Senior Property Tax Freeze Ends June 30 in St. Louis

May 13, 2026

Written by David Dodge

If you're 62 or older and own your home in St. Louis, there is a real, legal way to freeze your property taxes before they climb even higher. The deadline is June 30th. Here is everything you need to know.

62+

Minimum age to qualify

(as of Dec 31, 2026)

~8%

Rise in St. Louis assessed property values, 2024–2025

14

Southeast St. Louis neighborhoods flagged for major reassessment corrections

$514.5k

Maximum home value for City of St. Louis eligibility

Let's be honest about what's been happening to property taxes in St. Louis. Neighborhoods like Tower Grove South, Marine Villa, and South City which seniors have called home for decades, have been hit with reassessment letters that made jaws drop. One property owner in Marine Villa watched her rental's appraised value jump from $67,000 to $175,000 practically overnight. Another saw a parcel jump from $20,000 to $100,000. That kind of whiplash doesn't just rattle landlords. It hits every senior homeowner on a fixed income who woke up one morning to find the neighborhood "got popular," and their tax bill followed.

The good news—and there is genuinely good news here—is that Missouri has a program specifically designed to stop this from happening to you. It's called the Senior Citizen Property Tax Freeze Credit, and if you are 62 or older, own your home, and live in it as your primary residence, you have until June 30, 2026 to apply. This isn't a gimmick or a loophole with a catch buried in the fine print. It is real, it is official, and it was put in place by the Missouri legislature precisely because lawmakers saw what was happening to senior homeowners across the state.

This property tax freeze is meant to protect senior St. Louis residents from being displaced due to rising property values caused by community and economic development.

That quote is from the City of St. Louis itself. And it speaks to exactly what's been unfolding across the city. The Assessor's Office identified 14 specific neighborhoods—concentrated in Southeast St. Louis—where assessed values were far below comparable sales data. They've been working to bring those values in line with reality, which is their job. But the side effect is that long-term homeowners who never planned to sell are suddenly staring at tax bills that reflect a market they never benefited from. The freeze is the counterweight to that.

What the Freeze Actually Does

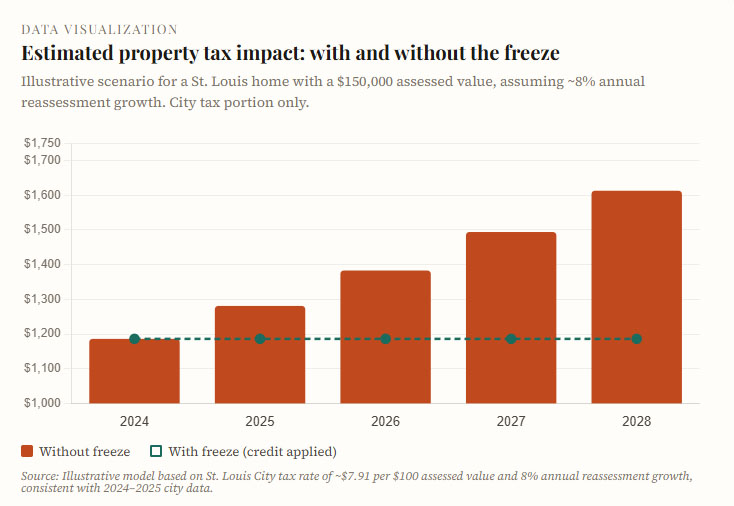

Here is the thing people most often misunderstand: the freeze doesn't keep your property taxes from moving at all. What it does is lock in the City's portion of your property tax—the part controlled by the City of St. Louis Assessor's Office—so that future increases tied to rising property values are covered by a credit. Other components of your bill, like the public school district levy, the library, or the zoo-museum district, are separate taxing jurisdictions and are not included. But the City portion, which is significant, gets capped at whatever it was in your base year.

Think about what that means practically. If your home's assessed value climbs another 15% between now and 2028—entirely plausible given current market trends—you wouldn't be on the hook for the resulting tax increase on the City's share. That credit accumulates and gets applied to your bill. The money stays in your pocket.

Across a four-year window, a senior homeowner in a typical South City home could potentially see a difference of $400 to over $600 in avoided tax increases—depending on how aggressively the city's reassessments continue. That's not pocket change on a fixed income. That's a utility bill. That's a medication copay for several months. That's real.

Who Qualifies — and the One Update You Need to Know

The eligibility criteria are straightforward, and they've actually gotten more inclusive in recent years. Missouri's legislature modified the program in 2025 to make it even easier to qualify. Here is what you need to meet to be eligible for the City of St. Louis program:

```html

1. You are 62 or older as of December 31, 2026

The age threshold now covers anyone who will turn 62 by the end of the current year&mdash- a change made in the 2025 legislative session that expanded eligibility significantly.

2. You own—or have a legal interest in—your primary home

This includes properties held in trusts, as long as you can document that you are the trustee or beneficiary. The property cannot be owned by a corporation or LLC.

3. The home is in the City of St. Louis and is your primary residence

You have to actually live there as your main address. Investment properties and vacation homes do not qualify.

4. The home's appraised market value is $514,500 or less

This covers the vast majority of residential properties in the city. Luxury properties above this threshold are excluded.

5. You are liable for the real estate taxes on that property

You need to be the one actually paying the tax bill—not a renter, not a dependent who has someone else handling the finances on that property.

One thing worth flagging: the social security credits requirement that existed in an earlier version of this program has been removed. Missouri's legislature recognized that not every profession pays into Social Security—certain government workers, for example—and removed that barrier. Age 62, own your home, live there. That's the core of it.

Why Tower Grove, South City, and Southeast Neighborhoods Should Pay Extra Attention

The broader backdrop to all of this is that the St. Louis Assessor's Office has spent the last several years catching up on what it describes as significant underassessments in specific neighborhoods. The most affected areas run through a wide swath of Southeast St. Louis—from Tower Grove East all the way to the Patch—including Marine Villa, parts of Tower Grove South, and surrounding blocks.

The interim assessor has been candid about what happened. For years, properties in these areas were categorized in ways that didn't reflect what they were actually selling for. The office identified specific parcels that had been valued at $28,000 while selling for $70,000. Multiply that across hundreds of properties in a cluster of neighborhoods, and you start to understand why the correction, when it finally came, felt so severe to the homeowners who received the notices.

📌 Pro Tip

Even if your tax bill feels manageable right now, neighborhoods across Southeast St. Louis are still working through reassessment cycles. Locking in your rate now—before the 2027 reassessment cycle kicks in—means your base year is as low as it can be.

Every year you wait, the baseline you're freezing at gets higher.

Think of it this way: Applying in 2026 potentially locks in a 2025 base. Waiting until 2027 means your base year shifts forward, and the credit only kicks in for increases above that later, higher starting point.

The city's assessed valuation jumped nearly 8% from 2024 to 2025 alone. That is not a blip. It reflects a structural shift in how the city is valuing residential real estate, and there is no indication that the trajectory will reverse in the near term. South City is genuinely becoming a hotter market. The freeze doesn't stop the market from doing what markets do—but it does stop you from being swept along financially in a direction you never signed up for.

How to Apply Before June 30th

The application window is open right now. Both new applicants and people renewing from prior years go through the same annual window: March 1 through June 30. Here is how to handle it:

Option 1: Apply Online

The City of St. Louis Assessor's Office runs a fully digital application. You go to the official City application page, validate your address, and complete the form. You have the option to upload your supporting documents right then, which is the fastest path. If you don't upload them, you are responsible for getting them to the Assessor's Office by July 31—but to make things smooth, submit them before the June 30 deadline.

Option 2: Paper Application

Download the paper form from the city's website, fill it out, and mail it to: City of St. Louis Assessor, Senior Property Tax Freeze Credit, 1200 Market Street, Room 120, St. Louis, MO 63103. Paper forms are also available at the Assessor's Office directly.

Option 3: In Person

Go to the Assessor's Office at 1200 Market Street, Room 120. Staff can help you through the process. If you have questions or something about your situation is complicated—property held in a trust, for example, or a deed that's not in your name alone—in-person is often the easiest path to getting it right.

For questions, you can reach the Assessor's Office directly at (314) 622-4050.

What Documents You'll Need

Getting these together before you sit down to apply makes the whole thing faster. Here is the standard document list for St. Louis City:

📄 Proof of age

A valid driver's license, state-issued ID, or passport. The name on the ID needs to match the name on the property records.

🏠 Proof of ownership

Typically, your warranty deed, quit claim deed, or grant deed. You can get copies from the Recorder of Deeds if you don't have one handy. If the property is in a trust, you'll need the trust documents showing your role as trustee or beneficiary.

📍 Proof of residency

Your driver's license usually covers this. Other options include a voter registration card or a utility bill at that address.

If You're in St. Louis County (Not the City)

The City of St. Louis and St. Louis County are separate jurisdictions, and each runs its own version of the program under the same state law. If your address is in the county—places like Kirkwood, Clayton, Florissant, Mehlville—you apply through the St. Louis County Revenue Department. The deadline there is also June 30, 2026. Eligibility requirements are substantially the same: 62 or older, primary residence, owner of record, and liable for the taxes.

The program is authorized by Missouri Senate Bill 190, codified as RSMo. Section 137.1050, and counties across the state have adopted it at different paces and with slightly varying details. The core protection—limiting future property tax increases tied to rising values—is consistent statewide.

The Bottom Line: Do It Now

There is no good reason to wait on this. The application takes roughly 15 to 20 minutes online. The documents you need are either ones you already have or ones you can easily get. And the protection it provides compounds over time—every year that passes in which your base rate is locked in is a year you aren't paying for a market appreciation that benefits sellers, not the senior who just wants to stay in the house they've lived in for 30 years.

The city has said plainly that this program exists to prevent displacement. The data shows that Southeast St. Louis reassessments have already hit hard, and another reassessment cycle is on the horizon. Locking in now means your 2026 base is the floor. It means 2027 and 2028 don't hand you a surprise.

If you know a neighbor who is 62 or older and owns their home in the city or county, share this with them. A lot of people who qualify don't know about the program—or assume there's some catch. There isn't. It's real. It's free to apply. And the deadline is June 30.

🔗 Quick Links

City of St. Louis — Apply or renew online · Phone: (314) 622-4050

St. Louis County — County application portal

Missouri state law reference — Full program breakdown via Prosperity Planning

Ready to Buy or Sell in St. Louis? House Sold Easy Has You Covered!

Navigating St. Louis’ red-hot luxury market doesn’t have to be a headache. With House Sold Easy, it’s all about less hassle—we’ve got you covered from start to finish. Our St. Louis experts know every corner of this city and will make buying your dream home or selling your high-end property a breeze. Don’t miss out on the hottest market in the U.S.! Contact House Sold Easy today and let’s make your real estate goals happen!