St. Louis Real Estate: Why Waiting for Rates is a Trap

Jul 18, 2026

Written by David Dodge

The Relatable Problem: The Psychological Toll of 6.5%

You want to buy a home. You’ve saved the down payment, your credit score is pristine, and you spend your evenings scrolling through Zillow listings in St. Charles and Florissant. But every time you run the numbers through a mortgage calculator, looking at a 6.5% mortgage rate makes you physically sick.

You remember 2020 and 2021. You remember your friends locking in sub-3% rates. Because of that psychological anchor, you make a seemingly logical decision: "I am going to wait until rates drop back to 4% before I buy my first home."

It feels like the prudent, financially responsible thing to do. You decide to sign another year-long lease on your apartment, sit on your down payment cash, and wait for the macroeconomic tides to turn in your favor.

The Reality: The Hidden Cost of the Waiting Trap

Trying to time the mortgage market is one of the most dangerous financial traps a first-time homebuyer can fall into. The problem with waiting for the perfect interest rate is that the rest of the economy does not hit "pause" while you wait.

While you sit on the sidelines holding out for a miraculous return to pandemic-era interest rates, two very distinct financial forces are actively working against your wealth-building goals: climbing rent prices and persistent home appreciation.

Force 1: St. Louis Rents Are Quietly Creeping Up

If you aren't buying, you are renting. And renting in St. Louis in 2026 is getting more expensive. According to the latest

While St. Louis remains significantly more affordable than the national average—running about 33% below national median rents—the trajectory is pointing firmly upward. St. Louis rent prices have quietly continued to creep up, rising 4.0% year-over-year.

What does that mean in practical terms? Renters today are paying roughly $85 more per month on average than they were last year just to stay in the same apartments.

-

1-Bedroom Units: Averaging $1,095/month.

-

2-Bedroom Units: Averaging $1,425/month.

-

Single-family rental houses: Averaging $1,590/month.

Every month you wait for a 4% mortgage, you are paying 100% interest to your landlord. A year of waiting costs you over $15,600 in base rent for an average apartment—money that builds zero equity and offers zero tax advantages. For a deeper look at the neighborhood-by-neighborhood breakdown,

Force 2: The Bidding War Threat

Let’s play out your ideal scenario. Let’s imagine it is early 2027, and the Federal Reserve has slashed rates. Mortgage rates suddenly plunge to 4.5%. You rejoice, pull out your pre-approval letter, and get ready to buy that 3-bedroom ranch in Florissant.

You are not the only one.

There is massive pent-up demand in the St. Louis market. Thousands of other sidelined buyers have been playing the same waiting game as you. If rates drop significantly, that dam will break. A flood of buyers will enter the St. Louis market simultaneously.

When demand skyrockets and inventory remains constrained, we know exactly what happens: brutal bidding wars.

Instead of negotiating with a seller on a $280,000 home (the current average home price in St. Louis as of 2026), you are suddenly competing against ten other offers. You are forced to waive your inspection contingencies, cover appraisal gaps in cash, and bid $30,000 over the asking price just to get your foot in the door.

According to

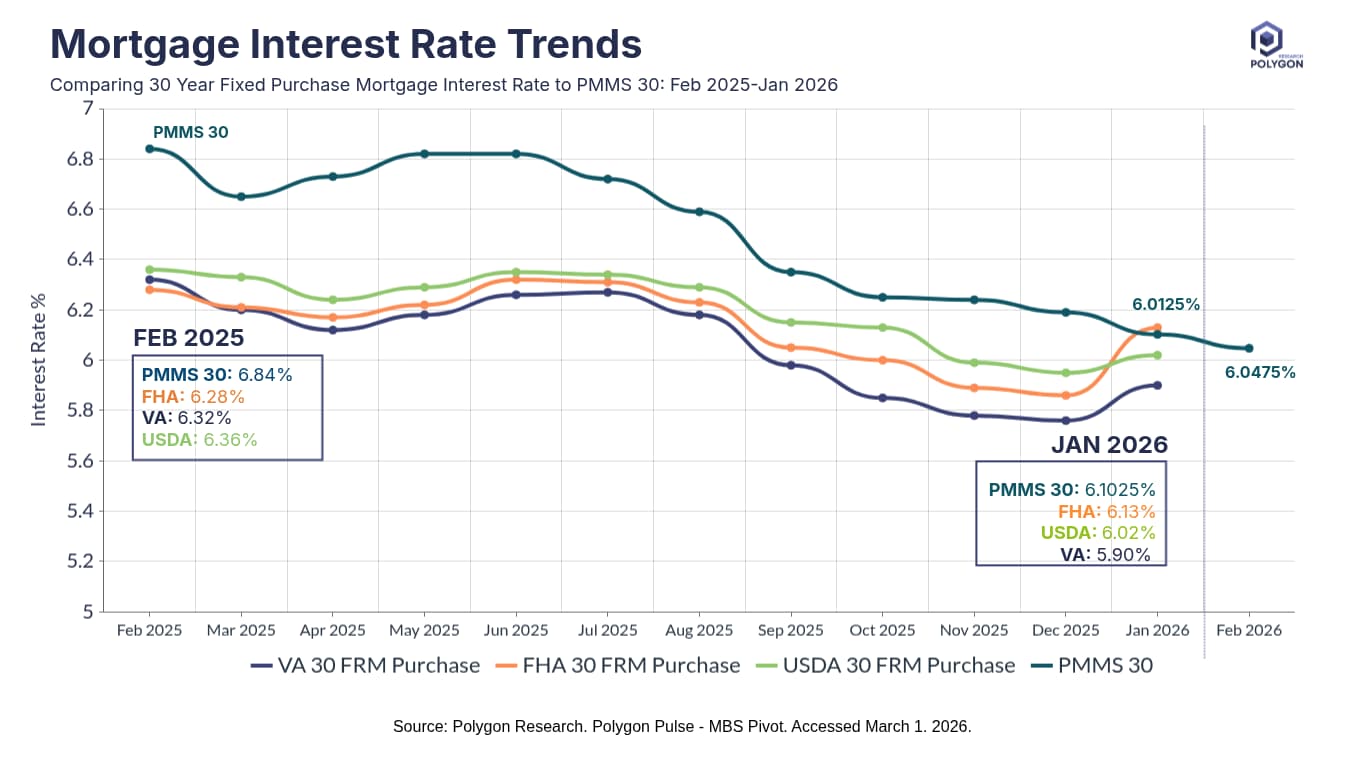

The Mortgage Rate Reality Check

It is crucial to look at actual data rather than relying on nostalgia for 2021. According to the

Freddie Mac Mortgage Rate Trends 2025-2026. Source: Polygon Research

While 6.49% is higher than a few years ago, it is completely normal from a historical perspective. Furthermore, waiting for 4% might mean waiting for a decade. The

If you are waiting for a crash, you will be disappointed. Inventory is slowly improving, but not at a rate that will cause prices to plummet.

The Solution: Date the Rate, Marry the House

In the real estate industry, we have a saying for this exact economic climate: Date the rate, marry the house.

Interest rates are temporary. The purchase price of a home is permanent.

If you can comfortably afford the monthly payment today at 6.49%, buy the house now. By buying in a higher-rate environment, you have leverage. You have the luxury of actually doing a home inspection without losing the deal. You can negotiate closing costs with the seller. You can take your time deciding between a historic home in St. Charles or a solid mid-century build in Florissant.

Look at the mathematical comparison of buying a $280,000 home today versus waiting a year:

| Scenario | Buy Today (2026) | Wait for 2027 Rates Drop, Prices Rise |

|---|---|---|

|

Purchase Price |

$280,000 |

$294,000 Assumes 5% appreciation |

|

Interest Rate |

6.49% |

5.50% |

|

Down Payment (10%) |

$28,000 |

$29,400 |

|

Loan Amount |

$252,000 |

$264,600 |

|

Estimated Monthly P&I |

Approximately $1,592 |

Approximately $1,502 |

|

Bidding War Risk |

Low to Moderate |

High |

|

Ability to Negotiate |

Yes |

No |

Note: P&I is Principal and Interest only. Taxes and insurance are extra.

Yes, waiting drops the monthly payment by about $90. But to get that $90, you spent $15,600 on rent for a year, had to put down more cash for the down payment, paid a higher overall price for the house, and likely lost your ability to negotiate.

And remember the golden rule of "dating the rate": If you buy today and rates drop to 5.5% next year, you can just refinance. You get to keep your lower 2026 purchase price, but you get the 2027 interest rate. It is a win-win.

Conclusion: Take Control of Your Timeline

At House Sold Easy, we see buyers struggle with this exact dilemma every day. The impulse to wait for the "perfect" market conditions is natural, but real estate isn't about perfection—it's about positioning. The reality is that there is no perfect time to buy a house, only the right time for you.

When you choose to wait on the sidelines, you aren't actually avoiding the market; you are just shifting your financial exposure to the rental market, where you are guaranteed a 100% loss on your monthly housing payment. Buying now, even with interest rates sitting in the mid-sixes, allows you to lock in your purchase price and begin building equity immediately in the St. Louis market.

If the monthly numbers work for your budget today, the smartest move is to secure the property while you still have the negotiating power to do so on your own terms. Whether you are exploring traditional financing or looking into owner financing options, securing your footprint in St. Charles or Florissant today protects you from the inevitable bidding wars of tomorrow. Stop playing the waiting game, date the rate, and marry the house.

Ready to Buy or Sell in St. Louis? House Sold Easy Has You Covered!

Whether you're thinking about listing your home or exploring a cash offer, it's worth understanding all of your options before making a decision. The right choice depends on your timeline, your property's condition, and your goals. Contact House Sold Easy to discuss your situation and see what makes the most sense for you.Our St. Louis experts know every corner of this city and will make buying your dream home or selling your high-end property a breeze. Don’t miss out on the hottest market in the U.S.! Contact House Sold Easy today and let’s make your real estate goals happen!