How to Avoid Foreclosure in Missouri with a Fast Cash Home Sale (2026)

Mar 20, 2026

Written by David Dodge

Nobody buys a home expecting to face foreclosure. But life happens — job loss, divorce, medical bills, a death in the family, or just a run of bad luck that piles up faster than you can manage. If you’re a Missouri homeowner who’s fallen behind on payments, you have more options than you think. One of the fastest, least stressful paths is selling your home for cash before the bank takes it.

Missouri Foreclosure in 2026: The Numbers

Foreclosure filings in Missouri have been rising since pandemic-era protections expired. Understanding where things stand is the first step to making a smart decision.

Missouri foreclosure filings

+18%

Year-over-year, 2025–2026

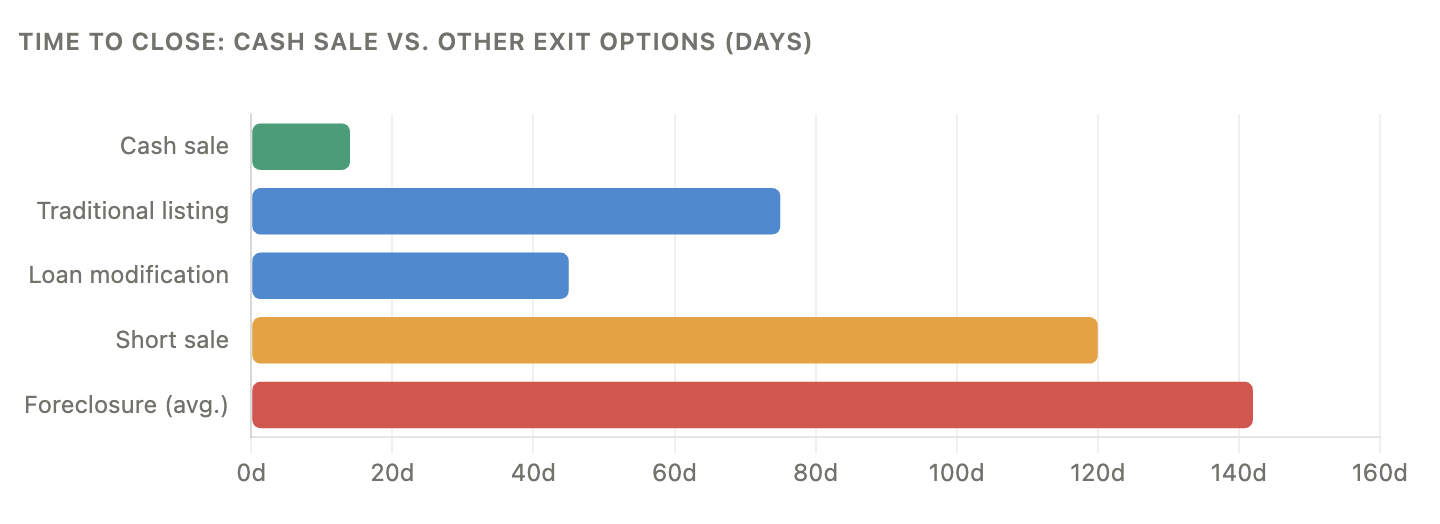

Avg. days to foreclosure sale

142

Missouri (non-judicial state)

Cash sale close time

7–14

Days to close with a cash buyer

Credit score drop

−150

Avg. points lost from foreclosure

The Missouri Foreclosure Timeline: What You’re Up Against

Missouri is primarily a non-judicial foreclosure state, which means lenders don’t need a court order to foreclose. They can move fast — and the timeline is shorter than most homeowners realize.

Under RSMo § 443.310, Missouri law requires the trustee’s sale to be published in a local newspaper for 20 consecutive weeks before the auction. You also receive written notice. Once the gavel drops at the trustee’s sale, it’s over — Missouri has no statutory right of redemption after the sale.

⚠ Critical Window

If you’re 90+ days behind on payments, the clock is already running. Most Missouri homeowners have a window of roughly 60–90 days to act before the trustee’s sale date is locked in. Acting in that window is the difference between walking away with equity and walking away with nothing.

The Real Cost of Letting Foreclosure Happen

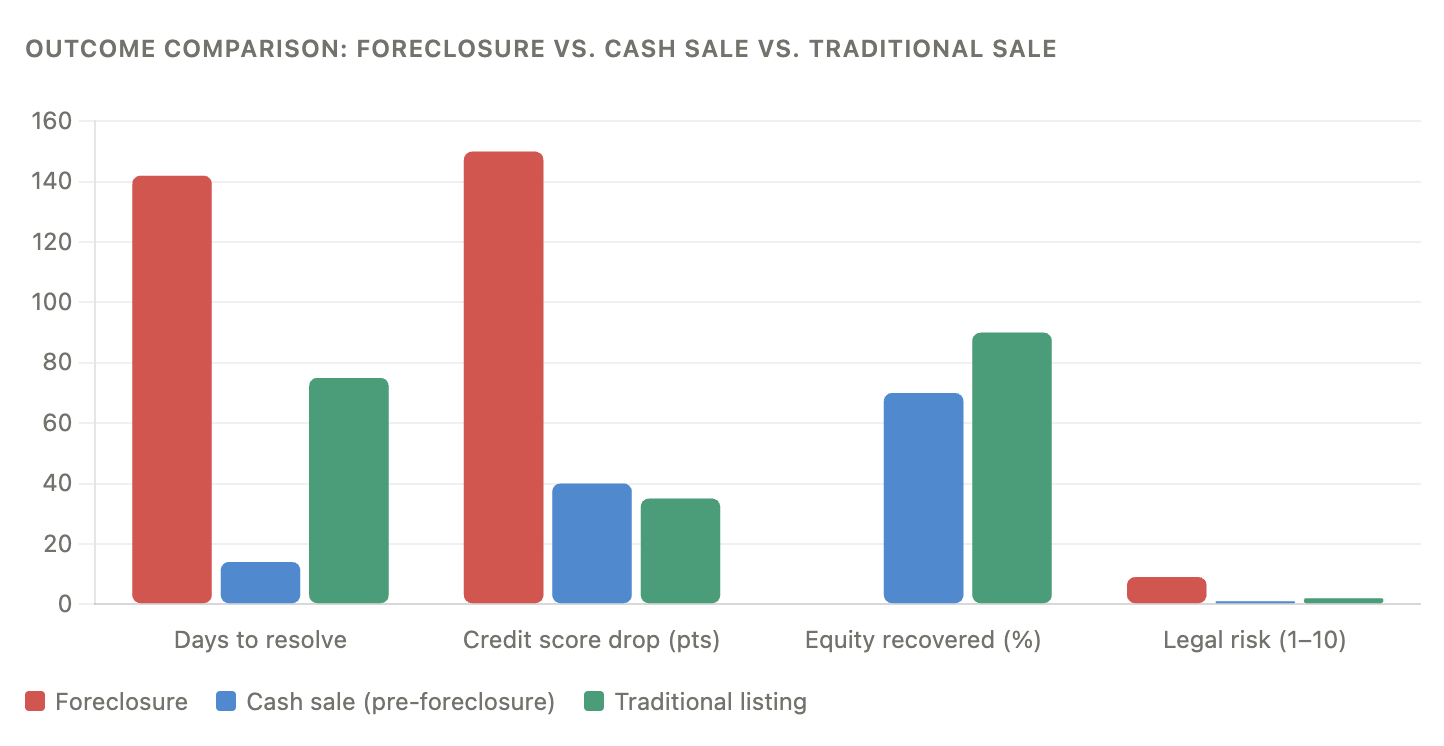

A lot of homeowners freeze up — partly from shame, partly because they don’t know their options. But inaction is the most expensive choice you can make. Here is how the main exit paths compare side by side:

- Credit score damage: A completed foreclosure can drop your score by 100–150 points and stay on your report for seven years. (CFPB)

- Loss of equity: At a trustee’s sale, your home often sells for well below market value. Equity you’ve built disappears.

- Deficiency judgments: Missouri allows lenders to sue you for the difference between the sale price and the outstanding balance.

- Tax consequences: Forgiven mortgage debt can sometimes be treated as taxable income by the IRS.

Your Options When You’re Behind on Payments

Before jumping straight to a cash sale, it helps to know all your cards.

|

Option |

Best For |

Speed |

Credit Impact |

Keep Home? |

|---|---|---|---|---|

|

Loan modification |

Temporary hardship, enough income for modified terms |

30–90 days |

Moderate |

Yes |

|

Forbearance |

Short-term income disruption |

1–2 weeks |

Moderate |

Yes |

|

Cash sale |

Hard foreclosure deadline, need to move fast |

7–14 days |

Low (late payments only) |

No |

|

Short sale |

Underwater on mortgage, lender cooperation |

3–6 months |

Moderate–High |

No |

|

Let it foreclose |

No equity, no other options (last resort) |

142 days avg. |

Severe (7 years) |

No |

How a Cash Sale Helps You Sell Before Foreclosure in Missouri

When people search “we buy houses Missouri” or “cash offer for house,” they’re often in exactly this situation: behind on payments, running out of time, and looking for a way out that doesn’t leave them wiped out. Here’s how the timelines stack up:

No Repairs Required

Most cash buyers purchase properties as-is. You don’t need to spend money on fresh paint, new appliances, or a new roof — the buyer accounts for condition in their offer.

Certainty of Close

Traditional sales fall through constantly — buyers lose financing, inspections kill deals, and appraisals come in low. With a cash buyer, if they’ve made a written offer and you’ve signed, the deal almost always closes. That certainty is everything when you’re racing a foreclosure date.

Stops the Foreclosure Clock

The moment a cash sale closes, and the mortgage is paid off, the foreclosure process stops. The bank gets paid, the lien is released, and you’re no longer in default. Your credit takes a hit for the late payments — but not the catastrophic seven-year hit of a completed foreclosure.

You May Walk Away with Cash

If you have equity in your home — meaning the property is worth more than what you owe — a cash sale returns that equity to you. Even if the offer is below full retail value, the net amount you receive may be significantly more than you’d see from a foreclosure auction.

Step-by-Step Plan to Sell Your House Before Foreclosure

1. Get your payoff statement - Call your lender’s loss mitigation department and request a full payoff statement, including missed payments, interest, and fees.

2. Know your home’s approximate value - Use Zillow, Redfin, or a quick agent consultation to get a ballpark on current market value. You need to know if equity exists before talking to buyers.

3. Contact multiple cash buyers - Search “we buy houses Missouri” or “sell house before foreclosure Missouri.” Reach out to several companies. Legitimate buyers provide a no-obligation written offer within 24–48 hours.

4. Vet buyers carefully - Check Google reviews and the BBB. Ask for references. A reputable buyer is transparent about how they calculate their offer and will not pressure you to sign immediately.

5. Consult a Missouri real estate attorney or HUD counselor - Before signing anything, have someone knowledgeable review the contract. A Missouri attorney can check the title, verify there are no additional liens, and make sure the terms protect you.

6. Accept the best offer and set a closing date - Accept the offer that makes the most financial sense. Communicate your urgency — a good cash buyer can prioritize your closing if there’s a hard foreclosure deadline approaching.

7. Close and pay off the mortgage - At closing, the title company handles the mortgage payoff directly. Any remaining proceeds after the loan and closing costs go to you.

8. Notify your lender - Once you have a signed purchase agreement, contact loss mitigation and let them know a sale is in progress. They may pause collection activity while the sale closes.

Missouri-Specific Legal and Financial Tips

Missouri Is Non-Judicial — But You Still Have Rights

If your lender hasn’t followed proper notice procedures, there may be grounds to challenge the foreclosure. Missouri law requires a minimum 20-day written notice before the sale. An attorney can review whether proper steps were followed. See guidance from the National Consumer Law Center.

Watch Out for Additional Liens

Unpaid property taxes, HOA dues, or contractor liens all complicate any sale. A title company or real estate attorney can run a full title search. Never try to sell without knowing exactly what’s attached to the property. For licensed agent verification, check the Missouri Real Estate Commission.

Missouri Property Tax Sales Run Separately

If you’ve fallen behind on property taxes in addition to your mortgage, Missouri’s tax sale process runs on its own track. Counties can sell a tax certificate which can lead to a tax deed sale entirely separate from the mortgage foreclosure. Check with your county collector’s office.

Beware of Foreclosure Rescue Scams

Distressed homeowners are prime targets. Be extremely cautious of anyone who:

- Asks you to sign over the deed with promises to let you rent it back

- Guarantees they can stop foreclosure with no explanation of how

- Asks for upfront fees before doing anything

- Pressures you to decide immediately

- Asks you to stop communicating with your lender or a housing counselor

|

Legitimate Cash Buyer ✓ |

Warning Signs ✗ |

|---|---|

|

Written offer with clear terms |

Verbal promises only |

|

No upfront fees charged to the seller |

Upfront “processing” or admin fees |

|

Allows attorney review before signing |

Pressures you to sign immediately |

|

Verifiable Google/BBB reviews |

No online presence or reviews |

|

Closes through a title company or attorney |

Wants to close without a title company |

|

Explains how the offer was calculated |

Vague or evasive about the numbers |

Is a Cash Sale Always the Right Move?

Not necessarily. Here’s a quick framework:

- Significant equity + 60+ days to sale date: A traditional listing might net you more money.

- Underwater on the mortgage: A short sale or loan modification may be more appropriate.

- Foreclosure date is weeks away: A cash sale is almost certainly your best path — speed is everything.

- Truly temporary hardship: Talk to your lender first. A forbearance or modification might let you keep the home.

The Bottom Line

Facing foreclosure in Missouri in 2026 is a serious situation — but it’s not a dead end. The worst thing you can do is nothing. Whether you pursue a loan modification, a traditional sale, or a fast cash offer, taking action early is what separates homeowners who come out of this in one piece from those who don’t.

If you need to sell your house before foreclosure in Missouri, a cash offer can be the fastest, cleanest way to protect your credit, recover equity, and put this chapter behind you. Work with a buyer who is transparent, reputable, and gives you time to understand what you’re signing.

You built something when you bought that home. Even in the hardest circumstances, you deserve to exit with dignity.

Ready to Buy or Sell in St. Louis? House Sold Easy Has You Covered!

Navigating St. Louis’ red-hot luxury market doesn’t have to be a headache. With House Sold Easy, it’s all about less hassle—we’ve got you covered from start to finish. Our St. Louis experts know every corner of this city and will make buying your dream home or selling your high-end property a breeze. Don’t miss out on the hottest market in the U.S.! Contact House Sold Easy today and let’s make your real estate goals happen!