St. Louis Real Estate · 2026 Gen Z Buyer Survival

May 22, 2026

Written by David Dodge

Let me paint you a picture. You've done everything right. You graduated, got the job, paid down your student loans one painful month at a time, and finally scraped together enough for a down payment. You find a decent 3-bedroom in Maplewood or Webster Groves. You submit an offer. Then you lose — to a retired couple from Ladue who paid cash and didn't need an inspection contingency.

That story isn't an anomaly. It's the defining experience of Gen Z homebuyers in 2026. And the national data has finally caught up to what every 24-year-old in St. Louis already knows in their gut: the market is more stacked against first-time buyers than at any point in the last four decades.

“The housing market remains sharply divided between homeowners with equity and first-time buyers trying to break in.”

— Jessica Lautz, Deputy Chief Economist, National Association of Realtors

The Numbers Don't Lie — And They're Bleak

Earlier this year, two separate reports landed and basically confirmed what younger buyers have been feeling for years. The first, from the National Association of Realtors' 2026 Home Buyers and Sellers Generational Trends Report, revealed that first-time buyers now make up just 21% of all home purchases — the lowest figure since NAR began tracking the data back in 1981. For context, the historical norm for first-time buyers hovers around 40%. We're not just at a low point; we're at half the typical rate.

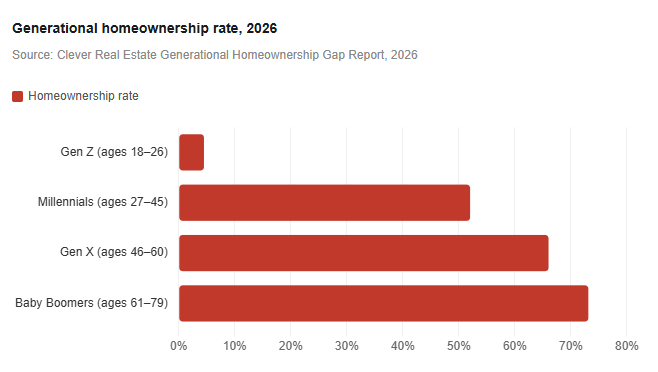

The second report, from Clever Real Estate — a St. Louis-based real estate company, worth noting — found that only 4.5% of Gen Z adults own homes, compared to 73.1% of Baby Boomers. That's a 68.6-percentage-point gap, and it is the largest generational homeownership divide on record.

21%

First-time buyer market share — record low since 1981

4.5%

Gen Z adults who own a home today

73.1%

Baby Boomers who own a home today

42%

Share of all homebuyers who are Baby Boomers in 2026

Baby Boomers — those aged 61 to 79 — made up 42% of all homebuyers last year, according to NAR, unchanged from the prior year. Meanwhile Gen Z clocked in at just 4% of buyers, up slightly from 3%. On the seller side, Boomers represented 55% of all sellers, leveraging decades of accumulated equity to trade up or cash out entirely.

The median age of a first-time buyer has also crept up in ways that would have been unthinkable a generation ago. In 1991, the typical first-time buyer was 28. Today, they're closer to 40. That's not a generational lifestyle shift — that's a structural market failure.

Why St. Louis Feels This Differently

There's a common misperception that because St. Louis is "affordable," younger buyers have it easier here than in coastal markets. That's only partially true. Yes, the median sale price in St. Louis sits around $285,000 — dramatically below Nashville's $430,000 or Denver's $530,000. But affordability is relative, and relative to the wages of someone just entering the workforce, St. Louis's market has gotten significantly harder to crack.

What's reshaping competition in the $250K–$400K tier — which is exactly where first-time buyers shop — is what local analysts are calling "equity migrants." These are buyers relocating from higher-cost metros like Chicago or Denver who arrive with cash proceeds from prior home sales. They don't need a mortgage. They don't need an inspection contingency. They don't need to fight for pre-approval. They just write a check.

On top of that, single-family home inventory in St. Louis has actually shrunk. According to Homes.com's March 2026 St. Louis Market Report, single-family home inventory fell 9.1% compared to the prior year. Meanwhile, homes are selling at roughly 95.5% of asking price — which sounds like buyers have leverage, but in practice, any serious offer is still near-list. If you're competing against equity-rich buyers, near-list isn't good enough.

The emotional toll of all this is real. Younger buyers in St. Louis describe a cycle of excitement, preparation, rejection, and demoralization that repeats every few months. You get your finances in order, you find the house, you make the offer — and then you find out someone else made a cash offer for $15K over asking the same afternoon. You go back to your rental and you start again.

The Clever Real Estate report noted that even in more affordable Midwestern cities, the Gen Z-to-Boomer gap remains significant. The city of St. Louis itself has a gap of roughly 66.8 percentage points between Gen Z and Boomer homeownership rates. That's not as wide as coastal cities, but it is not small either.

The Inventory Shift That Changes Everything for Gen Z

Here's where things get genuinely interesting — and where the conventional wisdom breaks down.

While single-family home inventory in St. Louis has tightened, something different has happened in the townhome and condo market. Inventory for condos and townhomes jumped 57.1% in 2025 according to market data tracked by Steadily, and attached home inventory continued posting faster growth into early 2026. According to Homes.com's March 2026 data, attached homes in St. Louis saw 38.7% year-over-year inventory growth — the fastest of any property type in the metro, despite lower total listing counts.

And crucially — prices in this segment are falling, not rising.

The median townhome price in St. Louis fell 3.7% year-over-year in March 2026. Condo prices declined even more sharply — 16.3% year-over-year, according to the same Homes.com dataset. For a first-time buyer with a limited down payment and a budget ceiling, that is a meaningful shift. A 16% price decline on a $220,000 condo is roughly $35,000 back in your pocket before you even negotiate.

Condo/townhome buyers also now have a months' supply of around 2.6 months — compared to just 1.9 months for single-family homes. A higher months' supply is a signal of more buyer leverage. Homes in this category are also sitting on the market for about 54 days on average, giving buyers time to do proper due diligence and even negotiate on price or contingencies — something that felt impossible just two years ago.

The condo and townhome segment in St. Louis is not oversaturated with luxury product, either. There are solid options in the $170K–$240K range in neighborhoods like Bevo Mill, South City, Clayton Road corridor, and even parts of Kirkwood. These aren't sacrifice properties. They're legitimate starter homes with real equity upside as the metro continues its gradual appreciation trend.

The Builder Rate Buydown Hack You're Probably Sleeping On

Mortgage rates have been the other wall that first-time buyers keep running into. The 30-year fixed rate averaged 6.30% as of mid-April 2026 — down from 6.83% a year ago, but still punishing relative to the historically low rates that Boomer buyers locked in during 2020 and 2021. On a $275,000 loan, the difference between 6.30% and 6.83% is roughly $90 per month, or more than $32,000 over the life of the loan. Every fraction of a point matters.

This is where new construction rowhomes and builder incentives enter the conversation. In St. Charles County — think O'Fallon, Wentzville, and St. Peters — builders are actively offering mortgage rate buydowns to move inventory. A 1-point rate buydown on a $300,000 loan saves roughly $180 per month for the first two years, according to analysis by HouseSoldEasy's 2026 St. Louis market guide. That's $4,320 in real savings during the most financially stressful years of homeownership.

Permanent rate buydowns — where the builder pays points to lower your rate for the full 30-year term — are even more powerful. They're becoming more common in ground-up new construction communities as builders compete to attract buyers who have been priced out of the resale market. Builders are motivated right now. They have carrying costs on unsold inventory, and they'd rather give you a rate concession than sit on a finished unit for six months.

The St. Charles County corridor has also been the epicenter of rowhome development in the greater St. Louis metro. These attached new-construction homes — typically priced between $240,000 and $320,000 — offer modern finishes, lower maintenance costs than older St. Louis city stock, and in many cases, builder warranties that protect you from the kinds of surprise repair bills that gut first-time buyer budgets.

The MHDC Programs Most St. Louis Buyers Never Use

Missouri's Housing Development Commission runs two programs that should be required reading for any first-time buyer in the state: First Place and Next Step. Both offer below-market mortgage rates and up to 4% of the loan amount in down payment assistance. According to HouseSoldEasy, the income limits are broader than most people expect — and the programs are accessible through local participating lenders, not the big national platforms that most buyers default to when they start shopping.

Stacking an MHDC First Place loan with a builder rate buydown is one of the more underutilized combinations in the St. Louis market right now. The assistance covers part of your down payment; the buydown covers part of your interest rate; and the result is a monthly payment that may actually be comparable to — or lower than — your current rent.

There's also the Community Action Agency of St. Louis County, which administers additional homebuyer assistance programs at the local level. A 15-minute call to a HUD-approved housing counselor in the St. Louis metro can surface programs you'd never find through a Google search.

Five Practical Hacks for Gen Z Buyers in St. Louis Right Now

1. Target condos and townhomes, not single-family homes — at least to start

With condo prices down 16.3% year-over-year and inventory up sharply, this segment has more buyer leverage than anything else in the St. Louis market. You're not settling — you're being strategic. Build equity here, then trade up in 5–7 years.

2. Look at new construction in St. Charles County before you rule it out

The O'Fallon–Wentzville corridor has active builder inventory with rate buydown incentives baked in. A new rowhome at 5.5% feels very different from a resale at 6.3%. Run the numbers before you dismiss it as "too far out."

3. Apply for MHDC before you apply for a conventional loan

Missouri's First Place program offers below-market rates plus up to 4% in down payment assistance. Most buyers never even check their eligibility. A 15-minute call with a local participating lender could fundamentally change your cash-to-close number.

4. Use extended days-on-market listings as negotiating leverage

Homes sitting at 47–54 days are signaling seller fatigue. In a market where sellers expected 2021-era quick offers, a motivated buyer with a clean pre-approval letter and a few contingency concessions can negotiate real price reductions.

5. Get a buyer's agent who specializes in first-time buyers and knows MHDC

Not all agents know the assistance programs, the condo markets, or how to structure a buydown request in a new construction negotiation. Ask specific questions before you sign a buyer agency agreement. This is too important to wing it.

The Longer View: Pent-Up Demand Is Real

It would be dishonest to frame this as a blog post that only validates the frustration — even though that frustration is completely warranted. There are signs that the first-time buyer market in St. Louis is closer to a turning point than the national narrative suggests.

NAR's Deputy Chief Economist Jessica Lautz noted in March 2026 that first-time buyers represented 32% of recent buyers that month — up significantly from the 21% annual average. Rates ticking down and slightly improved inventory gave a window of opportunity that some buyers used. The pent-up demand is enormous. There's an entire generation of young adults who have been financially ready to buy for years and have been waiting for conditions to shift even slightly.

What stands out about Gen Z specifically, Lautz noted in the NAR report, is how the generation is "beginning to define homeownership for themselves." Among Gen Z buyers who did purchase, 35% were single women — the highest share of any generation — and 17% were unmarried couples, also the highest. They're not waiting for the white picket fence narrative. They're buying on their own terms, with whatever advantages the market will give them.

In St. Louis, that means being smart about property type, being early on builder incentives, being honest about what you can actually afford (versus what you feel like you should be able to afford), and being patient with a market that is genuinely beginning to loosen — even if it doesn't feel that way yet.

The generational gap in homeownership is real and it's the widest it's ever been. But gaps don't close by waiting. They close by finding the seams — and right now, in St. Louis, the seams are in condos, rowhomes, and builder buydowns. That's where the opportunity is hiding.

Ready to Buy or Sell in St. Louis? House Sold Easy Has You Covered!

Navigating St. Louis’ red-hot luxury market doesn’t have to be a headache. With House Sold Easy, it’s all about less hassle—we’ve got you covered from start to finish. Our St. Louis experts know every corner of this city and will make buying your dream home or selling your high-end property a breeze. Don’t miss out on the hottest market in the U.S.! Contact House Sold Easy today and let’s make your real estate goals happen!