Hidden Costs & Smart Money-Saving Tips for St. Louis Buyers

Jan 16, 2026

Written by David Dodge

Buying a home in St. Louis can be an exciting and rewarding experience. The city and its surrounding areas offer beautiful historic brick homes, friendly neighborhoods such as The Hill, Tower Grove, or Maplewood, and a cost of living that remains significantly more affordable than in many other major U.S. cities. As we move through early 2026, the St. Louis real estate market continues to show strength and resilience. For example, according to recent market updates, homes in the St. Louis MSA sold for a median price of $275,000 in December 2025, which represented a solid 5.77% increase from the previous year, even with some seasonal fluctuations. You can find more detailed statistics and trends in the latest reports from sources like the St. Louis MSA Real Estate Market Update for January 2026.

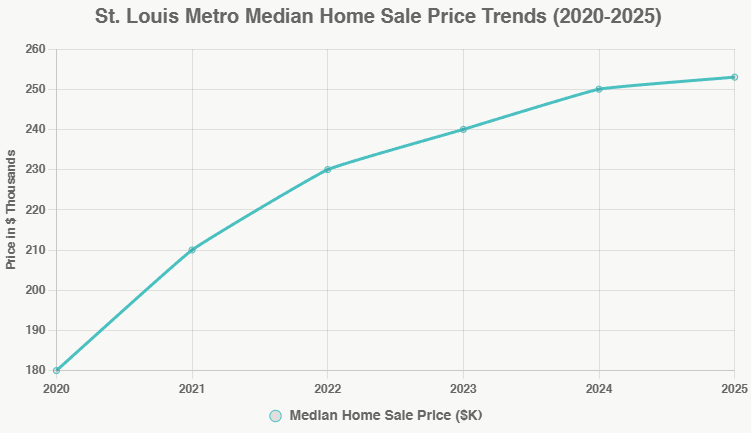

Here’s a clear visual representation of recent St. Louis home price trends based on legitimate, up-to-date data:

This line graph illustrates the upward trend in median home sale prices in the St. Louis area over recent years, highlighting steady appreciation despite some seasonal dips.

Here are relevant charts showing the market trends:

This chart captures the recent price climb in the St. Louis market (October 2024 context, reflective of ongoing upward movement into 2025-2026).

This visual provides a focused look at median price trends and growth patterns in the St. Louis area, aligning with the reported increases.

- Recent Legit Data Snapshot: As of December 2025, the St. Louis MSA median sold price reached $275,000 (a 5.77% increase from the prior year), with a median list price of $299,000 (up 6.41% YoY). City-specific figures vary, often around $235,000–$253,000 in core St. Louis areas, showing modest but positive growth into 2026.

While the overall affordability makes St. Louis appealing, especially for first-time buyers or those relocating, several hidden costs can catch people off guard if they're not prepared. These include differences in property taxes between the City and County, closing fees that add up at the end of the process, and special considerations for the many older brick homes that give the area so much character. The good news is that with careful planning and the right strategies, you can avoid many of these surprises and even save thousands of dollars along the way.

This guide explains everything in clear, straightforward language, so it's easy to understand. We'll walk through the main hidden costs step by step, share practical ways to save money, and finish with a simple checklist you can use as you go through the homebuying process.

Why Property Taxes Stand Out as a Major Ongoing Cost

One of the biggest long-term expenses when owning a home in St. Louis is property taxes. These taxes help pay for local schools, roads, police and fire services, and other community needs. The amount you pay is calculated by taking the assessed value of your home and multiplying it by the local tax rate.

What makes this especially important in St. Louis is the clear difference between the City of St. Louis and St. Louis County. In the City, tax rates can vary quite a bit depending on the neighborhood, and recent reassessments (like the 2025 cycle that affects current bills) have led to noticeable increases in some areas because home values have been rising. For many City properties, the median annual property tax bill comes in around $1,935, though it can be higher in popular spots. Official details on the 2025 Property Tax Rates for the City of St. Louis are available through the city's assessor's office.

In contrast, St. Louis County uses a system with separate subclass rates for different types of property, which has been in place since 2003. This approach helps keep rates more stable for homeowners, particularly for residential properties, which usually get the lowest rates. Median taxes in the County tend to be higher in some suburbs, often around $3,193 annually, partly because of the services provided. Some areas have even discussed levy increases (like a proposed 12.4% maximum for 2026 in certain discussions), but the subclass system generally provides more protection against sharp spikes.

To save on this ongoing cost, you can appeal your assessment if you believe your home's value has been set too high—many people succeed by providing evidence such as recent comparable sales in the area. There are also exemptions available for things like homestead status, seniors, or people with disabilities. Always use the online tools from the City or County assessor's offices to get a good estimate before you buy, so you can factor this into your monthly budget realistically. Expect to pay anywhere from $2,000 to $4,000 or more per year, depending on where the home is located and its value.

Closing Costs: What to Expect When You Finalize the Purchase

When you reach the closing table, you'll pay a set of fees known as closing costs. These cover things like loan processing, title searches, appraisals, and prepaid items such as property taxes and homeowners' insurance that get set up in advance.

Missouri is actually one of the most buyer-friendly states when it comes to these costs, with averages falling between 0.8% and 2% of the home's purchase price (not counting realtor commissions). For a typical $275,000 home, that usually means $2,200 to $5,500 total for the buyer. In St. Louis specifically, you'll encounter standard fees like title insurance and settlement charges (often $300–$800), plus an appraisal ($400–$600). If you're buying in the City, keep in mind the Housing Conservation Inspection, a required check for many properties to ensure they meet basic safety and code standards—it's usually around $120 for most units. More information is available on the City of St. Louis Housing Conservation page.

These costs can feel like a surprise at the end, especially if prepaids are higher for an older home. The best way to keep them down is to shop around with different lenders, compare their Loan Estimates carefully, and ask about any credits or discounts they might offer.

Special Inspections Needed for Older Brick Homes

A huge part of St. Louis's appeal comes from its inventory of beautiful older brick homes, many built before the 1950s. These houses have incredible character, thick walls, and timeless style, but age means they can have hidden issues that aren't always obvious during a walkthrough.

Common problems include cracks or seepage in the foundation (often due to the region's clay soil and freeze-thaw cycles), worn tuckpointing (the mortar between bricks that needs replacement every 10–15 years), leaking chimneys, outdated electrical wiring like knob-and-tube, old plumbing, termite damage, damp basements with mold potential, uneven floors, or roof issues.

To protect yourself, plan for several key inspections. A standard general home inspection usually costs $350–$500 and gives an overall look at the structure and systems. Many buyers in St. Louis also add a sewer lateral scope ($150–$300) because old clay pipes are common and can fail. Radon testing ($150–$200) is smart since Missouri has moderate risk levels, and a termite inspection is often required by lenders. If anything looks concerning, you might need a structural engineer or chimney specialist.

These inspections are worth every penny because they uncover problems you can then negotiate with the seller—perhaps getting credits, repairs, or a lower price. Skipping them could lead to expensive surprises later, like $5,000–$15,000 for major tuckpointing or foundation work.

Other Hidden Costs to Anticipate

Beyond the major categories already covered, several additional expenses can quietly add up during and after the homebuying process in St. Louis. These smaller but still significant costs are easy to overlook if you're focused only on the purchase price and down payment.

Homeowners insurance is one of the most important ongoing expenses. For older brick homes—which are very common in St. Louis—insurance premiums tend to be higher than average. The age of the home, its location (especially in flood-prone areas or neighborhoods with higher crime statistics), and specific features like an older roof or outdated electrical systems can all drive up rates. Many buyers find themselves paying between $2,500 and $4,000 or more per year for adequate coverage. In some cases, if the property sits in a designated flood zone, you'll also need separate flood insurance, which can add several hundred to over a thousand dollars annually, depending on risk level.

Immediately after closing, most new homeowners discover minor repairs or updates they want to make right away. This could include fresh paint, new light fixtures, carpet cleaning or replacement in high-traffic areas, fixing small plumbing issues, or addressing cosmetic wear that wasn't noticeable during showings. It's wise to set aside $5,000 to $10,000 for these initial post-closing repairs and improvements so you can settle in comfortably without stretching your budget too thin.

Don't forget about one-time setup costs like transferring utilities, scheduling movers, changing locks, or paying any minor HOA fees if the property is part of a homeowners association (common in some suburban areas). If the home is in a low-lying area near rivers or creeks, flood insurance might become a recurring necessity as well.

To help you visualize the potential first-year extras (beyond your down payment and mortgage principal), here is a quick estimate table of the most common hidden or additional costs:

| Cost Item | Typical Range |

|---|---|

| Closing costs | $2,000–$5,500 |

| Inspections | $500–$1,500 |

| Annual property taxes | $2,000–$4,000 |

| Insurance (first year) | $2,500–$4,000 |

| Initial repairs/maintenance | $3,000–$10,000 |

These numbers are based on typical experiences for St. Louis buyers purchasing older homes in the current market. Your actual totals will vary depending on the home's condition, location, and the specifics of your loan and insurance choices. Planning for these extras upfront makes the transition to homeownership much smoother.

Smart Ways to Save Money During the Process

The current market, with inventory slowly increasing but still somewhat limited (often 2–3 months' supply in many areas), gives buyers some room to negotiate, especially if a home has been on the market longer.

One of the best strategies is asking for seller concessions—many sellers agree to contribute 2–6% of the purchase price toward your closing costs, repairs, or even a home warranty. This can easily save $5,000–$10,000 or more.

If you're a first-time buyer (or haven't owned in the last three years) or a qualified veteran, look into the Missouri Housing Development Commission (MHDC) programs. The First Place program offers below-market interest rates plus up to 4% in forgivable down payment and closing cost assistance. For those with slightly higher incomes, the Next Step program provides similar benefits. Check the latest details directly on the MHDC homebuyer programs page.

Other savings ideas include shopping lenders for the best rates and fees, negotiating after inspections to cover specific repairs, and timing your offer when more homes are available.

Your Simple Step-by-Step Checklist

Here’s an easy-to-follow checklist to keep you on track:

- Before making an offer, get pre-approved for a mortgage, research tax rates using City or County assessor tools, and see if you qualify for MHDC programs.

- When writing your offer, include an inspection contingency for protection, request seller concessions (like 3% toward closing costs), and note any required City inspections.

- During the inspection period, schedule the general inspection plus sewer, radon, and termite checks. Pay close attention to brick-specific items like tuckpointing and foundation. Use findings to negotiate repairs or credits.

- As you approach closing, budget 2–5% for costs, finalize any MHDC applications, and carefully review your Loan Estimate.

- After you move in, consider appealing your property tax assessment if it seems high, and plan for regular maintenance like tuckpointing every decade or so.

Final Thoughts: Make Your St. Louis Home Purchase a Smart One

St. Louis combines historic charm, strong communities, and real affordability, but understanding the local property tax differences, closing realities, and needs of older brick homes helps you avoid surprises. By using programs like MHDC incentives, negotiating seller help, and budgeting carefully, many buyers save significant money and feel confident in their decision.

If you're ready to start, talk to a local real estate agent or lender who knows the area well—they can provide personalized guidance. Download or print the checklist above, run some online calculators for taxes and closings, and feel free to share your own experiences in the comments. Your dream home in St. Louis is closer than you think!

Ready to Buy or Sell in St. Louis? House Sold Easy Has You Covered!

Navigating St. Louis’ red-hot luxury market doesn’t have to be a headache. With House Sold Easy, it’s all about less hassle—we’ve got you covered from start to finish. Our St. Louis experts know every corner of this city and will make buying your dream home or selling your high-end property a breeze. Don’t miss out on the hottest market in the U.S.! Contact House Sold Easy today and let’s make your real estate goals happen!