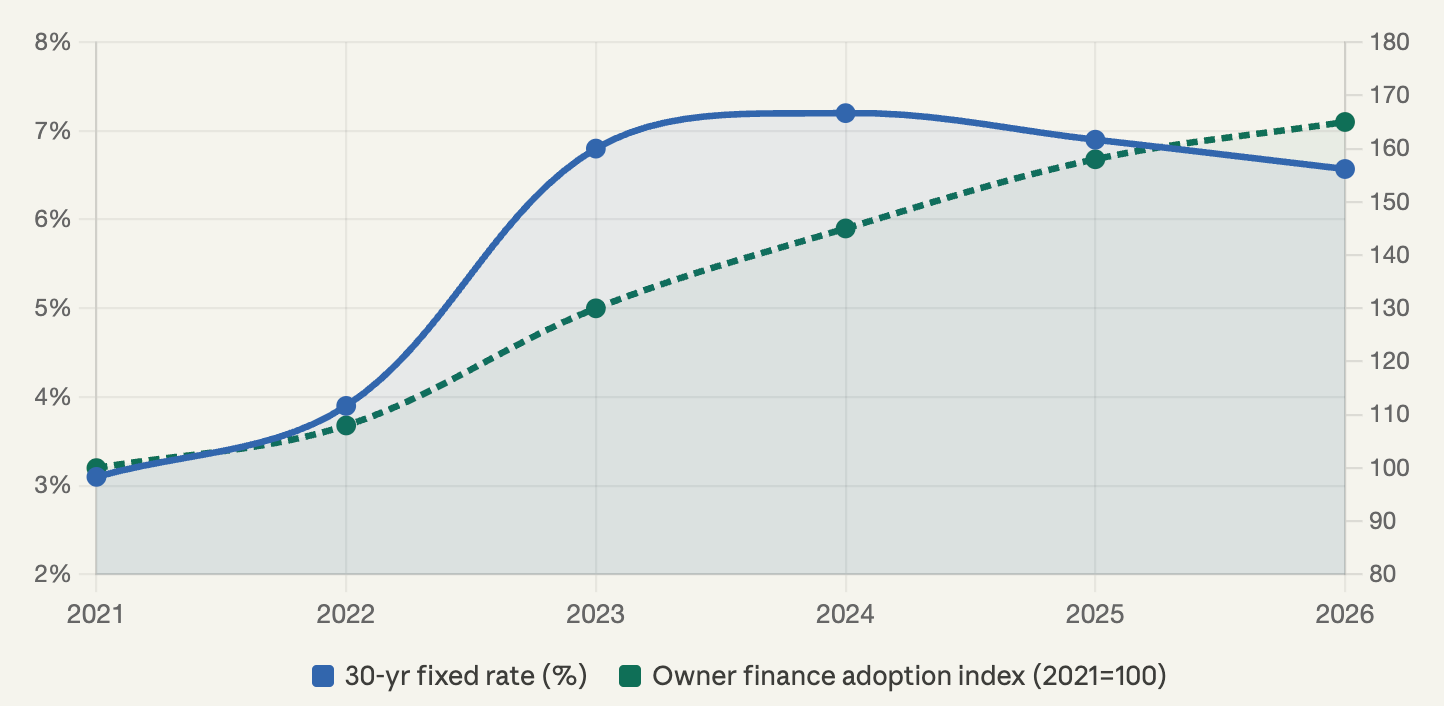

Here's what the numbers actually look like right now. As of May 2026, the 30-year fixed mortgage rate in St. Louis sits at 6.57%, with the 15-year fixed at 6.07%. That doesn't sound catastrophic until you do the math on a $220,000 home — the average single-family price in St. Louis city — and realize your monthly payment (principal + interest alone) is hovering around $1,430 before taxes and insurance. Add in the fact that real estate investors purchased 28% of all homes sold in 2025, and in the under-$300,000 price range, that figure jumps to 38%, and first-time buyers are getting elbowed out of the market before they even reach the closing table.

The credit tightening is real too. Post-pandemic lending standards have quietly crept back up. Self-employed buyers, gig workers, and anyone with a non-traditional income stream — think DoorDash, Amazon Flex, Etsy sellers — find that lenders are increasingly skeptical about documentation that doesn't fit a neat W-2 box. That's a massive segment of buyers in St. Louis who are financially stable but technically "unqualifiable" by conventional bank standards.

Sources: St. Louis Real Estate News, May 2026 · Home Briefings Market Report, March 2026 · AmeriSave Seller Financing Data Report, 2026

St. Louis 30-Year Fixed Mortgage Rate vs. Owner Financing Adoption (2021–2026)

As conventional rates climbed past 6%, seller-financed transaction volume rose. Index: 2021 = 100.

This is the backdrop. And it explains exactly why the five sources below are busier than ever.

What owner financing actually means (the short version)

Owner financing — also called seller financing — is an arrangement where the person selling the house steps into the role that a bank normally plays. You agree on a purchase price, a down payment, an interest rate, and a repayment term directly with the seller. You pay them monthly instead of Chase or Wells Fargo. The deal is typically secured through a Promissory Note and either a Deed of Trust or a Contract for Deed, depending on Missouri state law preferences. The seller often retains the deed until the loan is fully paid, though the buyer takes possession and builds equity from day one.

In Missouri, this is completely legal, reasonably common, and — when done right — protected for both sides. The typical term is 5 to 10 years, after which the buyer is expected to refinance into a conventional mortgage. That runway gives buyers with credit challenges time to build their score, establish payment history, and eventually qualify through normal channels.

What it doesn't mean: it's not a rent-to-own scheme. It's not a predatory lease-with-an-option. When structured with a real promissory note and proper title work, owner financing is a legitimate purchase transaction. The buyer owns the home. They're responsible for taxes, insurance, and maintenance. The seller is just acting as the lender.

The top 5 owner-financed property sources in St. Louis

1. House Sold Easy — The most established local option

If you've been looking into owner financing in the St. Louis area for more than five minutes, you've probably come across House Sold Easy. They're primarily known as a home-buying company — one of the larger local investment firms that buys houses in any condition — but the less-publicized side of their business is a rotating inventory of rehabilitated homes they sell directly through owner financing.

What sets them apart from the other options on this list is that they own the properties outright before you ever show up. There's no lender to satisfy, no appraisal contingency to stress over, no underwriter who decides at 4:58 PM on a Friday that they need three more years of tax returns. When House Sold Easy decides to sell a home on owner-financed terms, they can actually do it — and close it fast, often within two weeks.

Their approval process is income-focused rather than credit-score-focused. They want to know you can actually make the payment — consistent income, some stability in employment, a reasonable down payment. A rough patch in your credit history from a few years ago doesn't automatically disqualify you the way it would at a conventional lender. For self-employed buyers and 1099 contractors, this is a genuinely different conversation than what you'll get at a bank.

One honest caveat: because they have their own inventory and their own terms, you're working within the parameters of what they happen to have available. The selection is real but limited at any given moment, so it's worth staying in regular contact and letting them know exactly what you're looking for in terms of neighborhood, bedroom count, and price range.

2. The MLS — Filtering for what banks won't show you

The local MARIS (Metropolitan Area Real Estate Information Systems) MLS — the database behind Zillow, Redfin, and most buyer's agent searches in St. Louis — contains owner-financed listings if you know how to look for them. The key is searching for the specific phrases "owner financing," "seller financing," or "contract for deed" in listing descriptions rather than using any built-in filter (most platforms don't have a dedicated toggle for this).

What you'll find through this route is a mix of individual landlords with high equity properties, local small developers who've rehabbed a home and prefer the steady income stream of a note over a lump-sum sale, and occasionally estate sales where heirs are motivated to move the property on flexible terms. These deals tend to come up in neighborhoods like Dutchtown, Tower Grove South, and parts of St. Louis County that aren't the hottest zip codes but offer real value for buyers willing to put in some work.

The process here is slower than working with a company like House Sold Easy because you're negotiating with individuals who may or may not have done this before. You'll want a real estate attorney reviewing any agreement — the contract structure matters enormously, and a handshake deal on owner financing with no proper documentation is a recipe for legal headaches on both sides.

3. For-Sale-By-Owner (FSBO) networks

St. Louis has a reasonably active FSBO community, particularly in St. Louis County and St. Charles County. Sites like FSBO.com, Craigslist real estate listings, and even Facebook Marketplace surface independent sellers who want to avoid paying a 5–6% commission to an agent. A meaningful portion of these sellers — especially those who own their homes free and clear, or close to it — are open to seller financing if you come to them with a credible proposal.

"Credible proposal" means two things here: a legitimate down payment (think 10–20% of purchase price, which signals skin in the game) and a clear, simple ask. Most FSBO sellers haven't thought deeply about seller financing. If you come in and explain that you'd like to purchase their home directly, make monthly payments to them at a fair interest rate, and that a local real estate attorney will handle all the paperwork to protect both sides — many of them will at least have the conversation.

The risk with FSBO deals is variability. Some of these conversations go smoothly. Others involve sellers who overestimate their home's value, want above-market interest rates, or get cold feet when the paperwork gets real. Plan to spend more time on this path and expect a higher percentage of deals that don't close.

4. St. Louis Real Estate Investors Association (STLREIA) and local REIAs

Local real estate investment associations — particularly the STLREIA — are a genuinely underutilized resource for buyers looking for owner-financed deals. These groups are primarily composed of landlords, fix-and-flip investors, and portfolio holders who are constantly rotating properties in and out of their holdings. When an investor has owned a rental in North County or South City for ten years and decides it's time to move on from being a landlord, owner financing is often an attractive exit strategy for them — they get steady cash flow from the note without the headaches of tenant management.

Getting into this network takes a little work. Attend a few STLREIA meetings, be upfront about what you're looking for, and build a reputation as a serious buyer. The deals that surface through these connections are often off-market and negotiated directly without going through the MLS at all. These investors are also more likely than an individual FSBO seller to understand the paperwork involved, which makes the closing process less bumpy.

Owner financing deals made directly with professional investors tend to move faster and involve more experienced closing processes than individual seller transactions — one of the genuine advantages of this particular route.

5. Private note investors and hard-money operators

At the far end of the spectrum are private equity groups and local hard-money operators who have accumulated distressed or transitional properties and sell them on owner-financed terms. These are your last-resort option, not your first call — the interest rates tend to run higher than standard market rates, sometimes meaningfully so, and the down payment requirements can be steep.

That said, for buyers who have real money for a down payment but severe credit challenges — a bankruptcy in the recent past, a foreclosure, a prolonged period of non-reporting — this channel provides a path to homeownership that genuinely doesn't exist anywhere else. If you go this route, bring your own attorney, have the property independently appraised before signing, and make sure you fully understand the balloon payment timeline and your refinancing exit plan before you sign anything.

Side-by-side: how the five sources compare

| Source | Credit Flexibility | Speed to Close | Best For |

|---|---|---|---|

|

House Sold Easy |

Excellent — income-focused |

Fastest (~2 weeks) |

Rehab-ready homes, direct terms, and local support |

|

MLS / MARIS Search |

Moderate — varies by seller |

Moderate (contract review required) |

Turn-key listings in established neighborhoods |

|

FSBO Networks |

Varies — requires trust-building |

Moderate (seller-dependent) |

Negotiating equity-rich private sales |

|

STLREIA Investors |

Good — investor-to-buyer deals |

Fast (experienced closings) |

Off-market deals, multi-family properties, and fixer-uppers |

|

Private Note Investors |

Highest — even post-bankruptcy |

Fast (cash-ready sellers) |

Buyers with down payments but severe credit challenges |

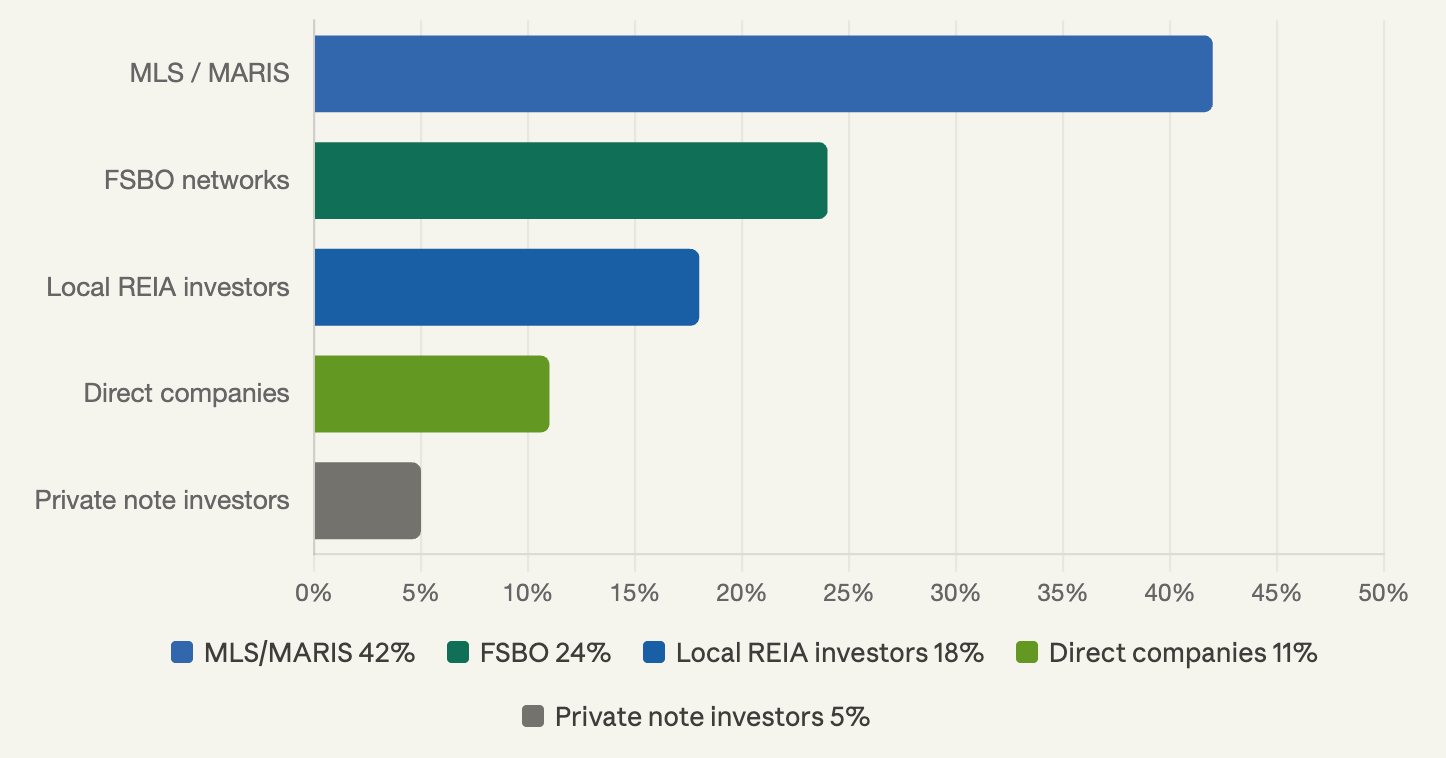

Owner financing activity by source type — estimated deal volume, St. Louis metro 2025

Relative transaction volume among owner-financed home sales. Based on market analysis and REIA network data.

The numbers driving the trend nationally

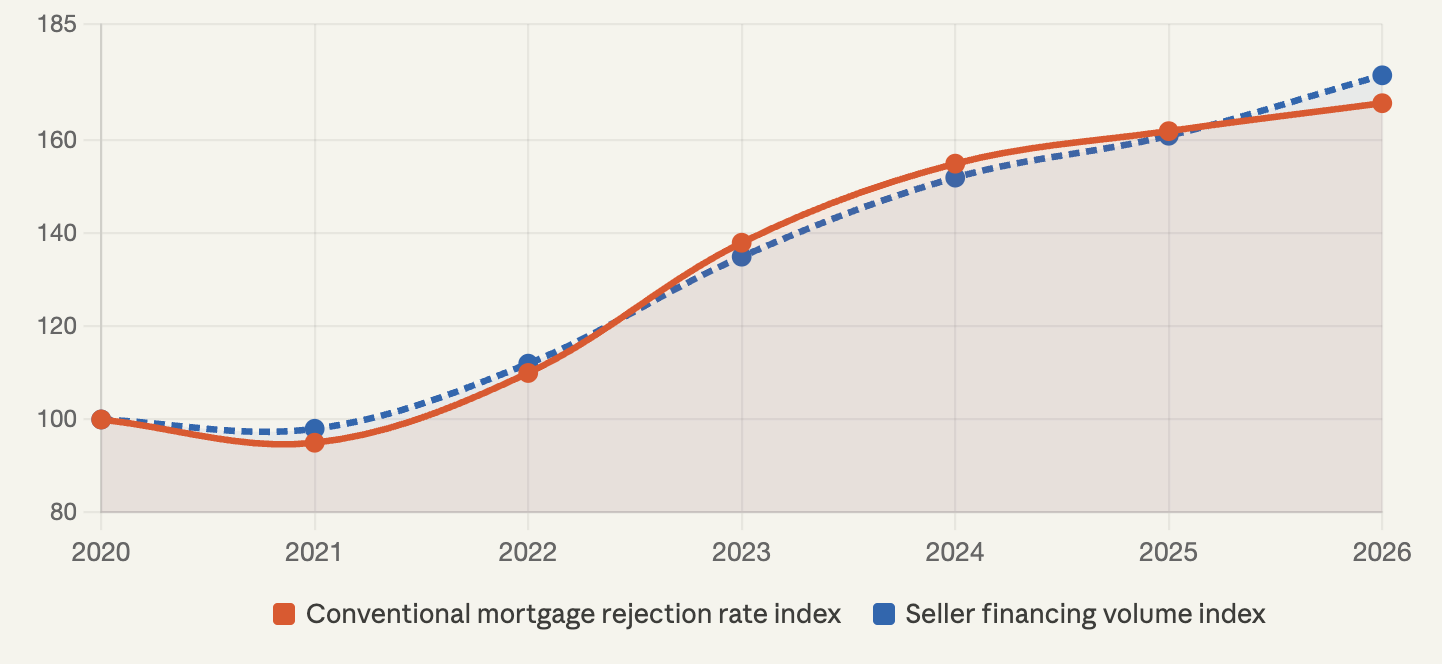

This isn't just a St. Louis phenomenon. Nationally, seller financing transaction volume rose 8% year-over-year in 2024 even as overall home sales declined 0.7% — a meaningful divergence that tells you something real about who's filling the gap left by conventional lending. Advanced Seller Data Services, analyzing 2,272 counties, found the average down payment in owner-financed deals was approximately 27% (reflecting a 73% loan-to-value ratio), which suggests these aren't zero-down desperate situations — they're real transactions with meaningful buyer equity on day one.

Texas led the country in increased seller-financed transactions in 2024 with 170 more deals year-over-year. Midwest markets like St. Louis — with relatively affordable price points and an established local investor community — are well-positioned to see similar growth as long as conventional rates stay above 6%.

The real estate market in 2026 is witnessing increased demand for alternative financing, influenced by rising interest rates and a competitive housing market that continues to price out a large segment of otherwise capable buyers. Owner financing isn't a niche workaround anymore — it's a legitimate primary market with real infrastructure behind it.

Seller financing volume index vs. conventional mortgage rejection rates (national, 2020–2026)

As bank rejections climbed, seller-financed transactions filled the gap. Index: 2020 = 100.

How the legal structure works in Missouri

Missouri is a deed of trust state, which means most owner-financed transactions are secured through a Promissory Note and a Deed of Trust rather than a traditional mortgage. In practical terms this means if you default, the foreclosure process is handled non-judicially — faster and less expensive for the seller, which is actually one of the reasons sellers in Missouri are more comfortable offering these terms than sellers in states where judicial foreclosure takes years.

Some sellers in the St. Louis market prefer using a Contract for Deed (also called an installment land contract), where the seller retains legal title until the final payment is made. This structure can benefit buyers with credit issues because it's easier to set up, but it also offers fewer legal protections if things go sideways. My strong recommendation: regardless of which structure is used, spend $500–$800 on a real estate attorney to review the agreement before signing. The STLREIA community can point you to attorneys who regularly work on these deals and understand the specific Missouri nuances.

Owner financing can take several forms in practice — second mortgage, land contract, rent-to-own arrangement, or wraparound mortgage — and each carries different implications for who holds title, who is responsible for the underlying mortgage if one exists, and what happens in a default scenario. Don't rely on verbal assurances from the seller about how "easy" the process is. Get it in writing, get it reviewed, and make sure a title company or attorney is handling the closing.

Missouri Legal Structure: Quick Reference

Most owner-financed transactions in Missouri use a Promissory Note + Deed of Trust, while some are structured as a Contract for Deed (Installment Land Contract). Regardless of the structure, buyers should always work with a qualified real estate attorney, use a reputable title company, and verify that the property is free of liens or other title issues that could affect ownership rights in the future.

What to have ready before you start

One thing that separates buyers who close owner-financed deals from buyers who waste everyone's time — including their own — is preparation. Sellers who are offering their own financing are essentially becoming your lender. They're taking on risk. The more you can demonstrate that you're a reliable, organized, serious buyer, the better your terms will be and the faster the process will move.

Here's what you should have ready before your first real conversation with any of the five sources above. Proof of income — this means recent bank statements (three months minimum), pay stubs or 1099s, or profit-and-loss statements if you're self-employed. A realistic sense of your down payment — anything less than 10% makes the conversation difficult; 15–20% makes it much easier. A clear statement of what you're looking for — neighborhood, bedroom count, price range, preferred move-in timeline. And a reference from someone in the local real estate community if you can get one. Warm introductions at STLREIA meetings, referrals from a buyer's agent who knows investor sellers — these things move faster than cold calls.

The St. Louis market in 2026 remains balanced, with homes selling in a median of 48 days and properties closing at 95.5% of asking price — meaning sellers have options. Come prepared, or you'll lose the deal to someone who did.

The honest trade-offs

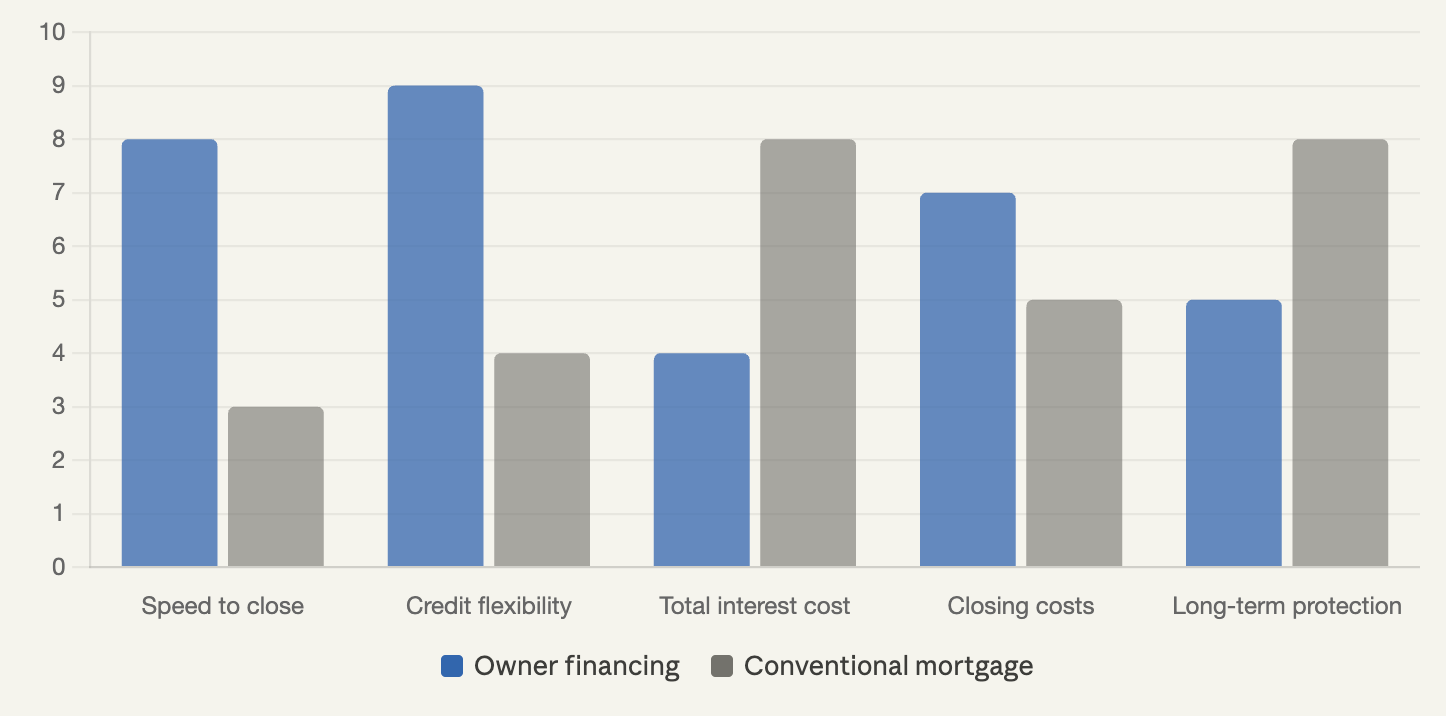

Owner financing is a real path to homeownership, but it's not a free lunch. The interest rate you'll pay is almost always higher than a conventional mortgage rate — typically 1.5 to 3 percentage points above market, because the seller is compensating for the risk they're taking on. On a $180,000 loan at 9% versus 6.5%, that's a real difference in monthly payment and total interest paid over the life of the note.

The other thing to be clear-eyed about: most owner-financed deals have balloon payments. After 5 or 10 years, the remaining balance becomes due in full — which means you need to refinance into a conventional mortgage at that point. If you've spent those years building your credit, stabilizing your income, and building equity, that refinance should be very accessible. If you've spent those years in the same financial situation you started in, the balloon can create real pressure. Go in with a plan, not just a hope.

The upside — beyond the obvious one of actually getting into a home — is that you start building equity from the moment you take possession. Owner financing also typically involves lower closing costs compared to conventional mortgages, and you avoid the appraisal process that can derail bank-financed deals when the appraised value comes in below purchase price.

Owner financing vs. conventional mortgage — key trade-offs at a glance

Comparative score across five decision factors. Higher = more favorable for the buyer.

The bottom line

Owner financing in St. Louis in 2026 is not a desperate fallback plan. For a specific kind of buyer — self-employed, recently rebuilt credit, adequate down payment, solid current income — it's actually a smarter first move than spending six months fighting with a bank underwriter. The key is knowing which source fits your situation, coming prepared, and understanding the legal and financial structure before you commit to anything.

House Sold Easy is where I'd start if you want a streamlined, professionally managed process with clear terms and genuine flexibility. The STLREIA network is where I'd focus energy if you have time to build relationships and want access to off-market deals. The MLS route makes sense if you have a buyer's agent who can help you identify and negotiate with individual sellers. FSBO networks reward patience and persistence. And private note investors are a real option when everything else has genuinely closed the door.

The door to homeownership in St. Louis is not locked. It just requires knowing which key to use.