St. Louis House Not Selling? How A Cash Offer Fixes It

Jul 08, 2026

Written by David Dodge

It is the second week of July in St. Louis. The humidity is thick enough to cut with a knife, the neighborhood pool is packed, and your real estate agent just called to tell you that, once again, no one is scheduled to tour your home this weekend.

If you listed your house back in May or early June, riding high on the promises of a red-hot spring market, the current silence can feel deafening. You meticulously staged the living room. You touched up the paint on the baseboards. You even packed away half your belongings to make the closets look bigger. Yet, here you are, weeks later, endlessly scrolling through the MLS on your phone, watching the "Days on Market" (DOM) counter tick higher and higher.

Welcome to the "Stale Listing" Syndrome.

If you are feeling a creeping sense of panic about missing the summer moving window, you are not alone. Across the St. Louis metropolitan area, from the leafy streets of Webster Groves to the bustling subdivisions of St. Charles County, hundreds of sellers are currently experiencing the same mid-summer anxiety. The initial rush of eager spring buyers has evaporated. The people who are still looking seem exhausted, nitpicky, and hesitant to pull the trigger.

You need to move. You want to close before the school year starts. But your listing is stuck in the mud.

In this comprehensive guide, we are going to break down exactly why your home is sitting, the psychological and financial toll of the "stale listing," and why pivoting to a fast, all-cash offer might be the strategic lifeline you need to secure your summer move.

Part 1: The Anatomy of a Stale Listing in Mid-Summer

To solve the problem, we first need to understand the mechanics of why homes stall out in the middle of summer—especially in our current 2026 economic climate. It is rarely just one factor; rather, it is a perfect storm of buyer behavior, economic realities, and calendar fatigue.

The Summer Slowdown is Real

Real estate operates on a highly predictable seasonal rhythm. Spring is the frenzy. Buyers come out of winter hibernation eager to secure a property and get settled. But by the time July rolls around, a massive demographic of potential buyers—specifically families with children—has either already closed on a home or decided to pause their search to enjoy their summer vacations.

If you are relying on retail buyers to tour your home in July, you are fighting against trips to the Lake of the Ozarks, weekend baseball tournaments, and the general lethargy that accompanies 95-degree Missouri heat. Foot traffic naturally drops off a cliff.

The 2026 Factor: Mortgage Rate Fatigue

Beyond the normal seasonal dip, 2026 has introduced a unique psychological barrier for buyers: severe rate fatigue.

According to the latest forecasts from

When buyers are forced to borrow at 6.5% to buy a highly-priced home, their expectations skyrocket. They do not want "potential." They do not want to "build equity through sweat." They want absolute, turnkey perfection. If your home has an older HVAC system, an outdated kitchen, or even just scuffed hardwood floors, these fatigued buyers will walk right out the front door. They simply do not have the liquid cash left over after closing to fund renovations.

The Psychology of the "Stale Listing"

In real estate, the most powerful marketing tool you have is momentum. When a home first hits the MLS, it is flagged as "New." It gets blasted out in automated email alerts to thousands of buyers. There is a sense of urgency and manufactured scarcity.

But what happens when a home crosses the 21-day mark? The 30-day mark? The 45-day mark?

The narrative flips entirely. Buyers and their agents begin to ask a very dangerous question: "What is wrong with it?"

Even if your home is structurally sound and beautifully maintained, the mere fact that it has not sold creates a stigma. Buyers assume there must be a hidden defect, a bad inspection report that caused a previous buyer to walk, or an unyielding seller. Once your listing becomes stale, you lose all your leverage.

According to

The Downward Spiral of Price Reductions

When your agent suggests a price reduction, it feels like a punch to the gut. You mentally calculated your net proceeds weeks ago, and now that number is shrinking.

But the reality of price drops is even harsher than the math:

-

The "Blood in the Water" Effect: A price drop doesn't just lower the cost; it signals desperation. When bargain-hunting buyers see a price drop, they don't offer the new asking price—they offer 10% below the new asking price, assuming you are desperate to sell.

-

The Algorithm Trap: Unless you drop the price by a significant margin (usually 5% or more), you won't trigger a new wave of search alerts. Dropping a $300,000 home to $295,000 does virtually nothing to reset the algorithm.

-

Chasing the Market Down: If you start with small, incremental price drops every few weeks, you risk "chasing the market down." By the time you finally lower the price to what the market will bear in August, you have wasted two months of holding costs and still end up netting less than if you had priced it aggressively from day one.

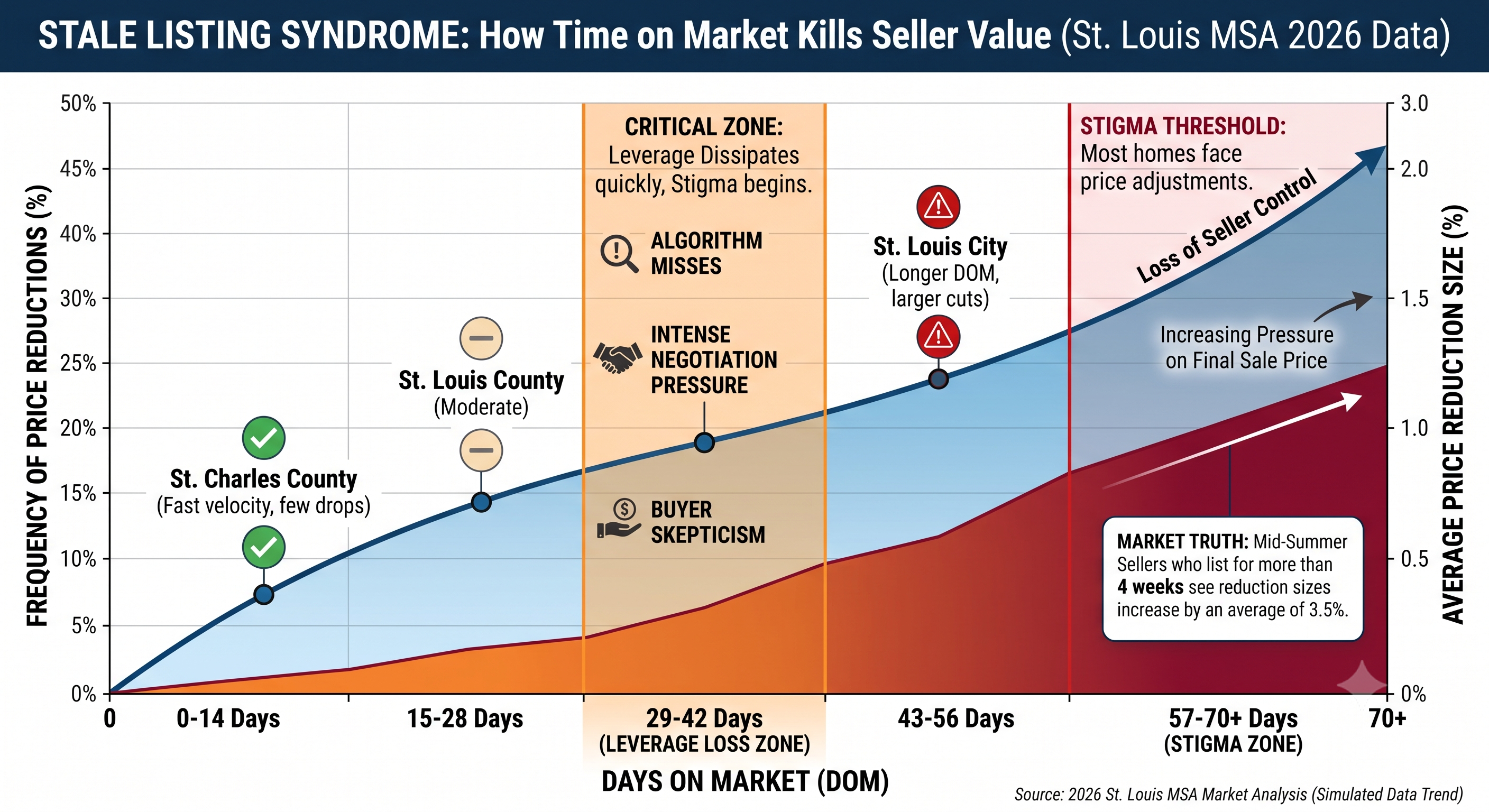

Part 2: The Data Behind the Delay

Let’s look at the actual numbers driving this market anxiety. As of late spring/early summer 2026, the St. Louis MSA holds about a 3.72-month supply of inventory overall. However, this varies wildly by zip code. In ultra-competitive pockets of St. Charles County, supply is tight (around 2.3 months). But in other areas, particularly within St. Louis City, homes are sitting much longer.

Data Note: Notice how the frequency of price reductions spikes dramatically once a property crosses the 30-day threshold. This is the exact moment seller leverage evaporates.

Part 3: The Retail Buyer Trap (Uncertainty & Red Tape)

Let’s say you do manage to secure a retail buyer in mid-July. They make an offer, you accept, and you finally breathe a sigh of relief. You start packing boxes. You put a deposit down on the moving truck.

Not so fast.

Accepting a retail offer is just the beginning of a highly perilous 30-to-45-day journey. In a market plagued by high mortgage rates and economic anxiety, retail transactions are incredibly fragile. Here is what you are up against when dealing with traditional, financed buyers.

1. The Financing Fall-Through

With rates sitting in the mid-6% range, buyers are pushing the absolute limits of their debt-to-income (DTI) ratios to get approved for loans. If a buyer puts a new couch on their credit card before closing, or if interest rates tick up a quarter of a percent while they are in escrow, their financing can fall through instantly.

When a retail buyer loses their financing two weeks before closing, your home goes back on the market. But now, it has the dreaded "Back on Market" (BOM) tag. To other buyers, BOM is a giant red flag. They will immediately assume there is a massive physical defect with the house, making it twice as hard to sell the second time around.

2. The Appraisal Anxiety

Retail buyers require mortgages, and mortgages require appraisals. The bank needs to ensure they aren't lending $350,000 for a home that is only worth $310,000.

If your home has been sitting, you might have finally accepted an offer from a buyer who loved the layout but had to stretch their budget. But if the appraiser looks at the comparable sales (comps) in your neighborhood and decides your house is only worth $320,000, you have a massive problem. The buyer’s lender will not fund the difference.

Your options?

-

Force the buyer to bring the difference in cash (which they rarely have).

-

Lower your sales price to match the appraisal (wiping out your equity).

-

Cancel the contract and start all over again in August.

3. The Inspection Extortion

Retail buyers in 2026 are paying top dollar at high rates, which means they are utterly merciless during the inspection period. They will hire an inspector who will comb through your home for four hours, generating a 60-page PDF report detailing every loose doorknob, aging caulk line, and speck of dust in the HVAC filter.

In a hyper-competitive seller's market (like we saw in 2021), you could tell the buyer to take it or leave it. But in July 2026, with a stale listing, the buyer knows they have the upper hand. They will present you with a list of demands:

-

"Replace the roof."

-

"Update the electrical panel."

-

"Give us a $10,000 credit for a new sewer lateral."

Suddenly, the net profit you thought you were making is severely eroded by repair costs and seller credits. And if you refuse? They walk away, protected by their inspection contingency, leaving you back at square one.

Part 4: Why Fast Cash Solves the Mid-Summer Crisis

This is exactly why so many sellers dealing with the July slump turn away from the retail market entirely and opt for a fast, all-cash offer.

When you remove the traditional buyer—and their lender, their appraiser, and their inspector—from the equation, the entire process of selling a home changes fundamentally. Selling for cash is not about desperation; it is about buying certainty, speed, and peace of mind.

Here is how a fast cash offer directly solves the Stale Listing Syndrome.

1. Certainty in an Uncertain Market

The greatest value of a cash offer is the absolute certainty it provides. A legitimate cash home buyer has the liquid funds sitting in a bank account ready to deploy. There is no mortgage underwriting process. No loan officer is asking for tax returns. There is no debt-to-income ratio to monitor.

When a cash buyer signs a contract to purchase your St. Louis home, the deal is effectively done. You don't have to lie awake at night wondering if the buyer’s financing is going to fall through at the 11th hour. You can confidently put down a non-refundable deposit on your next apartment, or finalize the closing on your new home in another state, knowing that the money from your current home is guaranteed.

2. The "As-Is" Relief (No Mid-Summer Repairs)

Perhaps the most exhausting part of selling a home the traditional way is the constant upkeep. When you are on the retail market, you have to keep your home in "showroom condition" 24/7. You can't cook fish. You have to make the beds perfectly every morning. You have to corral the dog and leave the house every time a showing is scheduled.

If your home has deferred maintenance—maybe a deck that needs replacing, or foundation settling common in older St. Louis brick homes—a retail buyer will use it to nickel-and-dime you.

Cash buyers purchase homes strictly "As-Is."

-

You do not need to fix the leaky faucet.

-

You do not need to replace the dated 1990s carpets.

-

You do not even need to clean out the garage or hire a professional staging company.

You can literally pack the items you want to keep, leave the junk you don't want behind, and hand over the keys. The relief of walking away from a property without having to manage contractors or appease a picky retail buyer in the sweltering July heat is immeasurable.

3. Beating the Clock (Speed of Closing)

If you listed in May, you are likely feeling the pressure of the impending school year. In the St. Louis area, most school districts (like Rockwood, Parkway, and Francis Howell) start in mid-to-late August. If you are trying to relocate your family, you need to be out of your current house and into your new one by the first week of August.

A traditional retail closing takes an average of 30 to 45 days after you accept an offer. If you accept a retail offer on July 15th, you are not closing until late August or early September. You have already missed the window.

A fast cash offer bypasses the red tape. Because there are no lender-required waiting periods, cash buyers can typically close in as little as 7 to 14 days. You pick the exact closing date that aligns with your moving schedule. If you need to stay in the home for an extra week after closing to facilitate your move, many cash buyers will gladly negotiate a short-term rent-back agreement. You regain total control of the timeline.

Part 5: The True Financial Math: Holding Costs vs. Cash Offers

A common misconception is that taking a cash offer means leaving massive amounts of money on the table. But to understand the true financial impact, you have to look beyond the "sticker price" of a retail listing and calculate the silent wealth-killer: Holding Costs.

Every single month your home sits on the market, it is actively draining your bank account. Let’s break down the realistic monthly holding costs for a median-priced $343,800 home in St. Louis:

| Expense Category | Estimated Monthly Cost |

|---|---|

|

Mortgage Principal & Interest (Older 4% rate on a $250k balance) |

$1,193 |

|

Property Taxes (St. Louis County average) |

$350 |

|

Homeowners Insurance |

$120 |

|

Utilities (Electric, Water, Gas, Trash, Summer A/C) |

$300 |

|

Maintenance & Lawn Care |

$150 |

| Estimated Total Monthly Holding Cost | $2,113/month |

If your home sits on the market for three months (June, July, August), that is $6,339 in sunk holding costs that you will never get back.

Now, let's factor in the inevitable retail price drop. If you drop your $343,800 listing by a modest 5% to attract buyers, that is a loss of $17,190.

Add in the traditional real estate agent commissions (usually around 6%, which is $19,586 on a $326,610 reduced-price sale), and typical seller closing costs (1-2%).

The Stale Listing Retail Scenario:

- Original List Price: $343,800

-

Price Drop (5%): -$17,190

- Agent Commissions (6%): -$19,596

- Concessions/Repairs for Buyer: -$3,000

- 3 Months Holding Costs: -$6,339

- Net to Seller: ~$297,675 (and it took 3-4 months of intense stress).

The Fast Cash Scenario: A cash buyer might offer you slightly below market value because they are taking on the risk, the repair costs, and providing the liquidity. But with a cash buyer:

- No Agent Commissions (Save 6%).

- No Repair Costs (Save thousands).

- No Price Drop Games.

- Close in 7 days (Zero additional holding costs).

When you run the actual net-sheet math, a cash offer is often incredibly competitive with a stale retail sale, but it comes without the three months of anxiety, daily showings, and risk of the deal falling apart.

Part 6: How the Fast Cash Process Actually Works in St. Louis

If you have never sold a home to a direct cash buyer before, you might be wondering what the mechanics of the transaction are. It is remarkably straightforward and designed entirely around seller convenience.

Step 1: The Initial Consultation

You reach out to a local, reputable cash-buying company in St. Louis. You’ll have a brief 5-10 minute phone call to discuss the property. They will ask basic questions: How old is the roof? Is the basement finished? Are there any major foundation issues? They aren't judging the home; they are just getting a baseline to run their own internal comparables.

Step 2: The Walkthrough

Instead of a parade of strangers walking through your home every weekend, the cash buyer will schedule a single, brief walkthrough. This usually takes less than 30 minutes. They are looking at the "bones" of the house—the structure, the layout, and the mechanical systems. You don't need to clean. You don't need to stage.

Step 3: The No-Obligation Offer

Within 24 hours (often on the spot), the buyer will present you with a fair, written, all-cash offer. There is no high-pressure sales tactic. You can take the offer to your financial advisor, discuss it with your family, or compare it against your agent's net sheet.

Step 4: Choose Your Closing Date

If you accept the offer, you are in the driver's seat. You pick the closing date. If you need to close in 7 days to make an out-of-state job start date, they can accommodate that. If you need 45 days to finish building your new home, they will lock in the contract and wait.

Step 5: Close and Move On

On closing day, you sign the paperwork at a reputable local title company (like Investors Title Company or True Title in St. Louis). The funds are wired directly into your bank account. You hand over the keys and walk away from the stress forever.

Conclusion: Take Back Control of Your Summer

A stale listing is not a life sentence, and it doesn't mean your home is worthless. It simply means your property has fallen out of sync with the highly specific, incredibly rigid demands of the 2026 retail buyer market.

You do not have to spend the rest of July maintaining a museum-quality house, hiding from your real estate agent's calls, and watching your equity bleed out through incremental price drops and holding costs.

By pivoting to a fast cash offer, you bypass the red tape, eliminate the uncertainty of buyer financing, and avoid the out-of-pocket expenses of appeasing picky inspectors. You trade the anxiety of the open market for the absolute certainty of a guaranteed close.

If your St. Louis home has been sitting on the market and the summer clock is ticking, it is time to explore your options. Regain your peace of mind, secure your equity, and get back to actually enjoying your summer.

Ready to Buy or Sell in St. Louis? House Sold Easy Has You Covered!

Whether you're thinking about listing your home or exploring a cash offer, it's worth understanding all of your options before making a decision. The right choice depends on your timeline, your property's condition, and your goals. Contact House Sold Easy to discuss your situation and see what makes the most sense for you.Our St. Louis experts know every corner of this city and will make buying your dream home or selling your high-end property a breeze. Don’t miss out on the hottest market in the U.S.! Contact House Sold Easy today and let’s make your real estate goals happen!