1997 Tax Trap: Why St. Louis Homeowners Won't Sell

Jun 18, 2026

Written by House Sold Easy Team

A nearly 30-year-old tax law is quietly trapping millions of homeowners — and right here in Kirkwood, Webster Groves, and Ladue, the numbers are bigger than most people realize.

Many longtime St. Louis homeowners have built substantial equity over the years. The problem is that selling can trigger a tax bill large enough to make them think twice about moving. — not because they want to stay, but because selling would hand the IRS a check they never saw coming.

This isn't just affecting a handful of homeowners. It's becoming a real issue for people who bought decades ago and are now considering downsizing or relocating, and it has a very specific local angle that anyone who owns — or inherited — a home in Kirkwood, Webster Groves, Ladue, or similar established pockets of the St. Louis metro should understand before they ever call a traditional listing agent.

Why the 1997 Tax Rule Matters Today

In 1997, Congress passed the Taxpayer Relief Act, which included what seemed like a genuinely helpful benefit for homeowners. Under Section 121 of the Internal Revenue Code, you could sell your primary residence and exclude up to $250,000 of profit from capital gains taxes — $500,000 if you were married and filing jointly. All you had to do was have lived in the home for two of the last five years.

At the time, that was more than enough cushion. The median home price in the U.S. in 1997 was roughly $127,000. A $250,000 exclusion covered almost any realistic gain a typical homeowner might see. The rule was clean, simple, and genuinely protective of the average American who had built equity in their home over the years.

The problem? Congress never tied that number to inflation. It has sat at $250,000 for single filers and $500,000 for married couples for almost three decades, untouched, while home values have done anything but stay flat.

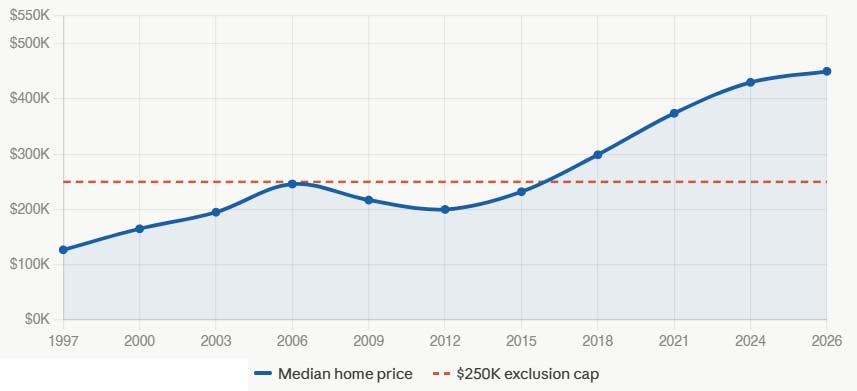

How the $250K exclusion cap has lost ground to real home prices

Median U.S. home price vs. Section 121 exclusion limit (1997–2026, single filer). Sources: CBIZ, NAR, Redfin.

Today, the national median home price sits somewhere between $400,000 and $460,000. In expensive coastal markets, it is well over $1 million. And here in St. Louis — which has historically been more affordable than those coastal cities — long-term homeowners in desirable neighborhoods have still watched their values climb dramatically. In 2026, the broader St. Louis market posted a 10% year-over-year appreciation rate, and inventory sits at a critically tight 2.4 months of supply, well below the 5-to-6-month level that defines a balanced market.

Adjusted for inflation, the 1997 thresholds would be worth approximately $475,000 for single filers and $950,000 for married couples in today's dollars. As home values have risen, more homeowners are finding that the exclusion doesn't stretch as far as it once did.

"Homeowners are facing a looming tax penalty simply for staying in their homes too long. These outdated thresholds are already distorting the housing market, limiting available inventory, and making it harder for many owners to move without triggering a significant tax bill." - National Association of Realtors NAR

13 Million Americans in the Same Trap — Including People Right Here in St. Louis

A report that made headlines in May 2026 put a real number on this problem. An estimated 13.1 million U.S. homeowners — roughly 15% of all owner-occupied households — already have gains above the current capital gains thresholds, meaning they face a real tax bill the moment they sell. That number is expected to grow significantly in the coming years.

The National Association of Realtors found that 25.4 million homeowners now hold prospective profit gains above $250,000, and that without legislative reform, 56% of all homeowners could exceed these limits by 2030. That is not a distant, theoretical problem. That is a wave that is already cresting.

Congress has noticed. In early 2026, the "More Homes on the Market Act" — which would double the exclusion to $500,000 for single filers and $1 million for married couples, and tie it to inflation in the future — had bipartisan support with 94 cosponsors. President Trump also publicly raised the idea of eliminating the capital gains tax on home sales. Lawmakers have proposed raising the exclusion limits, but no changes have been approved yet. For now, homeowners need to plan based on the rules currently in place.

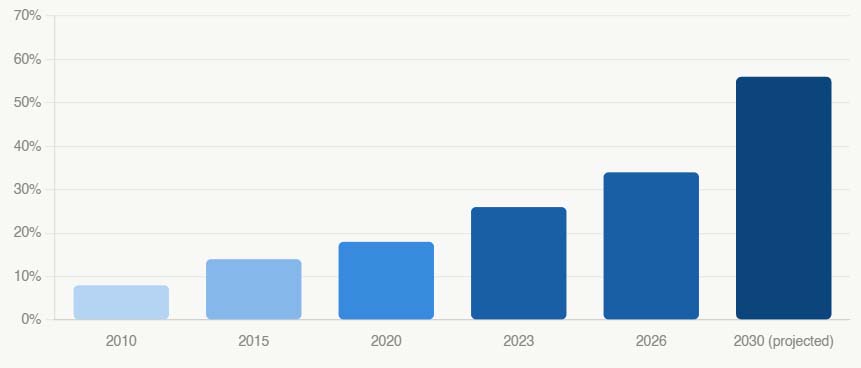

Share of homeowners exposed to capital gains taxes at sale — projected growth

Percentage of U.S. homeowners with gains above the exclusion cap

source: National Association of Realtors (NAR), 2026.

What This Looks Like in Kirkwood, Webster Groves, and Ladue

Here's what that can look like in neighborhoods such as Kirkwood, Webster Groves, and Ladue. If you bought a house in Kirkwood in 1995 for $180,000, you may be looking at a home worth well north of $500,000 today. Kirkwood values alone have climbed more than 43% over just the last five years, according to local market reporting from May 2026. A home worth $400,000 in 2020 is likely worth over $560,000 right now.

Run the math on a longer time horizon — say, someone who bought in Ladue in the early 1990s for $250,000 — and you could be staring down a current market value of $900,000 or more in that neighborhood, where the median listing price is around $2.29 million. After you apply the $500,000 married-couple exclusion, the taxable gain could easily clear $150,000, $200,000, or beyond.

And that is before you factor in Missouri state income tax on top of the federal capital gains rate, or the 3.8% Net Investment Income Tax that kicks in for higher earners. The total bite on a large gain can reach 35% or more when you add everything up.

Then add a traditional real estate agent commission — often 5-6% of the sale price — and suddenly the homeowner who "did everything right" for 30 years is watching a third or more of their equity walk out the door in fees and taxes the moment they sign at closing.

For many homeowners, these costs become a major factor when deciding whether selling still makes financial sense. Not because they do not want to move. Not because they do not need to downsize, or relocate, or pass assets to their children. But because the math, the way the traditional sales process is structured, makes the decision feel financially punishing.

Did you inherit a family home in the St. Louis area? Inherited properties come with unique capital gains considerations, especially when it comes to cost basis. If the home has been in the family for decades, the appreciated value could create a significant tax burden that many heirs don't discover until it's almost too late to plan for it.

There Are Alternatives — and They Are Worth Understanding

There are alternatives that some homeowners choose to explore before listing on the open market.: selling your home through a direct sale or a structured owner-financing arrangement is a legitimate, legal, and often significantly more tax-efficient path for long-term homeowners with large embedded gains.

Direct sales

Selling directly to a buyer — rather than listing on the open market through an agent — eliminates the commission layer, which on a $600,000 home can easily be $30,000 to $36,000 in fees alone. A direct buyer is often willing to move quickly and on terms that work for the seller, which means you keep more of what you earned.

Owner financing (installment sales)

One option worth discussing with a tax professional is an installment sale through owner financing. In a seller-financed or owner-financed deal, you act as the bank. The buyer makes payments to you over time, and critically, you only recognize the gain as you receive payments — not all at once in the year you close. Under IRS installment sale rules (Section 453), this can spread your taxable gain over several years, potentially keeping you in a lower capital gains tax bracket each year and dramatically reducing your total tax exposure.

For someone sitting on a $400,000 gain in Kirkwood or Webster Groves, the difference between recognizing that all in year one versus spreading it over five or seven years can be tens of thousands of dollars in actual tax savings. It is not a loophole. It is exactly how the tax code is designed to work — and most homeowners simply never hear about it because traditional real estate agents have no particular reason to bring it up.

1031 exchanges (for investment properties)

If the appreciated property is not your primary residence — say, it is a rental or investment home you inherited — a 1031 exchange lets you roll the gains into a new investment property and defer the tax indefinitely. This is a more complex transaction that requires careful timing and a qualified intermediary, but for the right situation, it can be a powerful tool.

The Bigger Picture: Why This Matters for the St. Louis Market

This is not just a personal finance story. The capital gains lock-in effect is one of the reasons housing inventory remains so constrained in established St. Louis neighborhoods. When long-term owners cannot afford — from a tax perspective — to sell, those homes stay off the market. First-time buyers and growing families cannot access them. The ripple effect compresses supply and pushes prices higher across the board.

Moody's Analytics has noted that updating the capital gains exclusion limits could unlock hundreds of thousands of homes nationally and meaningfully boost inventory. The St. Louis market, with its 2.4-month supply and 10% annual appreciation, would feel that kind of release. The inventory of single-family homes in the area has already decreased by about 13.6% compared to prior periods, per Norada Real Estate's 2026 analysis.

Whether Congress eventually acts on this — and the bipartisan energy around the More Homes on the Market Act suggests there is real momentum — the practical reality for a homeowner in Kirkwood or Ladue today is that waiting for legislation is not a strategy. The gains will keep accumulating, the tax exposure will keep growing, and the longer you wait without a plan, the fewer good options you have.

The Bottom Line for St. Louis Long-Term Owners

If you bought your home in the St. Louis area decades ago, or if you inherited a property that has been in the family since the '90s, you may be sitting on more equity than you realize — and facing more tax exposure than anyone has ever walked you through. The 1997 law was designed for a world where $250,000 in home appreciation was essentially the ceiling. That world no longer exists, especially not in Kirkwood, Webster Groves, or Ladue.

Every homeowner's situation is different. If you've owned your home for decades or inherited a property, it may be worth reviewing your potential tax exposure before deciding how to sell. Understanding your options early can help you avoid surprises later.

What it does require is having an honest conversation about what you actually walk away with — not just the sale price on the listing, but the after-tax, after-fee number that ends up in your bank account. That number is what matters. And for a lot of long-term St. Louis homeowners right now, there is a better path to maximizing it than the traditional route.

This article is for informational purposes only and does not constitute tax or legal advice. Consult a qualified tax professional before making decisions about your home sale or any tax strategy.

Ready to Buy or Sell in St. Louis? House Sold Easy Has You Covered!

Whether you're thinking about listing your home or exploring a cash offer, it's worth understanding all of your options before making a decision. The right choice depends on your timeline, your property's condition, and your goals. Contact House Sold Easy to discuss your situation and see what makes the most sense for you.Our St. Louis experts know every corner of this city and will make buying your dream home or selling your high-end property a breeze. Don’t miss out on the hottest market in the U.S.! Contact House Sold Easy today and let’s make your real estate goals happen!