5 St. Louis Real Estate Hacks for Buyers & Investors

Jun 05, 2026

Written by David Dodge

Hyper-local strategies built on the freshest June 2026 market data — whether you're buying your first home, pricing to sell, or trying to crack into investing without getting crushed by today's rates.

Every week someone asks me some version of the same question: "Is now a good time to do something in St. Louis real estate?"

The honest answer, as of June 2026, is that it depends entirely on who you are and what you're trying to accomplish. This market is bifurcated in ways that reward people who understand the nuance—and quietly punish those who treat it like one big, monolithic market.

So let's skip the vague national headlines. Here are five specific, actionable hacks for the exact moment we're in — pulled straight from the June 2026 data on our local market, not from some 30,000-foot think piece out of New York

Sale Price

Supply

(Late Apr)

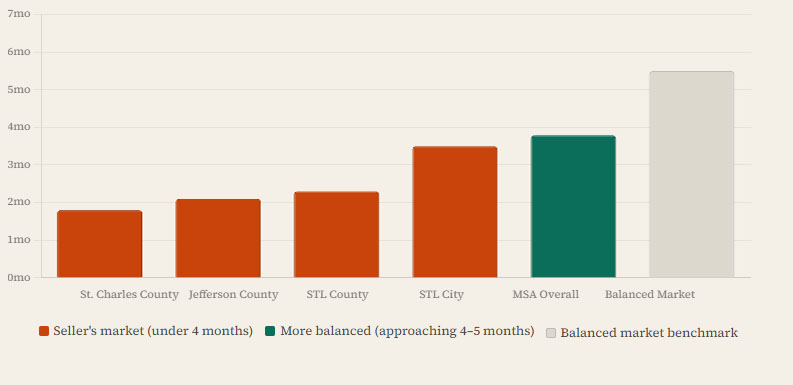

St. Louis Metro: Months of Housing Supply by Area (June 2026)

Source: eMetropolitan St. Louis Housing Market Report, April–May 2026. A balanced market = 5–6 months supply.

That chart tells you everything you need to know before making a single move in this market. Suburbs are starved for inventory. The city has more breathing room. And nobody — nobody — is at that balanced 5.5-month benchmark yet. Keep that picture in your head as we walk through each hack.

1. For First-Time Buyers

The "Free Cash" Hack: Missouri's Grant Programs Most People Don't Know Exist

I talk to first-time buyers every week who have been sitting on the sidelines, convinced they don't have enough saved to get into the market. And more often than not, what stops them isn't the income — it's a down payment assumption that's completely out of date.

Here's what's actually available to you right now. Missouri's MHDC First Place Loan program offers up to 4% of the loan amount as cash assistance toward your down payment or closing costs. On a $240,000 home — which is roughly the St. Louis metro median — that means many buyers are closing with less than $10,000 out of pocket when you stack the programs correctly. FHA loans require just 3.5% down with a 580+ credit score, VA and USDA loans are at 0% for eligible buyers, and conventional loans can go as low as 3% for qualifying first-timers.3

The MHDC program income limits are broader than most people expect. A 15-minute call with a participating lender can quickly tell you what you qualify for—so don't rule yourself out before making that call.

In competitive spring and summer markets, available funding can move fast. June is a critical window to explore your options.

Now, about where to look. If you've been losing bidding wars in Webster Groves or Kirkwood, I'd encourage you to give Affton and Overland a serious second look. Entry-level inventory in both neighborhoods has ticked up slightly this spring, which means you're getting something rare: real leverage as a buyer. We're not talking depressed markets — these are solid, established zip codes with good bones and tight community character. You're just not competing against eight other offers on a two-bedroom bungalow anymore.

The window is open. The programs are real. St. Louis remains roughly 21% less expensive than the national housing average, and that gap continues to draw buyers who've been priced out elsewhere. Don't wait for conditions to be perfect — they won't be. Use the tools available and get in while the programs are funded.

2. For Sellers

The "County vs. City" Pricing Hack: Why Your Location Changes Everything

This is the one that trips up sellers more than anything else in June 2026. People see a headline — "St. Louis is a seller's market" — and assume that applies equally everywhere in the metro. It doesn't. And the difference between pricing strategy in St. Louis County versus St. Louis City right now is significant enough to cost you real money if you get it wrong.

Let me give you the actual numbers. According to eMetropolitan's April/May 2026 market report, St. Louis County is sitting on a tight 2.3-month supply of homes. Buyers in the county paid an average of 100.6% of the list price — meaning they paid over asking. St. Charles County is even tighter, with Jefferson County buyers paying 101.3% of the list price. If you're selling a move-in-ready home in a desirable county school district right now, you have pricing power. Use it. Price aggressively. The data supports you.

2.3 months of supply or less

Buyers paying over list price

Homes are selling in just 7–10 days

3.5 months of supply

Buyers are paying 98.6% of the list price

Average market time of ~17 days

St. Louis City tells a different story. The city currently holds a 3.5-month supply, and while that's still technically a seller's market, buyers there are negotiating in ways their county counterparts simply can't. The 98.6% sale-to-list ratio is actually good — it means you're almost certainly getting close to your asking price — but it also means you need to price correctly from day one rather than pricing high and hoping. In the city, your magic number is pricing at exactly 98% of recent comps for comparable, well-maintained properties. Anything higher and you risk sitting, which in this market can create the perception of a problem even when there isn't one.

The other non-negotiable for county sellers right now: pre-listing inspections. Buyers are back to inspecting everything and using findings as negotiating leverage. Get ahead of it. Know your home's condition before they do, fix what you reasonably can, and price around what you can't. It prevents deals from dying after ratification — one of the most costly scenarios any seller can face.

3. For New Investors

The "House Hacking" Hack: How South City Duplexes Beat Today's Rates

If you're a first-time investor staring at a 6.4% mortgage rate and wondering how on earth real estate investing still makes sense, I want to introduce you to the strategy that local investors have been using in St. Louis for decades. It's hiding in plain sight among the brick two-family homes of South City, and it's called house hacking.

The concept is simple: you buy a duplex or small multi-family property, move into one unit, and rent out the other(s). The rental income offsets your mortgage. In the right deal, it offsets it completely — meaning you're building equity while your tenant essentially covers your housing costs.

Here's why the math works so well in St. Louis specifically. The FHA loan limit for two-unit properties in Missouri jumped to $693,050 for 2026, which gives you plenty of runway to buy a quality, renovated building in even the most competitive South City pockets. More importantly, FHA only requires 3.5% down on multi-family properties up to four units — provided you occupy one unit for at least a year. On a $350,000 duplex in Tower Grove East or Dutchtown, a conventional investment loan would require $87,500 down. An FHA loan brings that to just $12,250.

A duplex in Dutchtown or Tower Grove East at around $320,000 could work with an FHA loan at 3.5% down, roughly $11,200 down.

You live in one unit and rent out the other. FHA allows 75% of projected rental income to count toward your qualifying income, which means some buyers who may not qualify on salary alone could qualify once the rental math is included.

St. Louis is uniquely built for this strategy. Our architecture is dominated by historic multi-family buildings — the brick duplex is practically the city's architectural signature. Unlike coastal markets where two-family homes are priced into the stratosphere, St. Louis home prices remain roughly 48% below the national average, yet rental demand continues to climb. The metro-area average rent is rising, with the St. Louis metro rental market posting 3.6% year-over-year growth. That's your income floor, and it's holding strong.

After meeting FHA's 12-month occupancy requirement, you have options: refinance into a conventional loan and buy another FHA property, keep the loan and enjoy the cash flow, or use the equity you've built as a springboard into your next investment. This isn't a get-rich-quick scheme — it's the slow, boring, genuinely effective playbook that local investors have used to build portfolios here for 30 years.

4. The Ultimate Time-Saver

The Speed Hack: When the Math Says Skip the Market Entirely

Here's the hack nobody wants to hear — but the one that might be the most valuable for a specific subset of sellers reading this right now.

The St. Louis market in June 2026 is rewarding turnkey homes. Move-in-ready properties in desirable school districts are still moving fast and getting strong prices. But if you're sitting on a property that needs $25,000 to $40,000 in work just to compete with those listings, the traditional market math may not favor you the way you think it does. Let's walk through it honestly.

You spend $30,000 updating your kitchen and bathrooms to compete with renovated county listings. That takes 3–4 months and your time, energy, and upfront cash. Then you list, carry the home through 30–60 days of showings, negotiate with buyers who still try to use inspection findings as leverage, wait through a 30–45 day closing, and pay agent commissions of 5–6% on top of it all. By the time you add it up — holding costs, carrying costs, repair costs, commission, and the time value of your capital sitting in that house for six-plus months — the math often looks very different than the gross sale price suggests.

A record 34% of home sellers nationally cut their list price in February 2026. Days on market averaged 57 days in January nationally, compared to just 33 days during the peak May–June season.

The takeaway? Every month you delay past peak season can cost you leverage, buyer demand, and potentially thousands in lost value.

For sellers in this position, the ultimate hack is bypassing the traditional market entirely through a direct cash sale. No staging costs. No repair negotiations. No waiting on buyer financing contingencies. No volatility from interest rate fluctuations between contract and closing. You know your number, you know your timeline, and you move on with your life.

This isn't the right move for everyone — if your home is in strong shape and in a high-demand area, the traditional market will likely net you more. But for sellers with deferred maintenance, complex situations, or simply a strong preference for certainty over potential upside, the speed hack is real and worth running the numbers on before you commit to a six-month renovation-and-listing cycle.

5. For Everyone

The "Know Your Sub-Market" Hack: Stop Treating St. Louis Like One Market

I'll leave you with the meta-hack that makes all the others possible: St. Louis is not one market. It never has been. But the gap between sub-markets in June 2026 is wider than it's been in years, and acting on imprecise information is costing buyers, sellers, and investors real money.

A buyer who hears "St. Louis is competitive" and assumes that means they should waive inspection and offer $30,000 over asking on a City listing is making a costly mistake. A seller in a City neighborhood who prices their home like it's in a Ladue school district is going to sit and wonder why. An investor who buys a four-family in a neighborhood without checking current rental demand is operating blind.

The data is available. eMetropolitan publishes detailed monthly market reports that break down inventory, pricing, and days on market down to the county level. St. Louis REALTORS® publishes monthly housing data. Your agent should be able to tell you the months-supply figure for the specific zip code you're targeting — not just the MSA average.

Winning in this market isn't about being the most aggressive. It's about being the most informed.

Ready to Buy or Sell in St. Louis? House Sold Easy Has You Covered!

Navigating St. Louis’ red-hot luxury market doesn’t have to be a headache. With House Sold Easy, it’s all about less hassle—we’ve got you covered from start to finish. Our St. Louis experts know every corner of this city and will make buying your dream home or selling your high-end property a breeze. Don’t miss out on the hottest market in the U.S.! Contact House Sold Easy today and let’s make your real estate goals happen!