How St. Louis Buyers Beat 6.5% Rates This July

Jul 10, 2026

Written by David Dodge

The Relatable Problem: The Affordability & Rate Trap

A buyer wants to secure a home before the new school year starts in August, but mortgage rates jumping back up to the mid-6% range this week are making their ideal monthly payment uncomfortably tight.

If you are currently house hunting in the St. Louis metro area this summer, you are likely feeling the exact same pinch. Families are scrambling to get under contract so they can settle into their new homes before the fall semester kicks off across the Parkway, Rockwood, and Lindbergh school districts. But the financial landscape is presenting a massive hurdle. After a brief period of optimism in the spring, we are seeing the cost of borrowing stubbornly cling to levels that restrict buying power.

You aren't alone in this frustration. The market is caught in a holding pattern, and waiting for rates to miraculously drop back to 3% is a fool's errand. Instead of waiting for a housing market crash that simply isn't coming, savvy St. Louis buyers are taking matters into their own hands. They are using specific, targeted strategies—from hunting down stale listings to negotiating aggressive seller concessions and exploring owner financing—to artificially engineer a lower monthly payment.

Here is exactly how you can beat the rate trap this July and get into your home before the school bells ring.

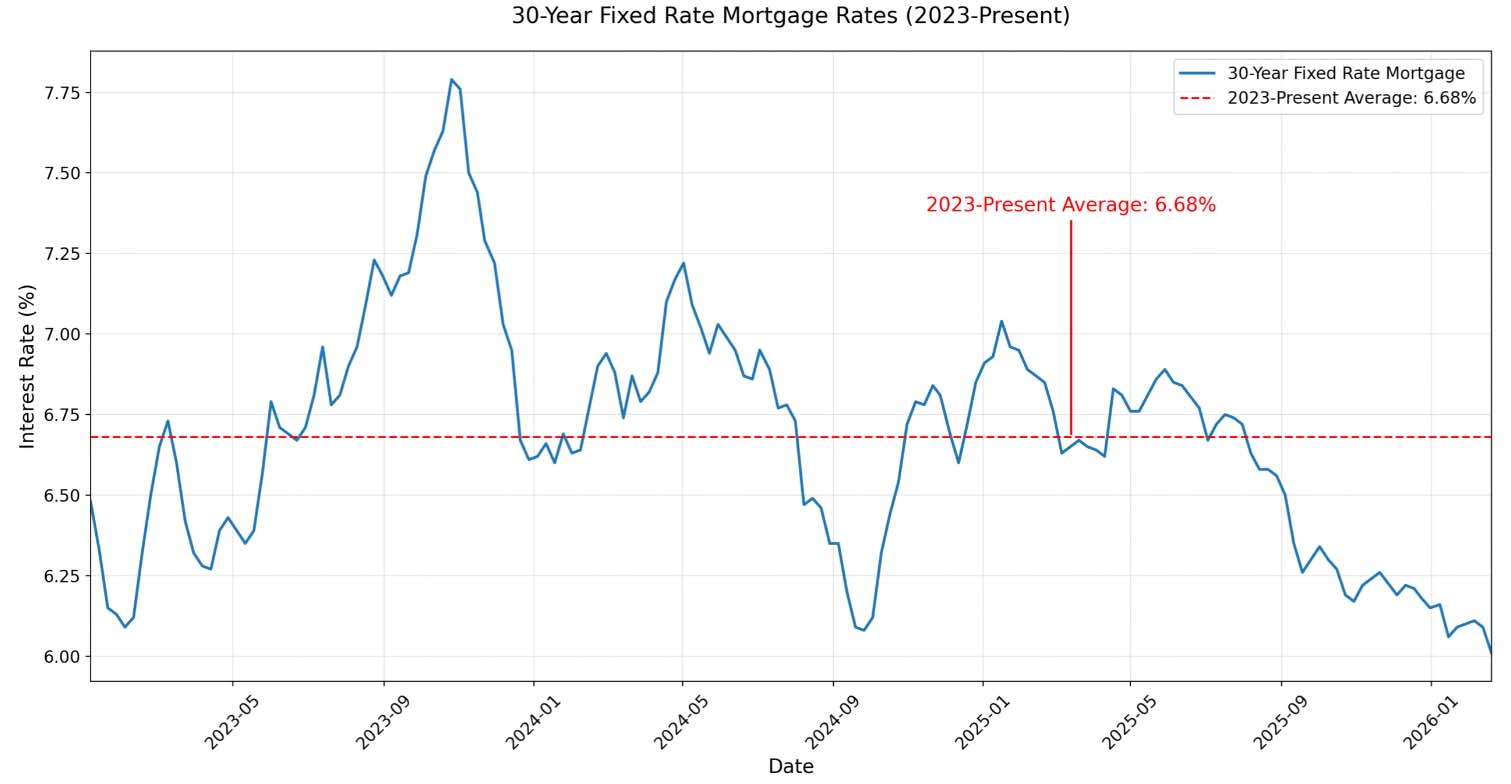

30-Year Fixed Mortgage Rates (2023-2026). Source: The Mortgage Reports

Strategy 1: Identifying "Stale" Listings for Maximum Leverage

The biggest mistake buyers make when entering a high-interest-rate market is continuing to shop the same way they did when rates were rock bottom. If you are only looking at properties that hit the MLS on Thursday and host an open house on Sunday, you are walking straight into a buzzsaw of competition. Fresh inventory in desirable St. Louis neighborhoods still commands top dollar.

To gain the leverage needed to negotiate your monthly payment down, you have to shift your focus to "stale" listings. In the context of the July 2026 market, a stale listing is any property that has been sitting active on the market for 30 days or more.

Why 30 days? Because the psychology of a seller changes dramatically at the one-month mark.

When a house first hits the market, sellers are optimistic. They have just spent weeks prepping, cleaning, and painting. By day 30, reality sets in. The showings start to dry up. The feedback from buyer agents is often lukewarm, usually pointing out that the home needs updates or is priced slightly too high for current borrowing costs. The seller begins to panic about carrying two mortgages, paying high taxes, or missing out on the home they want to buy themselves.

This is where your opportunity lies.

How to Find Stale Inventory in St. Louis

Your real estate agent should be running daily custom searches specifically filtered for Days on Market (DOM). You want to look for properties in your target school districts that have crossed that 30-day threshold.

Often, these homes are not fundamentally flawed. They might just suffer from terrible listing photos, a bad initial pricing strategy by an inexperienced agent, or minor cosmetic issues that scare off buyers who lack vision. A house in Ballwin that needs new carpet and a fresh coat of paint might sit for 45 days simply because buyers don't want to deal with renovations while paying a 6.5% interest rate.

If you are willing to look past minor imperfections, you suddenly hold all the negotiating cards. The seller wants out, and they know that in a high-rate environment, the pool of qualified buyers shrinks every day their house sits there.

Strategy 2: Mastering the 2-1 Rate Buydown Concession

Finding a motivated seller is only half the battle. The real magic happens at the negotiating table. When dealing with a stale listing, you shouldn't just ask for a blanket price reduction. Lowering the purchase price by $10,000 barely moves the needle on your monthly payment when rates are at 6.5%.

Instead, you need to negotiate for a seller concession specifically tailored to buy down your interest rate.

What is a 2-1 Buydown?

Here is how the mechanics work in practice:

-

Year 1: Your interest rate is reduced by a full 2%. If your approved fixed rate is 6.5%, your payments for the first 12 months are calculated at exactly 4.5%.

-

Year 2: Your interest rate is reduced by 1%. You will make payments calculated at 5.5% for months 13 through 24.

-

Years 3-30: Your rate returns to the original fixed note rate of 6.5% for the remainder of the loan.

The seller funds this by paying a lump sum at closing directly into an escrow account held by your lender. Every month for the first two years, a portion of that escrow money is used to subsidize your mortgage payment.

The Financial Impact for St. Louis Buyers

Let’s look at the hard numbers for a standard St. Louis suburban home priced at $400,000. Assuming you put 10% down, your loan amount is $360,000.

-

At a standard 6.5% rate, your principal and interest payment is roughly $2,275.

-

With a 2-1 buydown, your Year 1 payment (at 4.5%) drops to $1,824. That is a savings of $451 per month, keeping over $5,400 in your pocket during your first year of homeownership.

-

Your Year 2 payment (at 5.5%) is $2,044, saving you an additional $231 per month.

The total cost to the seller to fund this buydown is roughly $8,184.

Why would a seller agree to pay $8,000 of your costs? To a seller whose house has been sitting on the market for 45 days, handing over $8,000 in closing concessions is far more attractive than slashing their list price by $20,000 just to generate new interest. It preserves the optical value of their home while solving your immediate cash flow problem.

This strategy allows you to get into the house now, secure a highly affordable monthly payment for the next 24 months, and gives you a runway to potentially refinance if rates drop in 2027 or 2028.

Strategy 3: Bypassing the Bank with Owner Financing

While the 2-1 buydown is fantastic for traditional retail buyers, there is a completely different avenue that many St. Louis buyers overlook entirely: owner financing.

In a market where traditional bank lending is expensive and qualification standards are tightening, owner financing (also known as seller financing) cuts the bank out of the equation entirely. Instead of getting a mortgage from Wells Fargo or a local credit union, the seller of the property acts as the bank. You sign a promissory note agreeing to pay the seller directly over a set period, usually with a balloon payment due in 5 to 7 years.

Why Owner Financing Works in 2026

Owner financing is particularly prevalent in the St. Louis investment property market and for homes that might not qualify for traditional FHA or Conventional financing due to their condition. However, we are increasingly seeing it used for standard residential sales as a way to beat the high-rate environment.

Here is why a seller might offer it:

-

Monthly Income: Instead of taking a lump sum of cash that sits in a low-yield savings account, the seller receives a steady stream of monthly income backed by the collateral of the house.

-

Tax Benefits: Sellers can often spread out their capital gains tax liability over several years rather than taking a massive tax hit all at once.

-

Faster Closing: Without a bank underwriter picking apart your tax returns and demanding endless documentation, owner-financed deals can often close in a matter of days rather than weeks.

For buyers, the benefits are equally massive:

-

Negotiable Rates: You aren't bound by the Federal Reserve. You and the seller can agree on whatever interest rate makes sense for both of you. You might negotiate a 5% rate directly with the seller when the banks are charging 6.5%.

-

Flexible Terms: Everything is negotiable—the down payment, the amortization schedule, the interest rate, and the length of the contract.

-

Easier Qualification: If you are self-employed, a gig worker, or have a unique financial situation that makes traditional bank underwriting difficult, a private seller is often much more willing to look at your overall financial picture rather than just your W-2s and credit score.

If you are struggling to make the numbers work with traditional lenders, instruct your agent to actively seek out listings offering seller financing, or have them directly pitch the idea to sellers of properties that have been sitting vacant for months.

Why You Cannot Wait for a Market Crash

The most dangerous mindset a buyer can have in July 2026 is assuming that because interest rates are high, home prices are inevitably going to plummet. The narrative of a looming housing crash has been pushed for three years now, and it simply hasn't materialized in the St. Louis region.

The St. Louis market is fundamentally insulated from the wild boom-and-bust cycles seen in coastal markets like California or investor-heavy markets like Phoenix and Austin. We have a slow, steady, and incredibly resilient housing sector.

Because supply is so restricted, prices are holding firm. If you decide to wait another year for rates to drop, you run two massive risks:

-

Rates Don't Drop: The Federal Reserve's battle against inflation has been notoriously stubborn. If rates stay exactly where they are, or even climb to 7%, you will have wasted a year of equity building while paying rent.

-

Rates Drop, and Demand Explodes: If rates do suddenly drop to 5.5% this winter, every single buyer who has been sitting on the sidelines will flood the market simultaneously. You will instantly be thrown back into the chaos of bidding wars, waived inspections, and paying $30,000 over asking price.

Any savings you might get from a slightly lower interest rate will be completely wiped out by the inflated purchase price you'll have to pay to beat out the competition.

Securing Your Home Before the School Year

The clock is ticking. August is rapidly approaching, and if you want your family settled into a new home before the school year begins, you have to take decisive action now.

Stop looking at homes that hit the market yesterday. Stop letting the sticker shock of a 6.5% rate paralyze you. The tools to engineer a comfortable monthly payment exist, but they require a proactive, aggressive approach to the market.

Target the properties that have been sitting. Calculate exactly what a 2-1 buydown will save you, and instruct your agent to write it into the contract as a seller concession. Explore owner financing options if traditional lending isn't fitting your unique financial profile.

The St. Louis real estate market in July 2026 rewards the creative and the prepared. Use these strategies to beat the rate trap, lower your monthly payment, and get the keys to your new home before the summer ends.

Ready to Buy or Sell in St. Louis? House Sold Easy Has You Covered!

Whether you're thinking about listing your home or exploring a cash offer, it's worth understanding all of your options before making a decision. The right choice depends on your timeline, your property's condition, and your goals. Contact House Sold Easy to discuss your situation and see what makes the most sense for you.Our St. Louis experts know every corner of this city and will make buying your dream home or selling your high-end property a breeze. Don’t miss out on the hottest market in the U.S.! Contact House Sold Easy today and let’s make your real estate goals happen!