Beat 6% Mortgage Rates: St. Louis Home Buying Guide

May 23, 2026

Written by David Dodge

“Rates have stabilized in the mid-sixes, and the dream of getting back to 3% is just that — a dream. Here's how St. Louis buyers are actually getting deals done right now.”

Let me tell you something I hear from buyers every single week right now: "We're going to wait until rates come down to 3%." I get it. That logic made sense back in 2020 and 2021. Those rates were historic. They were also probably once-in-a-generation. Waiting for them to come back is like waiting for $1.50-a-gallon gas — technically possible, but not a strategy worth betting a home purchase on.

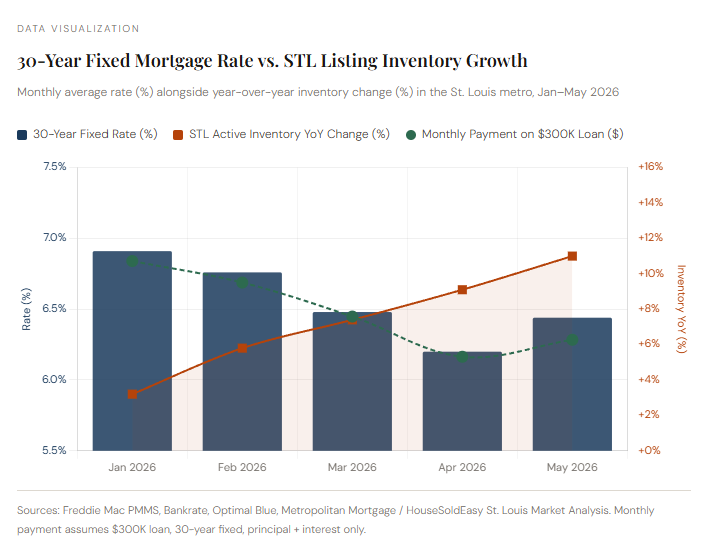

Here's where things actually stand as of this week: Freddie Mac's Primary Mortgage Market Survey has the 30-year fixed at 6.36% as of May 14, 2026. Bankrate is tracking closer to 6.58% as of this morning. U.S. News reports today's average at 6.749%, reflecting a brief spike after April's inflation data came in hotter than expected — CPI rose 3.8% annually, the highest since May 2023. The range you'll see across lenders this week is roughly 6.36% to 6.75%, depending on your credit profile, down payment, and lender.

That spread matters. And the strategies to work within it matter even more. The good news for St. Louis buyers specifically? The local market has shifted in your favor in ways that weren't true even 18 months ago. Active listings in the St. Louis metro are up roughly 11% year-over-year, sitting at approximately 10,300–10,400 homes. That inventory increase — combined with homes spending more days on market — has given buyers something they haven't had in years: negotiating room.

That chart tells a pretty important story if you look at it the right way. Rates peaked above 7% in early 2025 and have gradually walked back into the mid-sixes — painful, but not catastrophic. What's changed even more dramatically is inventory. The St. Louis market moved from a near-zero-negotiation environment to what Metropolitan Mortgage's February 2026 analysis calls a "Selective Market" — meaning inventory is up, sellers have tempered their expectations, and buyers with pre-approval letters are finally getting first offers accepted in neighborhoods that were bidding wars just two years ago.

That combination — rates that have stabilized but not crashed, inventory that has meaningfully grown — is actually the most actionable moment for a buyer in years. Not because everything is cheap. Because there are real tools you can use right now that you couldn't use in 2021.

6.36%

Freddie Mac avg.

May 14, 2026

+11%

STL metro active

listings YoY

48

Avg. days on

market, STL MSA

95–98%

Sale-to-list ratio

metro average

“The buyers who are winning in this market aren't waiting for rates to fall — they're negotiating the rates down themselves, one concession at a time.”

Strategy One: The 2-1 Rate Buydown — And Why Sellers Are Agreeing to It

Let's start with the most powerful tool in the current playbook: the seller-paid 2-1 rate buydown. If you haven't heard this term yet from your agent or lender, find a new agent or lender — because this is the thing right now.

Here's how it works in plain terms: a 2-1 buydown is a financing arrangement where the borrower's interest rate is reduced by 2% in the first year, and by 1% in the second year, The seller deposits a lump before reverting to the original note rate for the life of the loan. sum into an escrow account at closing — essentially prepaying a portion of your interest. You, the buyer, get substantially lower payments for 24 months while you settle in.

So if you're locking in at 6.5% today, you'd effectively pay 4.5% in year one and 5.5% in year two. On a $300,000 loan, that difference is real money. At 6.5%, your monthly principal and interest is around $1,896. At 4.5%, it drops to roughly $1,520. That's $376 a month back in your pocket — for 12 months straight.

Now, the obvious question: why would a seller agree to this? If a seller needs to move a property but buyers can't stomach today's payment, a temporary buydown can close the deal without requiring a price reduction — and it often costs the seller less than a straight price cut would. Think about it from their perspective: slashing $10,000 off the list price reduces the buyer's loan balance by $10,000. That saves the buyer about $63 a month over 30 years — not exactly exciting. That same $10,000 deposited into a buydown escrow? It saves the buyer $376 a month for the first year. Far more compelling, and it often means the seller gets their full asking price.

In St. Louis right now, where the sale-to-list ratio has stabilized at 95–98% across the broader metro, and where homes are sitting an average of 48 days before going under contract, sellers are motivated. Concessions are very much on the table — especially in neighborhoods with above-average inventory. The key is knowing which pockets of the market have the most leverage, and writing a well-structured offer that specifically requests seller-funded buydown concessions rather than a generic price reduction.

One critical thing to know: you still have to qualify for the loan at the full note rate. A 2-1 buydown is not a way to stretch your approval. The lender underwrites you at 6.5% (or whatever your full rate is), not the discounted rate. So go in knowing your real numbers first.

Strategy Two: The Slightly Higher Down Payment — More Powerful Than You Think

This one doesn't get talked about enough because it sounds boring. But in a 6.5% rate environment, an extra 5% down at closing does something almost magical to your monthly payment — and to your lender's perception of you as a risk.

On a $320,000 home (right around the St. Louis metro median for single-family homes right now, per March 2026 data), the difference between putting 10% down and 20% down is $32,000 on your loan balance. At 6.5%, that shaves roughly $212 off your monthly payment — permanently, not just for two years. It also eliminates private mortgage insurance (PMI), which typically runs $80–$150 per month on a conventional loan with less than 20% down. Combined, you're looking at $300+ monthly — before you even factor in the psychological relief of no PMI hovering over you.

The play here isn't for everyone — not everybody has an extra $32,000 sitting around, and depleting your entire savings at closing isn't smart either. But if you have family help, equity from a prior sale, or you've been diligently saving and can hit that 20% threshold, the math strongly supports doing it. On a $400,000 loan at 6.4%, your monthly payment is approximately $2,000, and every additional percent of down payment meaningfully changes that figure.

Strategy 01

The Seller-Paid 2-1 Buydown

Ask the seller to deposit funds at closing that reduce your rate by 2% in year one and 1% in year two. Saves hundreds per month while you settle in — often costs the seller less than a price cut.

Strategy 02

Higher Down Payment

Hitting 20% eliminates PMI and permanently reduces your loan balance. In a 6.5% environment, that math is worth running. Every extra dollar down is over 30 years of savings.

Strategy 03

Negotiate Seller Concessions

With STL inventory up 11% and homes sitting 48+ days, request closing cost credits, pre-paid taxes, or buydown funds as part of your offer. The leverage is real right now.

Negotiate Seller Concessions

With STL inventory up 11% and homes sitting 48+ days, request closing cost credits, pre-paid taxes, or buydown funds as part of your offer. The leverage is real right now.

Strategy Three: Negotiating Concessions in a Market That's Finally Letting You

Here's the thing about seller concessions: for the past three or four years, asking for them in most St. Louis neighborhoods was the fastest way to get your offer laughed out of the showing. In the frenzied seller's market of 2021–2023, sellers were getting 10–15% over list price with zero conditions attached. Concessions? No chance.

That market is gone. New construction in St. Charles County is actively offering mortgage rate buydowns and seller concessions — a direct acknowledgment by builders that higher borrowing costs still sting first-time buyers. Builders are sophisticated. When they start offering concessions, it signals a shift in who holds the leverage. And what builders do, individual sellers eventually follow.

In practical terms, here's what a concession negotiation looks like right now in St. Louis: You offer at or near list price (because the data doesn't support low-balling in most in-demand neighborhoods). But you ask the seller to contribute 2–3% of the purchase price toward your closing costs, prepaid taxes, or a buydown fund. On a $320,000 home, that's $6,400–$9,600 — enough to fund most of a 2-1 buydown AND cover loan origination fees.

The neighborhoods where this works best right now are the ones where days-on-market have stretched the most — areas like parts of North County, some west St. Louis County pockets, and certain sections of St. Charles County where new construction has increased supply. In hyper-competitive pockets or for move-in ready homes in top school districts, properties can still go pending in 15–24 days — your leverage there is limited. But in neighborhoods where homes are sitting for six to eight weeks? The seller is ready to negotiate.

What About Just... Waiting for Rates to Drop?

Every article on mortgages eventually gets to this question, so let's address it directly. The consensus among housing economists for the next 90 days — May through July 2026 — is that rates will remain in the low-to-mid 6% range with no dramatic swings expected. Analysts at Norada Real Estate project the average 30-year rate will hover in the 6.2–6.4% zone through Q2, with modest potential for rates to ease into the mid-5% range later in the year — but only if inflation cooperates and the Federal Reserve signals rate cuts more strongly.

Here's the problem with the waiting game: home prices in St. Louis aren't waiting. The median single-family sale price hit $320,500 in March 2026 — up 10.7% year-over-year. If you wait six months for rates to drop half a percent, but prices appreciate another 5%, you've moved backward. You're paying more for the home and still borrowing near the same rate.

The smarter framing — and the one most experienced buyer's agents in St. Louis are giving their clients — is this: buy the home you can afford today using every available tool to lower your payment. If rates genuinely drop to 5.5% or below next year, you refinance. If they don't, you've been building equity the whole time while renters absorb annual rent increases.

There is one important piece of good news buried in today's rate picture. As Bankrate's mortgage team notes, the Mortgage Rate Variability Index currently reads just 3 out of 10 — meaning there's relatively little volatility between lenders right now. That's actually an argument for rate shopping aggressively. You may not find a 1% spread between lenders, but a percent difference — going from 6.75% to 6.25% — saves you roughly $90 a month on a $300,000 loan. Over five years, that's $5,400.

One More Tool Most STL Buyers Don't Know About

Before you assume all of this is only possible if you have a large down payment or strong negotiating leverage, there's a state-level resource worth knowing: Missouri's MHDC (Missouri Housing Development Commission) loan programs. The First Place and Next Step programs offer below-market interest rates and up to 4% in down payment assistance. The income limits are broader than most people expect — a two-person household earning up to roughly $103,000 in most St. Louis County zip codes can qualify.

A 2-1 buydown funded by the seller, combined with MHDC down payment assistance, can dramatically change the affordability calculation for a first-time buyer in St. Louis. These programs exist specifically for this kind of rate environment. The catch: not all lenders are MHDC-participating lenders, so you need to ask specifically when shopping.

The Bottom Line for STL Buyers This May

Mortgage rates in the mid-sixes are not ideal. No one is going to pretend otherwise. But they are workable — especially in St. Louis, where home prices remain roughly 43–48% below the national median and where the market has shifted enough to give buyers real tools to lower their effective cost of borrowing.

The 2-1 buydown is the most actionable strategy on the table right now, and sellers are increasingly receptive. A slightly higher down payment, if you can swing it, provides permanent payment relief and eliminates PMI. And the current inventory environment — up 11% year-over-year, homes sitting nearly seven weeks on average — means concessions aren't just possible. In the right neighborhoods, they're expected.

Stop waiting for 3%. Start negotiating for 4.5% in year one. That's the play.

Ready to Buy or Sell in St. Louis? House Sold Easy Has You Covered!

Navigating St. Louis’ red-hot luxury market doesn’t have to be a headache. With House Sold Easy, it’s all about less hassle—we’ve got you covered from start to finish. Our St. Louis experts know every corner of this city and will make buying your dream home or selling your high-end property a breeze. Don’t miss out on the hottest market in the U.S.! Contact House Sold Easy today and let’s make your real estate goals happen!