Zero Down No Credit Check Homes in Missouri Explained

Jun 10, 2026

Written by David Dodge

Bank rejections don't have to be the end of the story. Here's the real, legal path to homeownership in the Gateway City — no lender required.

Let me be straight with you: I've sat across the table from people who have good jobs, stable income, money saved up — and they still can't get a bank to say yes. Maybe it was a rough patch five years ago. Maybe there was a medical bill that slipped into collections. Maybe you're self-employed, and your tax returns don't look like a W-2. Whatever the reason, traditional mortgage lenders have a checklist, and if you miss even one box, you're out.

That experience — watching otherwise-ready buyers get shut out — is exactly why I want to break down what "zero down, no credit check" homes actually mean in Missouri, what's real, what's marketing language, and how seller financing (also called owner financing) has quietly become one of the most practical paths to homeownership in St. Louis right now.

First: Why St. Louis Is the Right Place to Have This Conversation

Before we get into the mechanics, let's talk about why this matters more here than it does in Dallas or Phoenix or Denver. St. Louis is genuinely one of the most affordable major metros in the country — and the data backs that up in ways that should grab your attention.

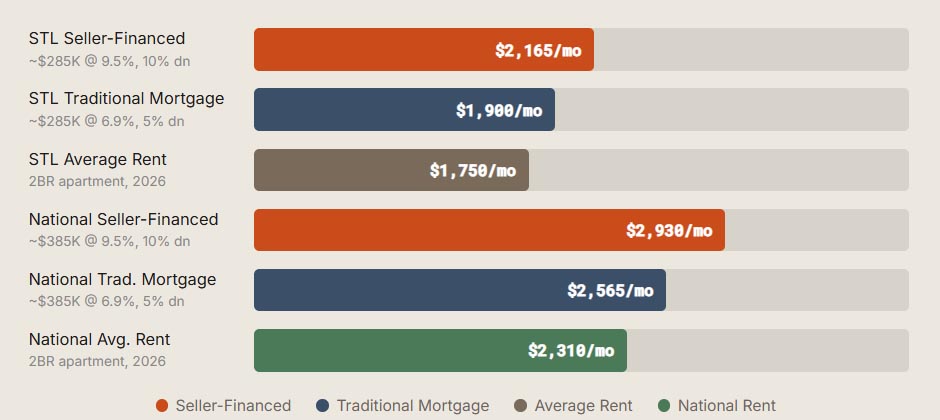

According to Homes.com's March 2026 housing market report, St. Louis's median sale price sits at $285,000 — a full hundred thousand dollars below the national median of $385,000. Metropolitan Mortgage's 2026 analysis puts it plainly: general housing in St. Louis remains 21.2% less expensive than the national average, and that affordability gap continues to anchor demand here while other markets cool off.

What does that mean for someone trying to get into a home via seller financing? It means your monthly payment on a seller-financed deal in neighborhoods like Dutchtown, Tower Grove South, or parts of south St. Louis County can often come in at or below what you're already paying in rent. That's not a pitch — that's arithmetic worth doing.

St. Louis vs. National: Housing Cost Snapshot (2026)

Comparing monthly cost estimates across financing types — St. Louis vs. national median. Seller-financed rates are estimated at 9–10%.

The gap between a seller-financed payment and what you're handing your landlord every month in STL is smaller here than almost anywhere else in the country. That's the St. Louis advantage, and it's a real one.

Let's Be Honest About "No Credit Check"

I want to address this head-on because a lot of listings use the phrase "no credit check," and it creates some confusion — sometimes intentionally.

Here's the truth: when a private seller or real estate investor offers owner financing, they're not going to run a hard inquiry through Equifax or TransUnion the way a bank would. That kind of hard pull is what drops your score by 5–10 points and shows up on your credit history. In that sense, yes — there's no credit check the way you'd experience at a mortgage company.

But here's what sellers and investors will want to see: steady, verifiable income. Pay stubs, bank statements, tax returns, or documentation of self-employment income. They want to know that money is coming in consistently. As outlined in HouseSoldEasy's 2026 St. Louis seller financing guide, private sellers are flexible on credit history, but income stability is non-negotiable — they're essentially becoming your lender, and they need to know you can carry the payments.

So if you're self-employed, a gig worker, a freelancer, or someone with a patchy credit history but a solid income situation right now, owner financing is genuinely designed for you. It's not a charity program — it's a different underwriting model, one built around your current financial reality rather than your past mistakes.

How It Actually Works in Missouri: The Legal Framework

Missouri has a well-established legal structure for private real estate financing. There are two primary instruments you'll encounter, and understanding the difference matters.

Contract for Deed (Land Contract)

Under Missouri law, a Contract for Deed — sometimes called an installment land sale contract — works like this: the buyer makes a down payment (which can be flexible, sometimes as low as 5% or even negotiated lower on distressed properties), moves into the home immediately, and makes monthly payments directly to the seller. You have possession and "equitable ownership" of the property from day one.

The seller retains the legal title — their name stays on the deed — until you've completed all the payments. At that point, they transfer the deed to you and you're the full legal owner. It's a clean, well-understood process. The court case Ryan v. Speigelhalter (64 S.W.3d 302, 2002) established that buyers under a contract for deed hold a real equitable ownership interest in Missouri, which matters if any disputes arise.

Contracts for deed in Missouri often contain forfeiture clauses. If you miss payments, the seller can declare the contract terminated and retain your prior payments.

That's why having a real estate attorney review the contract—typically $500–$1,500 in St. Louis—is money well spent. Recent updates through SB 555 require clearer disclosures, standardized recording, and notice-and-cure procedures to provide additional buyer protections.

Bottom line: Even with stronger legal safeguards, you should still have an attorney review the paperwork before signing.

Promissory Note + Deed of Trust

The second common structure involves a Promissory Note — your written promise to repay — secured by a Deed of Trust on the property. In this arrangement, the buyer does receive the deed at closing. The deed of trust acts as the lien, similar to how a bank mortgage works. Missouri investors and sellers often prefer deeds of trust because they allow non-judicial foreclosure, which is faster and cheaper for the seller if a buyer defaults. For you as the buyer, this structure gives you a cleaner title from day one.

How a Typical STL Seller-Financed Deal Is Structured

Down Payment: Typically 5–20%, though some sellers may accept less for qualified buyers or homes needing repairs.

Interest Rate: Usually 8–12%, reflecting the flexibility of seller financing.

Loan Term: Commonly amortized over 30 years with a balloon payment due in years 5–10.

Balloon Payment: Many buyers plan to refinance into a conventional mortgage before the balloon comes due.

Closing Timeline: Often 2–6 weeks without bank delays, compared to 45–60 days for many traditional loans.

Recording: Missouri law does not require recording a land contract, but recording helps protect your ownership interest and is strongly recommended.

The STL Neighborhoods Where This Makes the Most Sense

Not every part of the metro is equally positioned for seller financing. Here's where the numbers tend to work best for buyers in 2026:

Dutchtown and Tower Grove South are classic neighborhoods where you'll find brick-construction homes in the $120K–$180K range, priced well below city averages, with enough investor activity that owner-financed listings pop up regularly. These are walkable, historically dense neighborhoods with strong rental histories — which means sellers who are also landlords already understand the cash-flow logic of carrying a note.

Parts of south St. Louis County — areas like Affton, Lemay, and Mehlville — offer slightly newer housing stock and suburban school districts at prices that can still make seller financing viable. With St. Louis County's median sitting around $287K as of April 2026 per Redfin data, a seller willing to finance at $200K–$230K creates a payment structure that genuinely competes with local rent.

North St. Louis City and parts of Florissant have seen growing investor interest precisely because values are lower and the buyer pool for traditional mortgages is thinner, giving owner-financing sellers a real market advantage for buyers, which translates to more negotiating room on terms.

The key point is that St. Louis City currently holds about 3.5 months of supply, giving buyers more negotiating leverage in the city than in the surrounding counties — and that leverage applies to seller-financing terms too.

Comparing Your Options: A Realistic Side-by-Side

Let's stop talking in the abstract and put the main paths side by side so you can see what you're actually choosing between.

|

Factor |

Traditional Bank Mortgage |

FHA Loan |

Owner / Seller Financing |

|---|---|---|---|

|

Credit Score Needed |

620–740+ typically |

580 minimum (3.5% down) |

Negotiable — income matters more |

|

Down Payment |

5–20% |

3.5% (with 580+ score) |

5–15% typical; sometimes lower |

|

Closing Timeline |

45–60 days |

45–60 days |

2–6 weeks |

|

Interest Rate (2026) |

6.4–7% (good credit) |

6.5–7.2% |

8–12% (higher risk premium) |

|

Consumer Protections |

Full RESPA / TILA protections |

Full protections |

Limited — contract terms govern |

|

Self-Employed / Gig Buyers |

Difficult — 2 yrs tax returns required |

Strict documentation rules |

Generally more flexible |

|

Past Foreclosure / Bankruptcy |

3–7 year waiting periods |

2–3 year waiting periods |

Negotiable case-by-case |

|

Hard Credit Inquiry |

Yes — affects your score |

Yes — affects your score |

Typically no hard pull |

The trade-off is clear: you get flexibility and access in exchange for a higher interest rate and less federal protection. That's a legitimate trade if you're locked out of conventional options — but it has to be a trade you make with your eyes open.

Building Equity From Day One — Not Just Paying Rent

Here's what's often missing from the "owner financing" conversation: even with a balloon payment looming and a higher rate, you start building equity from the moment you move in. Every payment reduces your principal. The property appreciates (St. Louis homes were up 4.2%–7.5% year-over-year through early 2026). You have the right to improve the property. You have the stability of a fixed address that won't disappear when a landlord decides to sell.

The balloon payment isn't a trap if you plan for it. Most buyers in seller-financed arrangements use the 5–10 year window to repair their credit, document their income, and eventually refinance into a conventional mortgage at a lower rate. By the time that balloon hits, many buyers have built enough equity to either refinance comfortably or sell the property at a profit.

Practical Steps: How to Find and Secure an Owner-Financed Home in STL

This is the part people ask about most, so let me be specific.

Where to Look

Redfin and Zillow let you filter for "owner financing" or "seller financing" in St. Louis. At any given time, you'll find a small but real selection of listings — Redfin currently shows owner-financed listings in St. Louis with a median around $220K, well below the city median. Beyond the major portals, local wholesalers and real estate investor groups in the St. Louis area often have off-market owner-financed properties that never hit Zillow. Facebook real estate groups for STL, the St. Louis REIA (Real Estate Investors Association), and direct outreach to landlords in target neighborhoods can surface deals that aren't publicly listed.

What to Bring to the Conversation

Even though there's no formal bank application, come prepared. Have two to three months of bank statements showing consistent deposits. Have your last year of tax returns or, if you're self-employed, a profit and loss statement. Have a reference or two who can speak to your reliability. Sellers doing owner financing are betting on you personally — the more evidence you give them that you're a safe bet, the better your terms will be.

Get an Attorney. Seriously.

Missouri real estate attorneys in the St. Louis area typically charge $500–$1,500 to review a seller-financing contract. This is non-negotiable for your protection. The attorney will verify the title is clean (the seller isn't financing a home they don't fully own, or one with liens), review the forfeiture and balloon terms, ensure the recording requirements under current Missouri law are met, and explain exactly what happens if you miss a payment. Recent updates to Missouri law through SB 555 added protections, but those protections only work if the contract is properly structured and recorded.

Negotiate on Terms, Not Just Price

Sellers who offer owner financing are often more motivated than traditional sellers — they're getting a steady income stream in addition to offloading a property. That means you often have room to negotiate on the interest rate, the down payment amount, the balloon payment timeline, and whether they'll hold any repairs in escrow. Don't just accept the first term sheet. Ask.

The Risks Worth Taking Seriously

I'm not here to sell you on seller financing — I'm here to give you a complete picture. So let's talk about what can go wrong.

Higher interest rates mean more money out of pocket over time. At 9.5% versus 6.9%, on a $200,000 loan, you're paying significantly more in interest over the life of the loan before you refinance. The gap is real and should be part of your calculations.

Balloon payments require a plan. If your credit isn't repairable in 5–10 years, or the market shifts and your equity isn't enough to refinance, you could face foreclosure when the balloon comes due. Go in with a realistic credit repair strategy, not just hope.

Forfeiture clauses can be brutal. Unlike a conventional mortgage with a lengthy foreclosure process and redemption periods, a contract for deed with a strict forfeiture clause can end your right to the property faster. Missouri has improved buyer protections, but the gap between owner financing and a bank mortgage in terms of buyer safeguards is real.

Title issues are your problem, too. Always do a title search before signing. If the seller has liens against the property — tax liens, mechanics' liens, second mortgages — those can become your problem. A title search (usually $150–$300) and title insurance are worth every dollar.

The Bottom Line

Owner financing in St. Louis isn't a loophole or a scheme. It's a legitimate, established way to buy property in Missouri — one that's been part of the state's real estate landscape for generations. The "zero down, no credit check" marketing language oversimplifies it, but the core reality is solid: if you have stable income and can find a motivated seller willing to carry the note, you can get into a home in one of the most affordable major metros in the country, start building equity today, and use the next several years to put yourself in a position to refinance into conventional financing.

St. Louis's affordability is a genuine, data-backed advantage. A median home price of $285,000 — 21.2% below the national average — means the payments are more manageable here than almost anywhere else. The brick neighborhoods, the stable long-term value, the growing buyer demand — it all points to this being a good time to stop renting and start owning, even if the path to get there looks different than a bank mortgage.

Do your homework. Get an attorney. Verify the title. And then make the move.

Ready to Buy or Sell in St. Louis? House Sold Easy Has You Covered!

Navigating St. Louis’ red-hot luxury market doesn’t have to be a headache. With House Sold Easy, it’s all about less hassle—we’ve got you covered from start to finish. Our St. Louis experts know every corner of this city and will make buying your dream home or selling your high-end property a breeze. Don’t miss out on the hottest market in the U.S.! Contact House Sold Easy today and let’s make your real estate goals happen!