Sell Your Tornado-Damaged St. Louis Home Fast for Cash

Jun 02, 2026

Written by David Dodge

Key Takeaway: A year after the tornado, the city is finally moving money — but for thousands of North St. Louis families dealing with damaged or inherited property, government assistance may never reach them. Understanding your real options now could save you months of waiting and uncertainty.

If you've been watching the headlines lately, you already know the City of St. Louis has been in a heated back-and-forth over how to spend nearly a quarter-billion dollars from the Rams NFL settlement. A significant portion of that money — $110 million — has been earmarked specifically for North St. Louis tornado recovery. On paper, that sounds like a lifeline. And for some people, it will be.

But here's the part that doesn't make the front page: a huge number of homeowners, heirs, and landlords in North City are going to fall through every single gap that bill creates. If your property was vacant before the tornado, if you missed the insurance deadline, if the title has been tangled up in family ownership for decades, or if you simply inherited a house you never planned to own, the city's programs may leave you with nothing but a demolition notice and a tax bill.

This blog is written for you.

What the $110M Actually Means — And Who It Doesn't Help

On May 14, 2026, Mayor Cara Spencer and Board of Aldermen President Megan Green formally introduced legislation to allocate $230 million of the city's Rams settlement across three priority areas. The breakdown looks like this:

Tornado Recovery

Infrastructure

Revitalization

Of that $110 million, $70 million goes toward home repair and housing preservation, $31 million toward neighborhood implementation, and $5 million toward rental assistance and nonprofit case management. The remaining $4 million covers program management and compliance costs.

It sounds comprehensive. But community groups have been loud about the math. Action St. Louis, which mobilized over 150 people to rally outside City Hall the day after the bill was introduced, argues that tornado damage caused over $1.6 billion in damages to city wards — meaning $110 million barely scratches the surface. Their demand has been $150 million minimum, calling the current proposal a stopgap rather than a solution.

“The northside cannot remain in the state it's in. We've got a tornado-sized hole in this city.”

— Community member, Board of Aldermen public comment, May 2026

The bigger issue for individual property owners isn't the total dollar amount — it's eligibility. The programs that actually distribute these funds come with strict conditions, and the people who need help most are often the ones who don't qualify.

The FEMA & SEMA Demolition Reality Check

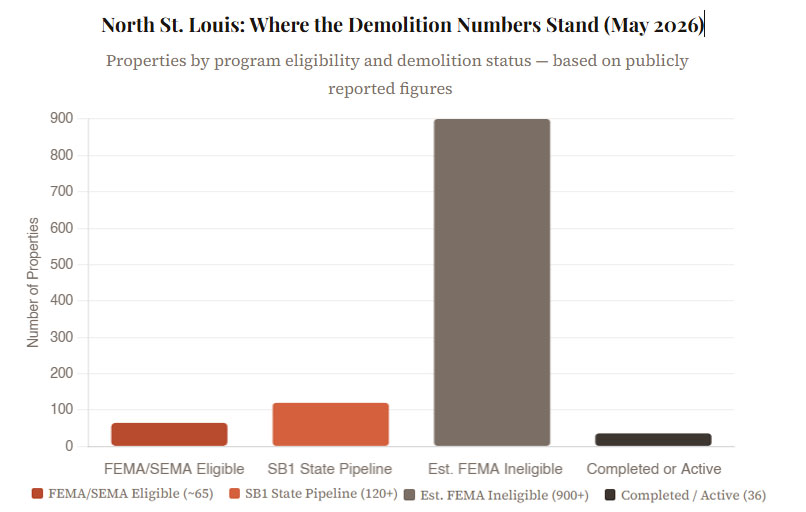

Also announced on May 14th, the City of St. Louis and the State of Missouri officially launched the FEMA/SEMA-funded demolition program, starting with 19 properties in the Academy/Sherman Park and Fountain Park neighborhoods. The Private Property Debris Removal program is expected to ultimately clear an estimated 65 structurally compromised structures — a number that sounds meaningful until you consider the scale of what remains.

A separate state-funded SB1 demolition pipeline has also ramped up. As of May 11, 2026, over 120 properties had been approved and moved into the demolition pipeline, with 36 demolitions already completed or actively underway. The SB1 program provides $10 million to handle properties that FEMA won't touch.

Here's the catch that's been buried in city press releases since February: FEMA has ruled that nearly 80% of private demolitions in North St. Louis don't qualify for federal reimbursement. Why? Because most of the properties were already vacant and condemned before the May 2025 tornado hit. Under FEMA's existing guidance — unchanged since the Biden administration — structures that were condemned before the disaster declaration are universally ineligible for demolition coverage.

Chief Recovery Officer Julian Nicks acknowledged the bind publicly: "Every dollar that we don't get covered by FEMA is a dollar that has to come from somewhere else that can't be used for all those other purposes that we know are much needed in our recovery."

That somewhere else is now largely SB1 state funding and whatever the city can carve out of the Rams settlement. But here's what that means practically for a family sitting on inherited property: if the structure is condemned, if the family owns multiple properties, or if it was commercially classified, you're almost certainly not in the FEMA queue. And the state and city programs have finite money and limited bandwidth.

The Inherited Property Problem Nobody Talks About

Walk through any block in Fountain Park, Academy, or Wells-Goodfellow, and you'll notice the same pattern: houses that have been in families for two or three generations. Maybe grandma paid it off in the 1980s. Maybe the deed was never updated after Dad passed. Maybe there are four siblings in four different states who technically co-own a place none of them have stepped inside in years.

These are "heirs' property" situations, and they've been a known problem in North St. Louis long before any tornado. After the May 2025 storm, the issue exploded. FEMA's own rules complicate it further: the federal agency classifies multiple properties owned by the same entity — including families managing two or three inherited homes — as commercial, making them ineligible for individual homeowner assistance regardless of who actually lives in them.

What this creates in practice is a class of property owners who are simultaneously:

- Not eligible for city-funded demolition (FEMA/SEMA won't cover them)

- Not eligible for the home repair programs (unclear title or multi-owner status)

- Still responsible for property taxes on a structure that the city may eventually condemn

- Sitting on a property that's losing value every month, it sits storm-damaged

And the clock is not stopping. Vacant damaged properties carry ongoing costs — insurance, utilities, taxes, liability — that pile up whether you're actively making decisions or not. Vacant homes are also magnets for vandalism and secondary weather damage, and most insurance carriers will void coverage on a vacant structure if utilities aren't maintained. That means additional damage after the tornado may fall entirely on the owner.

Your property may fall outside city assistance programs if:

- It was vacant or condemned before May 16, 2025

- You or your family owns multiple properties in the tornado corridor

- The deed is in the name of someone who has passed away (heirs' property)

- You missed the FEMA registration window (closed September 2025)

- The property didn't have active homeowner's insurance at the time of the storm

- The home sustained damage but isn't formally condemned — sitting in a gray zone

Why Waiting on Government Programs Can Cost You More Than You Think

There's an understandable instinct to wait and see — to watch the Rams bill move through the Board of Aldermen, keep an eye on which neighborhoods get prioritized for repair funds, and hope your block ends up in the right pipeline. That's a reasonable hope. But it's worth being clear about what waiting costs while it plays out.

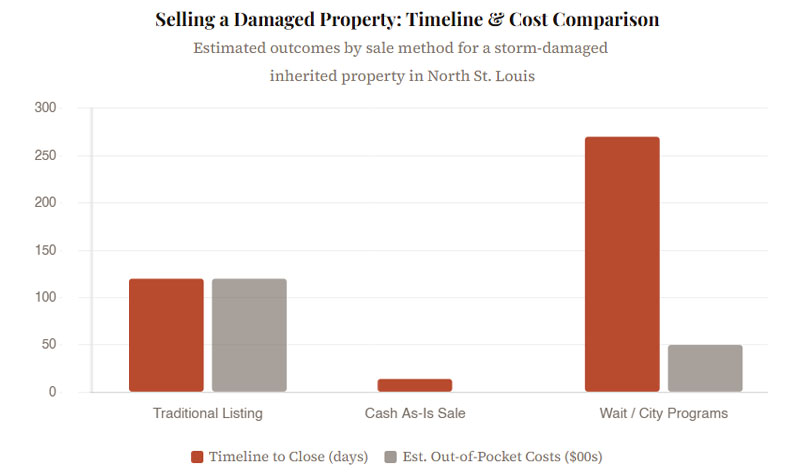

As of January 2026, the St. Louis median home price was $223,000, with properties sitting on the market for an average of 49 days before closing under normal conditions. Storm-damaged properties don't sell in 49 days on the traditional market. They require inspections, disclosure negotiations, and buyers willing to absorb repair costs — a dramatically smaller buyer pool, especially in neighborhoods where comparable properties are also damaged.

Meanwhile, property taxes don't pause for disaster recovery. Neither do HOA fees, if applicable. Neither do utility carrying costs if you're trying to maintain insurance coverage. And if the city condemns your property — a real possibility for structures that remain in deteriorated condition — you lose control of the demolition timeline entirely. Demolition liens can attach to the property and complicate any future sale or transfer to heirs.

The city has also been explicit that SB1 funds and Rams settlement funds are finite. Julian Nicks and other officials have repeatedly said these programs will prioritize "major street corridors" and properties that fit the formal demolition criteria. If your property is on a block that doesn't qualify, or if the fund runs dry before your application is processed, there is no guarantee of a second shot.

The Straightforward Alternative Most People Haven't Considered

There is another option — and it doesn't involve waiting for a government program that may never reach you, paying thousands for private debris removal, or trying to list a storm-damaged property on Zillow and hoping for the best.

Cash home buyers who specialize in distressed and as-is properties have been operating in the St. Louis market for years, and the post-tornado environment has made their services significantly more relevant. These aren't the same as the predatory "vultures" who showed up on doorsteps the morning after the storm with lowball offers designed to prey on shock. Legitimate cash buyers in the current market work on a transparent process: you get a fair offer, you choose your closing date, and you walk away without paying for debris removal, repairs, demolition, or agent commissions.

For heirs sitting on inherited North St. Louis property, a cash sale has specific advantages that go beyond just speed. Missouri imposes no inheritance tax or estate tax, meaning heirs receive their proceeds without state-level deductions for inheriting. At the federal level, inherited property also typically receives a stepped-up cost basis equal to fair market value at the time the previous owner passed, which can significantly reduce or eliminate capital gains tax if you sell reasonably soon after inheriting. That's real money back in your pocket compared to holding a condemned structure and accumulating carrying costs while the city's recovery programs inch forward.

How the Process Actually Works — No Surprises

If you've never sold a cash home before, here's what the process looks like when working with a legitimate buyer. It's genuinely simpler than most people expect:

1. Contact and Property Assessment

You reach out, share the address, and basic condition. A reputable buyer visits or reviews remotely and provides a no-obligation cash offer—typically within 24 to 48 hours. No cleaning, staging, or repairs required.

2. Review the Offer on Your Terms

There's no pressure to accept. Review the offer, ask questions, and take the time you need. A trustworthy buyer will explain how the offer was calculated and what they plan to do with the property.

3. Title and Paperwork — They Handle It

Even properties with probate issues, heirs' property situations, or missing deeds can often be resolved. Experienced cash buyers work with title companies that regularly handle these challenges.

4. Choose Your Closing Date

Close in as little as 7–14 days or choose a later date that fits your situation. No lender approval delays, appraisal contingencies, or financing issues that can derail the sale.

5. Walk Away with Cash

No agent commissions, closing costs, or debris removal bills. The buyer purchases the property as-is, allowing you to move forward without additional expenses or surprises.

A Note on Avoiding Predatory Buyers

It would be dishonest not to address this directly: in the weeks after the May 2025 tornado, North St. Louis was flooded with real estate speculators. Door knocks, phone calls, handwritten flyers — many of them offering shockingly low prices to families still in shock. That predatory activity is real, and it left a lot of people understandably skeptical of anyone trying to buy distressed property.

The difference between a legitimate cash buyer and a predatory one is transparency. A legitimate buyer will explain how they arrived at their number, give you time to compare offers, and never pressure you into signing the same week. They'll also be upfront that a cash offer will be below full market value — that's the trade-off for speed, certainty, and zero repair costs. A predatory buyer hides that math, creates urgency, and disappears once they've locked you into an unfavorable contract.

Missouri's real estate market has fewer wholesaler disclosure requirements than states like Ohio and Pennsylvania. That means you need to ask the right questions. Get the offer in writing. Ask how they calculated the number. Ask specifically what fees, if any, are deducted from your proceeds at closing. If those questions make someone evasive, keep looking.

📝 Before You Sign Anything

Questions to ask any cash buyer:

The Bottom Line

The $110 million in the Rams bill represents real progress — and the people who fought to get that allocation into the legislation deserve real credit. But for everyone whose property doesn't fit the program criteria, whose title is complicated, whose insurance lapsed, or who simply needs to move on from a house that became a burden rather than an asset, that bill is not the answer.

If you're sitting on a storm-damaged, inherited, or distressed property in North St. Louis and the government programs aren't reaching you, the best thing you can do is understand your options clearly before another month of carrying costs passes. A cash sale won't get you peak market value — no distressed sale will. But it will get you certainty, speed, zero out-of-pocket costs, and the ability to put this chapter behind you.

We've helped St. Louis families in exactly this situation. If you want an honest conversation about what your property is actually worth and what the process looks like, give us a call or fill out a form online. There's no obligation and no pressure. You'll at least know the number — and knowing is always better than waiting.

Ready to Buy or Sell in St. Louis? House Sold Easy Has You Covered!

Navigating St. Louis’ red-hot luxury market doesn’t have to be a headache. With House Sold Easy, it’s all about less hassle—we’ve got you covered from start to finish. Our St. Louis experts know every corner of this city and will make buying your dream home or selling your high-end property a breeze. Don’t miss out on the hottest market in the U.S.! Contact House Sold Easy today and let’s make your real estate goals happen!