Why St. Louis Fixer-Uppers Cost More Than Turnkey Homes

May 28, 2026

Written by David Dodge

It is Thursday morning in St. Louis. For the third time this month, an eager but increasingly exhausted prospective homebuyer stands on the porch of a pristine, beautifully staged craftsman bungalow in South City, anxiously refreshing their phone. The listing price is an attractive $285,000. Their real estate agent steps outside, flips open a transaction dossier, and breaks the bad news: “We already have twelve offers on the table, three are entirely all-cash, and the highest escalation clause is currently sitting $45,000 over asking with an inspection waiver.”

This exact scene has become the defining narrative of the St. Louis metropolitan housing market in mid-2026. Across core sub-markets like South County (Mehlville, Oakville, Affton), North County (Florissant), and South City (Tower Grove, Princeton Heights, Dutchtown), the consumer demand for “move-in ready” or “turnkey” residential assets has hit an unprecedented, white-hot fever pitch. Buyers are locked in fierce, multi-offer bidding wars that routinely push final contract prices 15% to 20% above historical fair market value.

Fatigued by the relentless cycle of being outbid, many desperate buyers are pivoting toward an alternative that, on paper, feels like a financial liferaft: the classic, unrenovated St. Louis “fixer-upper”.

Digital search infrastructure reveals a massive, systematic spike in localized consumer queries. St. Louis residents are aggressively typing phrases like “How much does it cost to renovate a house in St. Louis” or “Are fixer-upper homes worth it with high interest rates” into search engines. The foundational math seems simple and intuitively sound: purchase a dated, older home in an established neighborhood for $200,000, inject $50,000 of localized structural and cosmetic updates, and emerge with a customized property valued at $275,000, thereby completely bypassing the turnkey premium.

However, in the macroeconomic landscape of 2026, this logic is not just flawed—it is a dangerous financial trap. The reality check hitting local buyers is swift and unforgiving. When you finance those structural or cosmetic renovations at a sticky 6.6% interest rate, factor in local building permit delays, and collect real-world quotes from specialized St. Louis contractors, you quickly discover that the traditional “sweat equity” discount has completely evaporated. Due to structural shifts in construction labor availability and domestic material supply chains, buying a home that needs work can easily end up costing you substantially more in liquid wealth, long-term interest payments, and psychological stress than paying the premium for a move-in-ready home.

The Turnkey Premium Explained: The Real Cost of Convenience

To understand why the fixer-upper math has completely flipped in 2026, we must first break down the forces driving what economists call the "Turnkey Premium." In the current economic environment, the modern homebuyer values immediate occupancy not as a subjective luxury, but as a critical financial hedge.

|

Metric Baseline |

Market Impact Realities |

|---|---|

|

6.6% Average 30-Year Mortgage Rate |

The average 30-year fixed mortgage rate remains elevated, significantly increasing long-term borrowing costs for both homebuyers and builders. |

|

+$7,200 Avg. First-Year Capital Outlay |

New homeowners typically spend an additional $7,000–$8,000 on repairs, upgrades, and maintenance within the first 12 months of ownership. |

|

40 Years Median First-Time Buyer Age |

The median age of first-time homebuyers continues to rise due to affordability challenges and limited entry-level inventory. |

Buyers are willing to bid up these properties because they can roll the entire cost of the home into a single, predictable, 30-year fixed mortgage. Even at 6.6%, a buyer knows exactly what their monthly principal and interest payment will look like for the next three decades. More importantly, they will not be forced to dip into their remaining liquid cash reserves to fix a leaking roof or replace a cracked heat exchanger during their first winter. This peace of mind has driven the premium for turnkey homes to historic highs, forcing budget-conscious buyers to look at properties they would have ignored three years ago.

The Macroeconomic Anatomy of the Fixer-Upper Trap

The core trap lies in the assumption that renovation costs are linear, predictable, and easily financed. The reality of executing a renovation project in 2026 involves battling three massive macroeconomic headwinds simultaneously: compounding inflation on building materials, a structural deficit in skilled construction labor, and the brutal reality of compounding interest on non-mortgage debt capital.

1. The Skyrocketing Cost of Construction Material and Domestic Logistics

While general consumer price index (CPI) numbers have shown stabilization, the producer price index (PPI) for construction materials tells a fundamentally different story. Reclaimed wood, specialized plumbing fixtures, domestic steel, and copper wiring have sustained high baseline costs. Importing materials or transporting them across state lines incurs persistent logistical costs.

A standard mid-sized kitchen remodel that cost $25,000 in 2019 now regularly prices out at $48,000 to $55,000 in the St. Louis metropolitan area. Simple structural upgrades, such as replacing rotted sill plates or updating cast-iron stack pipes common in South City brick homes, require premium materials that erode a $50,000 renovation budget before aesthetic work even begins.

2. The Skilled Labor Shortage and the St. Louis Contractor Premium

Finding a licensed, bonded, and reputable contractor in Eastern Missouri has become an exercise in extreme patience and high spending.

In St. Louis, this labor bottleneck is highly amplified. Because local general contractors are backed up with major commercial developments, infrastructure projects, and high-end luxury remodels in West County, they charge a premium to take on smaller residential projects in Florissant or South County. If a contractor accepts a $40,000 renovation job, they are factoring in substantial labor overhead to retain their crew against competing commercial firms. Homeowners are left choosing between unlicensed, unbonded handymen—risking structural code violations—or paying a premium for a certified crew, completely destroying the financial feasibility of the project.

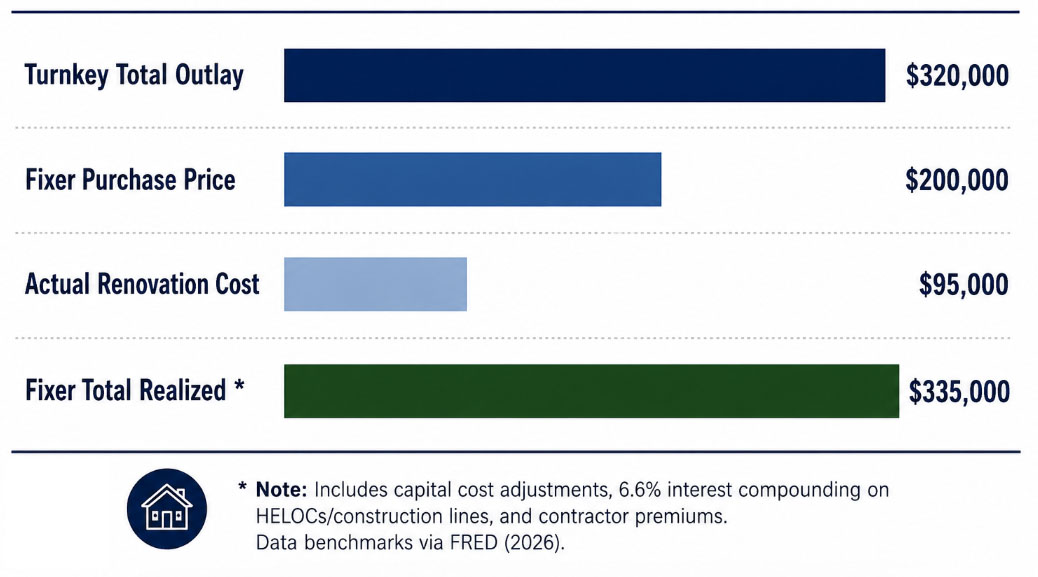

ST. LOUIS RESIDENTIAL BUDGET BREAKDOWN: TURNKEY VS. FIXER-UPPER (2026)

3. The Interest Rate Double-Whammy: Financing Renovations at 6.6% and Beyond

The single most destructive element of the fixer-upper trap is the cost of capital. Five years ago, a homebuyer could purchase a property using a conventional mortgage and fund renovations via a Home Equity Line of Credit (HELOC), a personal loan, or a specialized FHA 203(k) renovation loan at interest rates hovering around 3% to 4%. Today, with primary mortgage benchmarks holding firmly at 6.6%, construction financing structures have scaled proportionally upward.

If you take out a personal construction loan or an unsecured home improvement loan to cover a $50,000 renovation project, you are no longer paying mortgage rates. You are looking at specialized financing mechanisms that frequently carry interest rates between 8.5% and 12%, depending on credit tiering. If you roll the renovations into a single FHA 203(k) loan, your entire underlying mortgage principal absorbs a higher origination fee structure and strict, state-mandated oversight fees. Every dollar spent on drywall, wire, or cabinetry is heavily taxed by interest compounding at 6.6% or higher over 30 years, vastly inflating the lifetime cost of a simple aesthetic upgrade.

Neighborhood Spotlights: Where the Trap is Sprung in St. Louis

The financial physics of this phenomenon play out differently across the distinct architectural landscapes of the St. Louis metropolitan area. Let us examine three key regions where buyers frequently fall into the fixer-upper trap.

St. Louis Regional Structural Risk Matrix

|

Target St. Louis Region |

Typical Architecture Type |

Common "Hidden Pit" Component |

Estimated 2026 Repair Premium |

|---|---|---|---|

|

South City Tower Grove, Dutchtown, Princeton Heights |

1910s–1930s Historic Brick Masonry Bungalows |

Cast-Iron Stacks, Faulty Knobs, Rotted Sill Plates |

$25,000 – $45,000 |

|

Florissant / North County |

1950s–1960s Mid-Century Ranch Homes |

Slab Settlement, Outdated HVAC, Main Line Intrusion |

$18,000 – $35,000 |

|

South County Mehlville, Oakville, Affton |

1970s Split-Levels & Traditional Two-Stories |

Failed Retaining Walls, Aluminum Wiring, Aged Roofs |

$22,000 – $50,000 |

South City: The Charm of Historic Brick vs. Century-Old Deferred Maintenance

South City neighborhoods like Tower Grove, Princeton Heights, and Dutchtown are famous for their beautiful historic brick architecture. To a buyer priced out of a $350,000 renovated South City home, a $190,000 unrenovated brick four-square feels like a golden opportunity. However, these century-old homes feature complex, non-standard structural engineering.

Opening up a lath-and-plaster wall to update archaic knob-and-tube electrical wiring almost always uncovers further code violations. Plumbers frequently discover that the original underground cast-iron sewer stack is completely collapsed or heavily intruded by tree roots, demanding an immediate $15,000 main-line excavation. Because these historic homes fall under strict local historic preservation codes, replacement windows and exterior masonry work must meet rigorous architectural standards, multiplying material and specialized labor costs by two or three times standard suburban rates.

Florissant: Mid-Century Ranch Houses and the Danger of Slab and Main-Line Failures

Moving north to Florissant, buyers encounter rows of mid-century ranch homes built in the 1950s and 1960s. These homes are highly sought after by young families and first-time buyers due to their single-level layouts and reasonable baseline pricing. A dated, unrenovated Florissant ranch can often be secured for $165,000, while its fully modernized counterpart commands a $240,000 price tag. This $75,000 gap appears to offer a massive buffer for renovations.

However, many of these mid-century homes were constructed on concrete slabs or feature low-clearance crawlspaces. If the property has experienced uneven foundation settling over the decades, leveling the slab requires deep structural mud-jacking or piering, which instantly drains $15,000 to $25,000 without moving a single interior wall. Furthermore, updating original localized HVAC configurations or correcting poor drainage grading around the expansive perimeter can quickly exhaust a renovation budget, leaving the buyer with an open construction zone and zero liquid cash to complete the kitchen or bathroom updates they originally planned.

South County: Split-Levels and the Hidden Infrastructure Deficit

In South County communities like Affton, Mehlville, and Oakville, the dominant architectural styles are 1970s split-levels and traditional two-story frame houses. A fixer-upper here typically takes the form of a house with original wood paneling, worn shag carpeting, an outdated kitchen, and a dated deck. While these homes rarely suffer from the historic plaster failures of South City, they present an infrastructure deficit.

Roofs, asphalt driveways, and concrete retaining walls built in the late 20th century are reaching the absolute end of their operational lifespans. Replacing a failing 150-linear-foot timber retaining wall on a sloped South County lot routinely prices out at $20,000 in 2026 labor rates. Replacing an original multi-zone HVAC system alongside a weathered, leaking roof can cost another $25,000. Buyers focus heavily on the visual appeal of a modern open-concept floor plan, but find themselves forced to spend their entire budget fixing underground drainage tile, replacing rotted subfloors, and updating dated structural elements.

The Post-Purchase Spending Spike: Empirical Evidence

This dynamic is supported by academic research into consumer behavior patterns surrounding residential real estate transactions.

Crucially, this spending surge is heavily concentrated among first-time homebuyers and individuals purchasing properties that require immediate maintenance or modernization.

Renovation Reality Check: The True Financial Math

Let us analyze a real-world scenario comparing a turnkey purchase against a fixer-upper in South County under current 2026 market dynamics:

-

Scenario A (The Turnkey Route): You purchase a fully modernized home in Affton for $315,000 at a 6.6% interest rate. Your down payment is 10% ($31,500), resulting in a loan balance of $283,500. Your principal and interest payment is fixed at approximately $1,810 per month. The home requires zero immediate capital outlays, leaving your remaining liquid savings intact to earn yield in a high-interest savings account.

-

Scenario B (The Fixer-Upper Trap): You buy a dated home down the street for $210,000. Your 10% down payment is $21,000, creating a loan balance of $189,000 and a monthly mortgage payment of $1,208. You have "saved" $602 per month on your mortgage. However, the home requires a kitchen remodel, a panel upgrade, and a new roof to be functional. Contractor bids come in at $65,000.

To fund this, you use $25,000 of your remaining cash and take out a $40,000 home improvement loan at 9.5% interest over a 10-year term. The monthly payment on that construction loan is $517 per month. Your combined monthly housing payment is now $1,725. You are saving a mere $85 per month compared to the turnkey option, but you have fully depleted your liquid emergency fund by $25,000, spent six months living in an active construction zone, and are personally managing a complex network of unpredictable subcontractors.

The Renovation Reality Check: A Tactical Guide for St. Louis Buyers

If you choose to navigate the St. Louis fixer-upper market, you must abandon romanticized television narratives and operate with strict financial discipline. Use this tactical blueprint to evaluate properties, spot hidden money pits, and negotiate a protective contract structure.

1. How to Spot "Good Bones" vs. Structural Money Pits

When walking through an unrenovated property in South County, Florissant, or South City, you must train your eyes to ignore cosmetic issues like peeling wallpaper, dated carpets, and avocado-green appliances. Instead, focus entirely on the structural, mechanical, and environmental health of the property:

-

The Foundation Alignment Test: Bring a high-grade torpedo level or a simple steel marble to every open house. Place it on the basement concrete or along the main floor joists. In older South City brick homes, minor settling is normal, but horizontal cracking along concrete blocks or significant bowing in limestone foundation walls indicates active hydrostatic pressure failures. Repairing a failing foundation can instantly cost $20,000 to $30,000.

-

The Electrical Panel Audit: Locate the main electrical service panel. If you see an outdated brand name like Federal Pacific, Zinsco, or an old-style fuse box, the home is a fire hazard. Upgrading a service panel from an old 60-amp or 100-amp system to a modern 200-amp configuration required for modern appliances costs between $3,500 and $6,000 in St. Louis contractor labor. If the home features original ungrounded cloth-covered wiring throughout, a complete whole-house rewire can exceed $18,000.

-

The Scope-the-Sewer Mandate: Never buy an older property in St. Louis without paying a licensed technician $200 to run a camera down the main sewer line to the municipal connection. Clay pipes in older Florissant neighborhoods and cast-iron stacks in South City are highly prone to structural collapse, scale buildup, and tree root intrusions. If the line is cracked beneath the concrete basement floor or under the street, you are looking at a mandatory excavation bill ranging from $8,000 to $22,000 before you can safely flush a toilet.

2. The "30-Day Stale Home" Negotiation Blueprint

The hyper-competitive bidding wars of 2026 are intensely concentrated in the first 7 to 10 days on the market. If a property is dated and has been listed for more than 30 days, the psychological dynamic shifts completely. The seller's initial listing confidence turns to anxiety, giving savvy buyers an opening to secure a true financial discount. Use this clear negotiation strategy:

-

Quantify the Discount via Contractor Estimates: Do not simply make a lowball offer based on general feelings. Bring a licensed general contractor or structural engineer through the home during a secondary viewing. Request a formalized, line-item bid detailing exactly what it will cost to bring the property up to safety and building codes. Present this real-world estimate directly to the listing agent alongside your offer as empirical justification for your price reduction.

-

Structure an Escrow Holdback for Hidden Repairs: If an older home has a functional but aged mechanical asset—such as a 22-year-old furnace or a roof at the end of its lifespan—do not accept the seller's claim that "it still runs fine." Negotiate an escrow holdback clause. This mechanism ensures a specific portion of the seller's proceeds (e.g., $10,000) is held by the title company for 60 days post-closing. If the system fails immediately upon occupancy, those funds are automatically deployed to cover the repair costs.

-

Target the Over-Leveraged Seller: Research public property registries via the local county recorder of deeds to determine when the current owner purchased the home and what their outstanding debt level looks like. Sellers who inherited a property through probate or have owned a home for over 25 years possess immense equity liquidity. They are far more likely to accept a major price reduction than a recent investor who purchased the property at a premium and cannot afford to lower the price without bringing cash to the closing table.

Conclusion: Shifting Your Strategy in the 2026 Housing Market

The traditional real estate mantra was simple: “Buy the worst house on the best block, put in some sweat equity, and build long-term wealth.” While that strategy served multiple generations of St. Louisans well, the macroeconomic environment of 2026 has temporarily broken that model. The compounding strains of a historic construction labor shortage, high material costs, and sticky 6.6% financing rates have transformed the classic fixer-upper from a wealth-building tool into a major cash drain.

For buyers trying to establish roots in South County, Florissant, or South City, the path forward requires a fundamental shift in perspective. Do not look at a move-in-ready home's premium price tag simply as an extra expense. Instead, understand it for what it truly is: a financial shield that locks in your housing costs, preserves your remaining liquid capital, and protects you from the unpredictable, high-inflation world of modern home construction. In today's market, true financial freedom isn't found in a long, expensive remodeling project—it is found in a turnkey home where you can unlock the front door, unpack your bags, and live comfortably from day one.

Ready to Buy or Sell in St. Louis? House Sold Easy Has You Covered!

Navigating St. Louis’ red-hot luxury market doesn’t have to be a headache. With House Sold Easy, it’s all about less hassle—we’ve got you covered from start to finish. Our St. Louis experts know every corner of this city and will make buying your dream home or selling your high-end property a breeze. Don’t miss out on the hottest market in the U.S.! Contact House Sold Easy today and let’s make your real estate goals happen!