First-Time Homebuyer in St. Louis? Here's How to Buy in 2026

Mar 02, 2026

Written by David Dodge

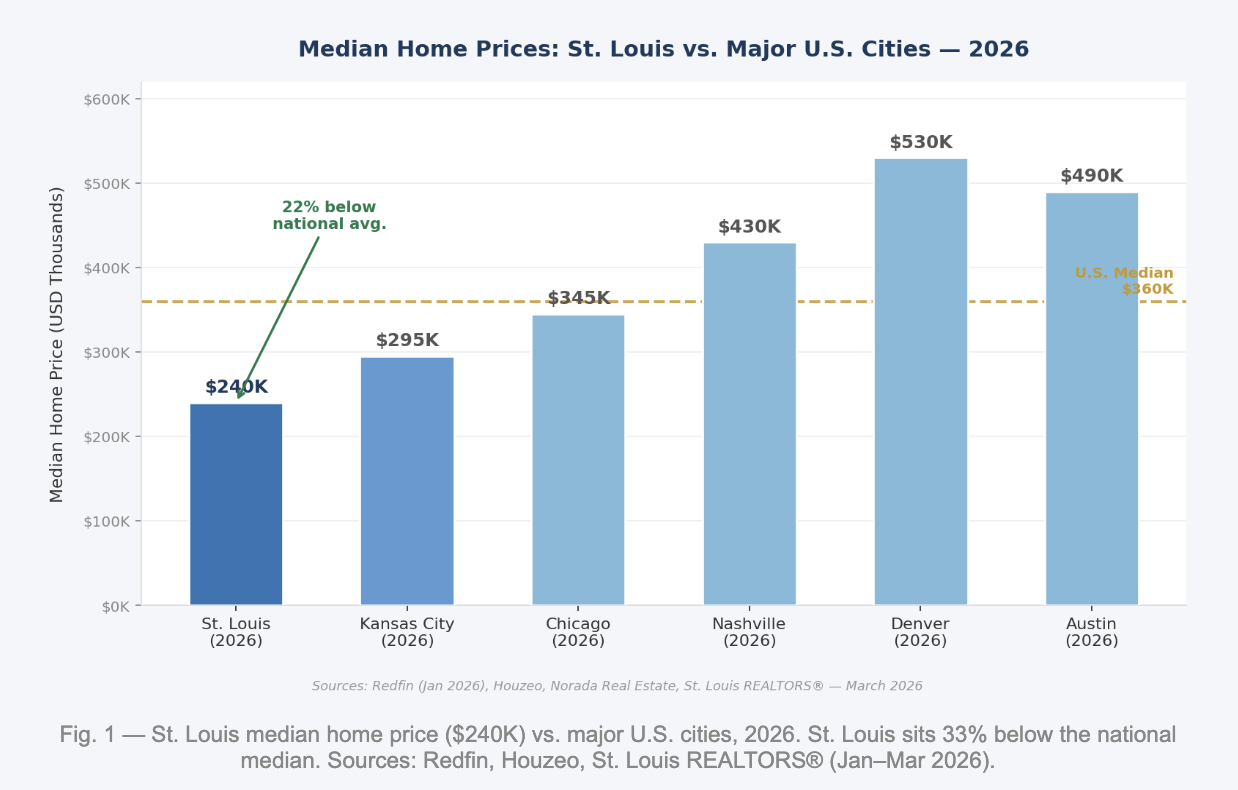

If you're a first-time homebuyer in St. Louis in 2026, you've picked your moment well. While real estate headlines across the country are dominated by stories of strained affordability, cooling demand, and buyer paralysis, St. Louis continues to defy the national trend. According to data published by St. Louis REALTORS in early 2026, the metro median home price stands at $240,000 — a figure that sits roughly 33% below the national median of $360,000. In a year when buyers in Nashville are staring down $430,000 price tags and Denver buyers are navigating a $530,000 average, that gap is staggering.

But 2026 is also a year of a meaningful shift in the St. Louis market. Inventory has crept back up to approximately 2.6 months of supply, mortgage rates have eased slightly to around 5.94% on a 30-year fixed as of early February, and the frenzied waive-everything, offer-in-an-hour energy of 2023 and 2024 has settled into something more measured. As one St. Louis Magazine report from January 2026 noted, this year represents the best window for buyer negotiation since 2019 — provided you know what you're doing and where to look.

That's exactly what this guide is for. Whether you're just starting to think about buying or you've been saving for two years and are ready to move, this is your complete, locally informed, 2026-specific roadmap to buying your first home in St. Louis.

|

St. Louis Market Snapshot — March 2026 |

Data |

|---|---|

|

Median Home Price (City) |

$240,000 (Redfin, Jan 2026) |

|

Median Home Price (Metro) |

$275,000 (St. Louis REALTORS®) |

|

Year-Over-Year Price Growth |

+4.1% (Redfin) / +9.1% peak neighborhoods |

|

Average Days on Market |

49 days overall; 11–15 days in hot pockets |

|

Months of Supply |

~2.6 months (seller-tilted but easing) |

|

30-Year Fixed Mortgage Rate |

~5.94% (Feb 2026, down from 2024 highs) |

|

Forecast Appreciation (2026) |

+3–4% projected through year-end |

|

Sale-to-List Ratio |

98% metro average; 103% in areas like Crestwood/Kirkwood |

Why St. Louis Is One of the Best Cities for First-Time Homebuyers in 2026

Let's start with the number that matters most: in January 2026, the median home sale price in St. Louis was $240,000 according to Redfin — and the broader metro median sits at $275,000 per St. Louis REALTORS data. Those numbers tell a story that no amount of national real estate commentary can capture.

While coastal markets and formerly "hot" Sun Belt cities like Austin and Nashville have either plateaued or softened significantly, St. Louis has continued its quiet, steady climb. Prices are up 4.1% year-over-year as of January 2026, and experts are forecasting a further 3–4% appreciation through the rest of the year. This is not speculative bubble territory — it's the kind of reliable, fundamentals-driven growth that makes homeownership a sound long-term investment.

The affordability story gets even more compelling when you zoom out. St. Louis offers a 22% lower cost of entry than the national average, according to 2026 market analysis. That means a first-time buyer with a modest down payment can get into a real home in a real neighborhood — not a distant exurb with a two-hour commute, but a place like Maplewood, Tower Grove South, or Kirkwood where people actually want to live.

The 2026 market has also given buyers something rare: breathing room. With inventory rising 9% year-over-year and days on market extending to an average of 49 days for standard listings, buyers in most price ranges no longer face the all-or-nothing pressure of 2022 and 2023. You can schedule a second showing. You can ask for an inspection. You can negotiate on repairs. That's a significant quality-of-life improvement for first-time buyers who are already navigating an unfamiliar process.

St. Louis Magazine's January 2026 housing report put it bluntly: in markets like Nashville and Austin, sellers now outnumber prospective buyers by 111% and 128% respectively. That dynamic simply doesn't exist here. St. Louis real estate agents report coming off a strong 2025 and expect 2026 to continue that momentum — particularly in the mid-county areas and desirable school districts that have remained consistently competitive.

Beyond price, there's the broader quality of life equation. St. Louis offers free world-class amenities — Forest Park (larger than New York's Central Park), the St. Louis Zoo, the Arch grounds — alongside a diverse and evolving restaurant scene, professional sports, and a genuine sense of neighborhood identity that's increasingly rare in American cities. For first-time buyers wondering whether they're trading lifestyle for affordability, St. Louis offers both.

The Step-by-Step Process for First-Time Homebuyers in St. Louis

Buying your first home is a process, not an event. The buyers who feel most confident and make the best decisions are the ones who understand the sequence — and complete each step before jumping to the next. Here's how it works in St. Louis in 2026.

Step 1: Know Your Credit Score and Set a Realistic Budget

Before you look at a single listing, you need an honest picture of your financial position. Start with your credit report — pull all three bureaus for free at annualcreditreport.com and review them for errors, collections, or derogatory marks. Errors are more common than people think and can be disputed and removed.

In 2026, with rates around 5.94% on a 30-year fixed, the difference between a 680 and a 740 credit score can translate to a meaningful difference in your monthly payment and total interest paid over 30 years. FHA loans accept scores as low as 580 for the minimum 3.5% down payment; conventional loans typically require 620 or higher.

Then get honest about your budget. Calculate your gross monthly income, add up your monthly debts, and determine your debt-to-income ratio (DTI). Most lenders want that number at or below 43%. Factor in the full cost of homeownership beyond just the mortgage: St. Louis property taxes (which vary significantly by municipality), homeowner's insurance, any HOA fees, and a maintenance reserve. A practical rule of thumb is to budget 1–2% of the home's value annually for upkeep.

Step 2: Explore Missouri and St. Louis-Specific Assistance Programs

This is the most underutilized step in the entire St. Louis homebuying process. Missouri has a set of programs through the Missouri Housing Development Commission (MHDC) that provide real, tangible financial help to first-time buyers — and thousands of eligible buyers simply never apply because they don't know these programs exist.

The MHDC First Place Loan program offers a 30-year fixed-rate mortgage paired with cash assistance of up to 4% of the loan amount, which can be applied directly to your down payment or closing costs. On a $240,000 home, that's up to $9,600 in direct financial assistance. There are income limits and property eligibility requirements, but many first-time buyers in the St. Louis metro qualify.

At the federal level, FHA loans remain the most accessible entry point with 3.5% down at 580+ credit. USDA loans offer 100% financing — no down payment — for homes in eligible areas outside the city proper, some of which are well within commuting range of downtown St. Louis. Veterans and active-duty service members should explore VA loans, which also offer zero down payment with no private mortgage insurance requirement.

With 30-year rates having eased to the mid-5% range in early 2026 after the painful highs of recent years, the monthly payment math has improved meaningfully. This is a window that buyers who've been sitting on the sidelines should seriously consider.

|

2026 Down Payment Assistance — Missouri First-Time Buyers |

Details |

|---|---|

|

MHDC First Place Loan |

Up to 4% cash assistance on down payment or closing costs |

|

FHA Loan |

3.5% down minimum (580+ credit score) |

|

USDA Loan |

0% down in eligible suburban/rural areas near St. Louis |

|

VA Loan |

0% down for eligible veterans and active-duty members |

|

Conventional 97 |

3% down for qualifying first-time buyers |

|

Key: Always ask your lender if they are MHDC-approved before committing to any program. |

|

Step 3: Get Pre-Approved with a Local St. Louis Lender

In today's St. Louis market, pre-approval isn't a formality — it's your entry ticket. Without a current pre-approval letter, most listing agents will not present your offer. More importantly, pre-approval tells you the exact price range you can genuinely afford, so you're not wasting weekends touring homes you can't buy.

We recommend working with a local St. Louis lender over national online platforms like Rocket Mortgage or Better. Here's why: local lenders understand Missouri-specific programs like MHDC, have established relationships with local title companies and real estate attorneys (Missouri is an attorney-closing state), and can often provide faster communication and decision-making when you're in a competitive offer situation. In a market where hot homes in Kirkwood still go pending in under 15 days, that responsiveness matters.

To apply, you'll need your last two years of tax returns and W-2s, two to three months of bank statements, recent pay stubs, and a government-issued ID. The process takes 2–5 business days. Pre-approval letters are valid for 60–90 days, so time your application to roughly align with when you expect to start seriously touring homes.

Step 4: Start Your Home Search by St. Louis Neighborhood

St. Louis is fundamentally a city of neighborhoods — and choosing the right one for your life and budget is as important as any financial calculation. Here's a current snapshot of the most popular areas for first-time buyers in 2026:

- Webster Groves — Consistently one of the most in-demand inner-ring suburbs. Charming historic homes, excellent schools, and a walkable village feel. The competitive pressure here remains high — expect multiple offers on well-priced homes. Budget: $260,000–$400,000 for entry-level single-family.

- Maplewood — A favorite among young professionals for its density of independent restaurants, coffee shops, and walkable streets. Prices have climbed but remain more accessible than Webster. Homes move fast in the 11–20 day range.

- Tower Grove South / South City — Historic bungalows, a diverse and active community, and proximity to South Grand Avenue's dining corridor. Strong long-term appreciation with more accessible entry prices. Good value for buyers who want urban character.

- Kirkwood — A complete suburb with its own thriving downtown, Amtrak access, excellent schools, and strong community identity. One of the markets where the 2025 report noted homes selling 20% over asking with waived inspections in peak season. Approach competitively.

- Brentwood / Richmond Heights — Centrally located with quick highway access to everywhere in the metro. A blend of ranch-style homes and newer construction. Strong appreciation trajectory and a balanced market feel in 2026.

- Florissant / Hazelwood — North county communities offering larger lots and square footage at more accessible price points. Best value-per-square-foot in the metro. Ideal for buyers prioritizing space and budget over walkability scores.

One important 2026 note: the St. Louis market is increasingly bifurcated. Per recent data, the sale-to-list ratio in hot pockets like Crestwood and Kirkwood is still running at 103% — meaning homes are selling above asking price. In less competitive areas, the metro average has dipped to 98%, meaning modest negotiating room exists. Your agent should help you understand which dynamic applies to your specific target neighborhoods.

Step 5: Making a Competitive Offer in 2026

The good news for 2026 buyers: you no longer need to waive every contingency and offer $50,000 over asking just to compete. The inventory increase and slight cooling of the broader market has restored some sanity to the offer process. That said, the most desirable homes in the best neighborhoods are still competitive — and a poorly structured offer will lose every time.

Start with a careful offer price rooted in recent comparable sales in the same neighborhood. Your buyer's agent will prepare a Comparative Market Analysis (CMA) that tells you what similar homes have actually sold for — not what they were listed at. In a market where the metro sale-to-list ratio is 98%, there's often modest negotiating room on price, but don't be cavalier about it.

If you're buying in a competitive pocket like Kirkwood or Webster Groves, consider an escalation clause — a provision that automatically increases your offer by a set increment above any competing bid, up to a maximum you're comfortable with. Pair this with a strong earnest money deposit (1–2% of purchase price in St. Louis is standard; higher signals commitment).

On contingencies: with inventory recovering, you no longer need to routinely waive the inspection contingency to win. Given that much of St. Louis's housing stock was built in the 1920s–1960s, a thorough home inspection is not optional — it's essential. Hidden foundation issues, aging electrical panels, and old sewer lines are real risks in older homes. The $400–$600 inspection cost can uncover tens of thousands of dollars in necessary repairs.

Once your offer is accepted, you enter the closing pipeline: home inspection (typically within 7–10 days of acceptance), appraisal, final loan approval, and closing. In St. Louis, the full process from accepted offer to keys typically runs 30–45 days.

Common Mistakes First-Time Buyers Make in St. Louis — and How to Avoid Them

Experience is expensive in real estate. Here are the mistakes we see most often — and what to do instead.

- Skipping pre-approval before starting the search. Without pre-approval, you can't make a legitimate offer. And in neighborhoods where good homes go in 11–15 days, the 3–5 days it takes to get pre-approved after you find a home is often 3–5 days too long.

- Forgetting about the total cost of ownership. The mortgage payment is only part of the picture. Property taxes in St. Louis vary significantly by municipality — St. Louis City, St. Louis County, and individual municipalities all have different rates. Add insurance, HOA fees if applicable, and a 1–2% annual maintenance reserve. Many first-time buyers are genuinely surprised by these costs in year one.

- Missing Missouri's MHDC assistance programs. This may be the single most expensive mistake first-time buyers make. Up to 4% of the loan amount in cash assistance is real money — potentially $8,000–$10,000 on a median St. Louis purchase. Always ask your lender about it before assuming you're on your own.

- Falling in love with a house before a neighborhood. The neighborhood — its trajectory, schools, walkability, commute — matters as much as the home itself. Do your research on crime trends, school ratings, planned developments, and flood zone status before committing.

- Waiving the home inspection. The 2026 market has given buyers the ability to include inspection contingencies in most offers. Use it. St. Louis's older housing stock makes this especially important. A $400 inspection is the best $400 you will spend.

- Underestimating closing costs. In Missouri, closing costs typically run 2–5% of the purchase price. On a $240,000 home, that's $4,800–$12,000 on top of your down payment. Ask your agent early about negotiating seller concessions — especially on homes that have been sitting on the market longer than average.

- Working with an out-of-area agent. St. Louis is a hyper-local market. Flood zones, school district lines, neighborhood trajectories, and off-market opportunities are things only a local expert can navigate confidently.

- Making major financial changes between the offer and the closing. Don't buy a car, open new credit accounts, change jobs, or make large unexplained bank transfers between offer acceptance and closing day. Any of these can disrupt your loan approval at the worst possible moment.

Frequently Asked Questions: Buying Your First Home in St. Louis in 2026

Here are the questions first-time buyers ask us most — answered honestly for current market conditions.

- How much do I need to put down as a first-time homebuyer in St. Louis in 2026?

Less than you might think. VA and USDA loans offer 0% down for eligible buyers. FHA loans require just 3.5% down with a 580+ credit score. Conventional loans can go as low as 3% for qualifying first-time buyers. Missouri's MHDC First Place Loan program can provide up to 4% of the loan amount in cash assistance toward your down payment or closing costs. On a $240,000 home, that means many buyers are closing with less than $10,000 out of pocket when programs are stacked correctly.

- Is 2026 a good time to buy a first home in St. Louis?

Yes — and arguably one of the better windows in recent years. Mortgage rates have eased to around 5.94% on a 30-year fixed as of February 2026, down from recent peaks. Inventory is up 9% year-over-year, giving buyers more options and more negotiating leverage than 2022–2024. Home prices are appreciating steadily at 3–4% projected for 2026 — not bubble territory, but meaningful equity growth. Market analysts have called 2026 the best buyer negotiation window since 2019.

- What credit score do I need to buy a home in St. Louis?

FHA loans accept scores as low as 580. Conventional loans typically require 620 or higher. However, a score of 700+ will get you meaningfully better interest rates. With 30-year rates around 5.94%, the difference between a 660 and 740 score can save hundreds of dollars per month over the life of a mortgage. If your score needs improvement, spending 3–6 months reducing credit card balances and clearing any collections can pay significant dividends before you apply.

- What are the most affordable neighborhoods in St. Louis for first-time buyers in 2026?

For buyers prioritizing value, Tower Grove South and South City neighborhoods offer the best combination of price, character, and long-term appreciation potential. North County communities like Florissant and Hazelwood offer the most square footage per dollar in the metro. Brentwood and Richmond Heights offer central locations with solid school options at mid-range prices. For those willing to look at the broader St. Louis metro, communities in St. Charles County continue to offer strong value for families prioritizing newer construction and top-rated schools.

- How competitive is the St. Louis housing market right now?

It depends heavily on the neighborhood and price range. Metro-wide, the market has moderated — average days on market have extended to 49 days, and the sale-to-list ratio has dipped to 98% in many areas. However, high-demand pockets like Kirkwood, Webster Groves, and Crestwood remain intensely competitive, with sale-to-list ratios still running at 103% and hot homes going under contract in 11–15 days. Know your target neighborhoods before assuming you can take your time.

- Do I need a buyer's agent, and will it cost me anything?

You absolutely need a buyer's agent — and in most St. Louis transactions, buyer representation is free to you. The seller typically covers both the listing agent's and buyer's agent's commission. Your agent will run comparable sales analysis, advise on offer strategy, coordinate inspections and title work, and advocate for you through every stage of the transaction. For a first-time buyer in an unfamiliar market, having an experienced local agent is one of the most valuable, risk-reducing decisions you can make.

- What closing costs should I expect in St. Louis?

Budget 2–5% of the purchase price. On a $240,000 home, that's $4,800–$12,000. Common items include lender origination fees, title insurance, attorney fees (Missouri is an attorney-closing state), property tax prorations, prepaid homeowner's insurance, and prepaid mortgage interest. The specific amount depends on your loan type, lender, and what you negotiate with the seller. First-time buyers are often caught off guard by closing costs — build this into your total savings target from day one.

Ready to Buy Your First Home in St. Louis? Let's Talk — Free Consultation.

The 2026 St. Louis market offers a genuine opportunity for first-time buyers: improving inventory, easing mortgage rates, and prices that remain well below national averages. But every buyer's situation is different — your credit, budget, timeline, and neighborhood priorities are unique. Our team specializes in guiding first-time buyers through the St. Louis market from pre-approval to closing. We know the neighborhoods, the programs, and the strategies that get buyers into homes they love at prices that make sense. Schedule a free, no-obligation consultation today. We'll review your situation, walk you through your down payment options (including MHDC programs you may not know about), and build a personalized roadmap for your homebuying journey.

📞 Call or text us anytime to get started 636-525-1566

Ready to Buy or Sell in St. Louis? House Sold Easy Has You Covered!

Navigating St. Louis’ red-hot luxury market doesn’t have to be a headache. With House Sold Easy, it’s all about less hassle—we’ve got you covered from start to finish. Our St. Louis experts know every corner of this city and will make buying your dream home or selling your high-end property a breeze. Don’t miss out on the hottest market in the U.S.! Contact House Sold Easy today and let’s make your real estate goals happen!